The Positive

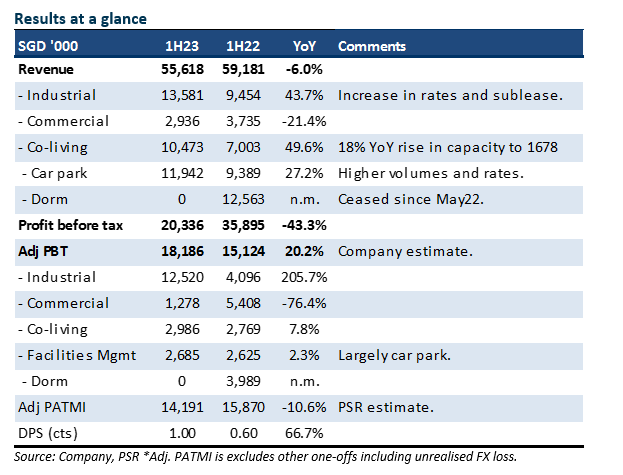

+ Growth in co-living and car park. Co-living revenue surged 50% to S$10.4mn. The improvement came largely from higher room rates and a new 105 keys Coliwoo Lavender (opened in Sep22). The 411 key Coliwoo Orchard started only in Feb23. And contribution in 1H23 has been minimal. Car park revenue rose on the back of increased volumes. This was despite the number of car parks remaining flat at 74 (or ~21,500 vehicle parking lots).

The Negative

– Higher interest expense due to expansion. Interest expense almost doubled to S$4.4mn in 1H23 due to higher interest rates and an increase in net debt to S$144mn (1H22: S$98mn). The rise in debt was due to acquisition of 404 Pasir Panjang and 48 Arab Street. Other options for LHN to de-gear include monetising its properties. A further source of recycling capital is the completion of the 55 Tuas food factory project, where strata units will be sold.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.