The Positives

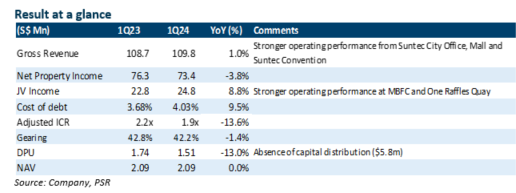

+ Income supported by high rental reversion and increasing contribution from Suntec Convention. Singapore offices’ rental reversion was 11.2% in 1Q24 and 21.7% for Suntec City Mall. Pure Yoga and Pure Fitness have returned ac.41k sqft back to SUN, and only 25% of it has been backfilled. Rental of backfilled is c.21% higher. As Singapore positions itself as the MICE spot and lines up events until the end of 2028, Suntec Convention Center is well-positioned to capture the momentum, given its central location, amenities, and the delay of the MBS renovation. Revenue for the convention center is up by 26.1% to S$11.6 mn, and we expect it to contribute to approximately 20% of total revenue in FY24e.

+ Firm on the S$100mn divestment goal. SUN is committed to the S$100mn divestment goal no plans on lowering the price. The proceeds generated will be used for debt repayment, with the aim of lowering gearing to 40%. The S$100mn strata units contribute to c.2.5% of the total revenue, thus compressing DPU by 1.5% after factoring in interest savings from debt repayment.

The Negative

– The creeping up in vacancy rate is overshadowed by high rental reversion. The retail and office occupancy rates at potfolio level saw a 2.1% points YoY and 3.5% YoY decline, respectively. We expect further downtime is required for 55 Currie Street and The Minster Building. Australia saw more leasing demand dropback due to supply influx in the CBD area; effective rental reversion was at negatives for 1Q24. SUN also observed increasing incentives for the Australian market, thus compressing earnings; incentives are up to 35-45% of the total income of the contract period. Valuation for the Australian side may decline further in the face of a possible cap rate expansion of 25bps.

– Borrowing cost inching up. Given the high-for-longer interest rates generally priced in by the market, we expect elevated interest costs to continue eroding DPU. FY24e, the cost of debt is expected to increase by 4.2%. However, the weakening start of FY24 may just mean that some extra patience is required to get there. We are still confident in SUN’s ability to generate cyclical rebound due to its lower % hedging ratio of 57% as of the end of 1Q24.

Miaomiao mainly covers the Singapore REITs sector and graduated from Singapore Management University with a Bachelor’s degree in Business Management.