The Positives

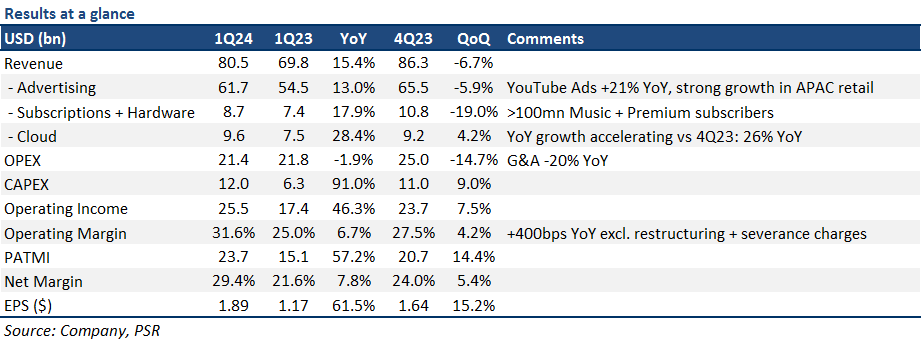

+ Search is still strong, and YouTube is seeing a quick acceleration in growth. Search advertising growth remained resilient at 14% YoY, driven by strength from Chinese retailers, which began in 2Q23. YouTube ad revenue saw a significant reacceleration to 21% YoY (4Q23: 16% YoY) as a result of higher user engagement on the platform, particularly in Shorts. YouTube ad revenue was driven by both strengths in direct response and brand advertising, with Shorts monetisation continuing to improve (monetisation rate >2x YoY).

+ Cloud remains the fastest growing segment, benefitting from AI offerings. Cloud growth accelerated to 28% YoY (4Q23: 26% YoY) as it remained GOOGL’s fastest-growing segment. Growth was supported by an increase in average revenue per seat, reflecting stronger demand for GOOGL’s cloud infrastructure and Generative AI solutions. Cloud’s 2nd quarter of accelerating growth indicates a resumption in customer spending likely due to continued migration to the Cloud and AI-related offerings – which was also seen from GOOGL’s key competitors Amazon’s AWS and Microsoft’s Azure.

+ Margins continue to expand due to ongoing efficiency efforts. GOOGL’s ongoing cost optimisation efforts continue to pay off – leaner organisational structure and improved product prioritization, with its 1Q24 operating margin of 31.6%, a 670bps increase YoY (+400bps YoY excl. restructuring and severance related charges), and is almost back to pandemic highs of 32.3%. GOOGL also reiterated its focus on moderating expense growth and its commitment to expanding margins, even in the face of higher AI-related investments. Headcount was down -5%/-1% YoY/QoQ. We raise our FY24e PATMI by 8% on higher operating leverage and cost efficiencies.

The Negative

– Higher CAPEX is a headwind to valuations. GOOGL’s 1Q24 CAPEX almost doubled to US$12bn as the company increased its investments in AI-related infrastructure like servers and data centres to support future AI development. GOOGL also mentioned that it would sustain this level of spending through the rest of FY24e. As a result, we increase our FY24e/FY25e CAPEX by ~25% YoY each to account for the higher levels of investments.

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.