The Positives

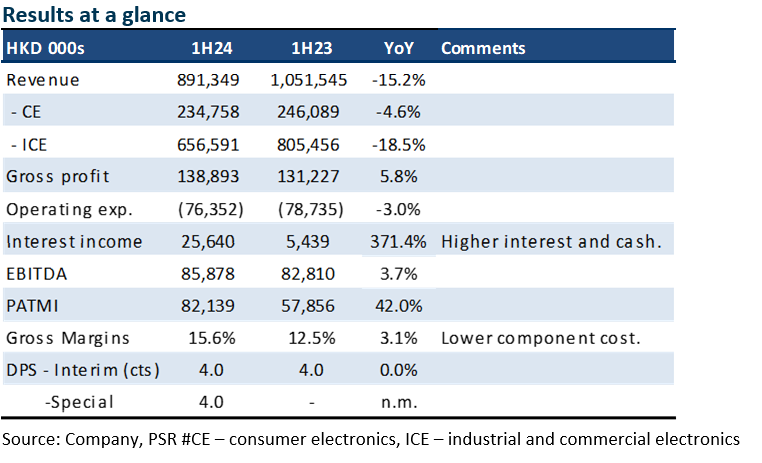

+ Recovery in margins. There were several drivers for the improvement in margins, namely, lower renminbi, reduction in staff, decline in depreciation and fall in component cost. Despite the increase in capex over the past three years, depreciation fell as most of the spending was on property and fittings which have a slower depreciation rate than equipment.

+ Unprecedented special dividend after interim results. The company announced a HKD4 cents special dividend in addition to the interim HKD4 cents. Valuetronics generated HKD179mn of free cash flow in 1H24 (1H23: HKD112mn), adding to their cash hoard of HKD1.143bn.

The Negative

– Decline in revenue. ICE segment registered an 18.5% decline in revenue. A large reason for the decline was lower component prices rather than weak demand. During the component shortages a year ago, some components had to be purchased at exorbitant spot prices on cash terms that were reimbursed by customers. The supply chain or lead times have normalised.

Outlook

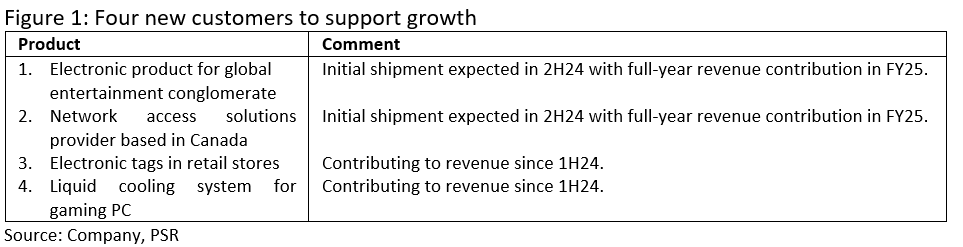

We expect a stronger 2H24. Revenue growth will come from the four new customers (Figure 1) announced by the company. Margin expansion is expected to continue from a higher mix of ICE products, increased volumes and weak renminbi.

Maintain BUY with a higher TP of S$0.70 (prev. S$0.61)

Our target price is based on industry valuations of 11x PE 1-year forward earnings.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.