The Positives

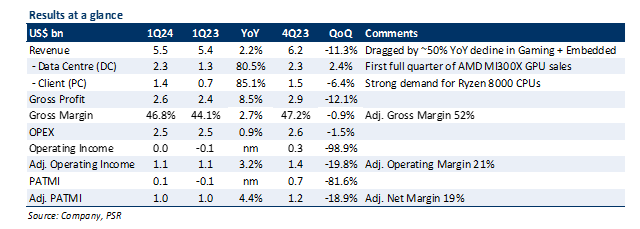

+ DC growth supported by strong MI300x ramp-up and server CPU gains. 1Q24 was the first full quarter of MI300x sales (~US$600mn) as customer demand for AMD’s AI GPUs remained strong. MI300x deployments expanded at Microsoft, Meta, and Oracle, with customer feedback of better inferencing performance vs. Nvidia’s H100. AMD raised its FY24e GPU revenue to >US$4bn (prev. >US$3.5bn) on improving demand-supply dynamics, which we estimate equates to roughly US$300mn additional ramp per quarter. Server CPU (EPYC) growth is also doing well (est. ~25% YoY), with enterprise customers beginning their server refresh cycle and expanding cloud and on-premise deployments. EPYC adoption is accelerating due to higher efficiency and cost savings (~45%) vs. competitors, with AMD gaining market share. AMD guided strong YoY growth for GPU and CPU sales in 2Q24e.

+ Early signs of PC upgrading cycle with strong demand for Ryzen 8000 CPUs. AMD’s PC segment grew to 85% YoY (4Q23: 62% YoY), significantly quicker than main competitor Intel (31% YoY). Demand from OEMs picked up, with desktop CPU sales growing strong double-digits YoY and laptop CPU sales almost doubling. AMD is anticipating growth in the PC market for 2024 due to 1) early signs of a refresh cycle from enterprises, and 2) increasing AI PC adoption. AMD guided its PC segment to increase QoQ, and significantly YoY due to higher volume and ASPs.

The Negative

– Gaming is still a huge drag, with Embedded recovery delayed. Gaming and Embedded were both down ~50% YoY, with Gaming still weak due to its 5th year in the console cycle and customer inventory still elevated. AMD expects weakness in Gaming to continue significantly into 2H24e. Embedded’s -46% YoY decline was more than expected due to weaker demand from the communications, industrial, and automotive sectors. The overall segment looks to have bottomed, although AMD expects the recovery to be more moderate. Recovery in the Embedded segment will be a tailwind to overall margins (1Q24 Adj. Operating Margin: 40%).

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.