In the last report “all clear for now”, we illustrated a list of nine indicators that we are watching closely to spot any cracks within the general equity market. Since then, the market continued to break new record highs as the respective indicators remained well in check. For this report, we will include another list of six recession indicators to build a more comprehensive view of the market.

Euphoria and complacency remain the main theme here as we marched into 2018, bringing the length of the economic expansion to 101 months, third longest in history.

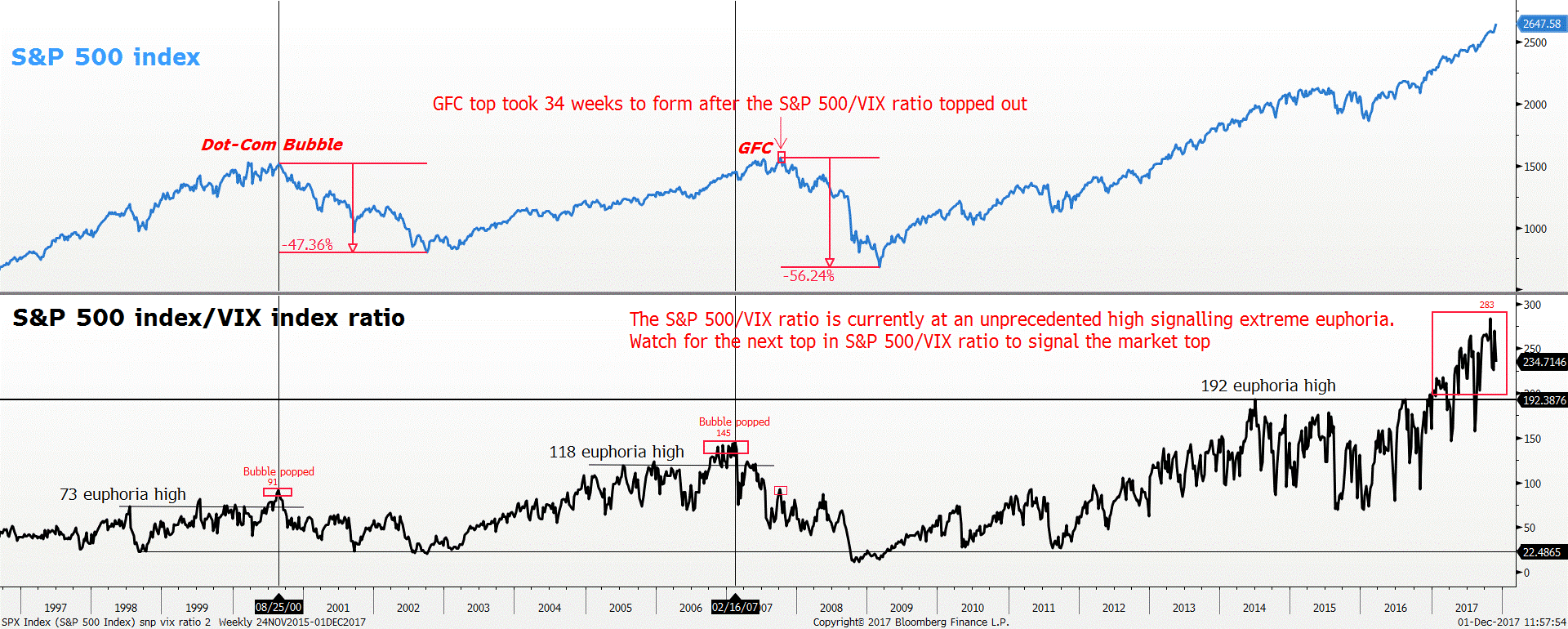

A good barometer for accessing market complacency is to look at the S&P 500/VIX ratio. S&P 500 index is a capitalization-weighted index of 500 stocks while VIX index shows the market expectations of 30 days volatility implied by S&P 500 index options. Both have a strong inverse correlation, but the recent violent whipsaw within the VIX index is showing the true dangers of an over complacent market. Small down days in the S&P 500 index could lead to a forceful spike in VIX index of up to 30% or more due to the excessive amount of shorts within the VIX Futures and Options market.

Figure 1: S&P500/VIX Index ratio – Unprecedented euphoria

During the Dot-Com boom of the 1990s and housing boom of 2000s, the highs this ratio was at 73 and 118 respectively, representing euphoria. As time goes by, the ratio continued to rip higher with the current era euphoria high being 192. New extreme high tend to signal bubble behaviour and the fall out of the ratio tends to signal the end of the bubble.

For example, during the Dot-Com era, after surpassing the 73 euphoric high on numerous occasions since July 1999, the ratio hit an extreme new record high of 91 before imploding, leading to fallout in the S&P 500 index with prices falling 47%.

During the housing boom decade of 2000, the newly formed euphoric high point was around 118. Since December 2005, the ratio has been edging higher above 118 signalling bubble environment. Ultimately, in early 2007, the ratio formed a record high of 145 and subsequently deep dived into a downtrend. As a result, the market managed to take an early warning signal from the falling ratio, and the housing bubble popped 34 weeks later with the S&P 500 index tumbling 56%.

The current environment is at a whole new exhilarating level, as the ratio way surpassed the 192 extreme euphoria high formed in 2014. Since early 2017, the ratio has been breaching new record highs suggesting growing complacency. The recent all-time high that was established in November 2017 stands at 283. Watch this ratio closely to see if the complacency continues to evolve higher or if the 283 high becomes the current cycle’s high. Keep in mind the during housing boom period of 2000, the topping of the ratio provided a 34 weeks warning before the S&P 500 index peaked out.

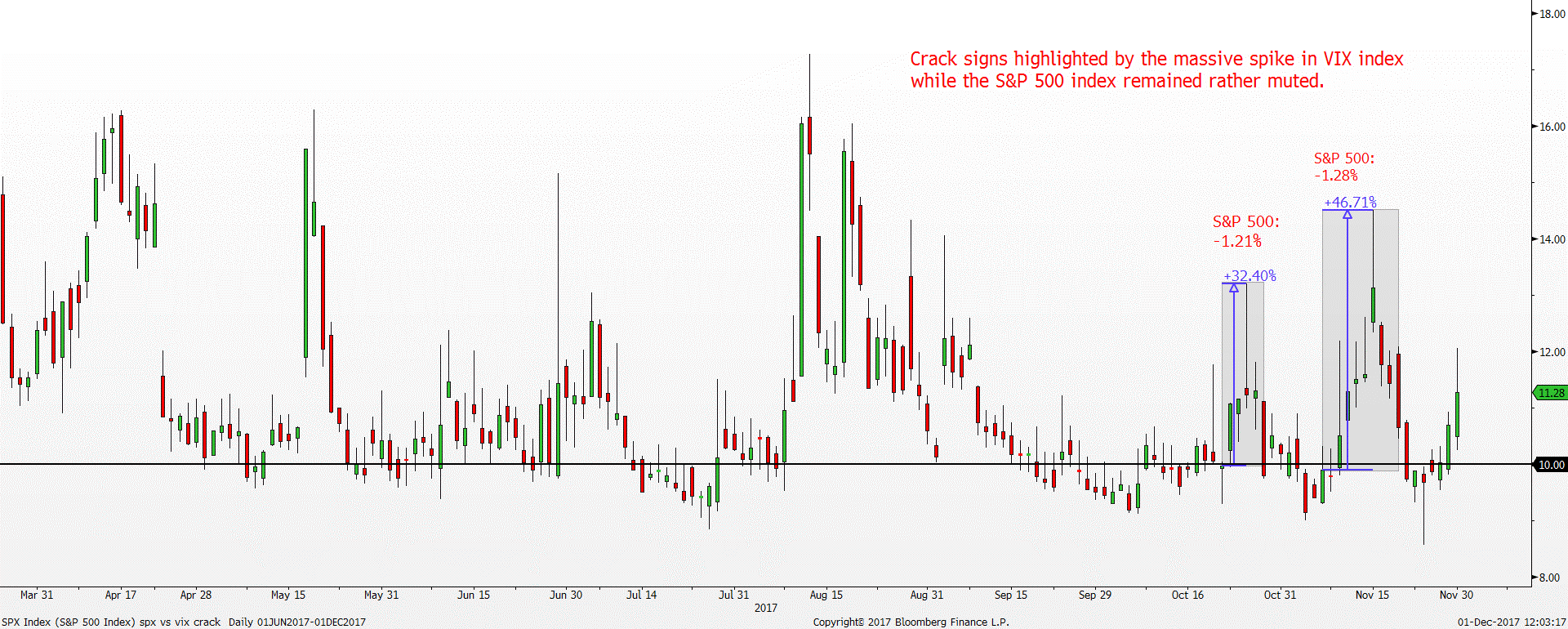

Figure 2: VIX Index exhibiting signs of vulnerability

The volatile move within the VIX index became more apparent recently as the VIX index consolidates around the 9 to 10 range. The erratic move higher was seen on 20 October when the VIX index spiked 30% over the following three trading days to a high of 13.20 even when the S&P 500 index only fell -1.21% over the same period.

A similar fragility from the VIX index surfaced again on 7 November where it surged to a high of 14.5 over six trading days, representing 45% spike in the VIX index. On the flip side, the correction from S&P 500 index remained rather muted as the S&P 500 index only lost -1.25% during the same period. Bear in mind the previous two examples of volatility spikes happened in the absence of any earthshattering news which reinforces the idea of growing cracks within the VIX index. As the shorts within the VIX universe continues to pile on with the belief that volatility will continue to stay subdued, a short squeeze of epic proportion is waiting to be unleashed. The exact timing of capitulation remains open for all to guess but by relying on our list of recession indicators provides us with a better sensing of the market movements for any possible catastrophic moves.

Even though we are currently in the late stage economic cycle, the current blow-off phase could last longer than expected. Hence, we have devised a list of recession indicators to spot for the major turning point. The previous list of indicators mentioned in “all clear for now” two months ago has yet to signal any drastic change yet.

All remains well for now, and the following list of recession indicators drives to the same optimistic conclusion.

Indicator 1: VIX Index – Canary in the coal mine

As the VIX index trades at different levels, it reveals the different stages of the general equity market. Our study has shown that the following criteria need to be met before the market goes into a meltdown mode:

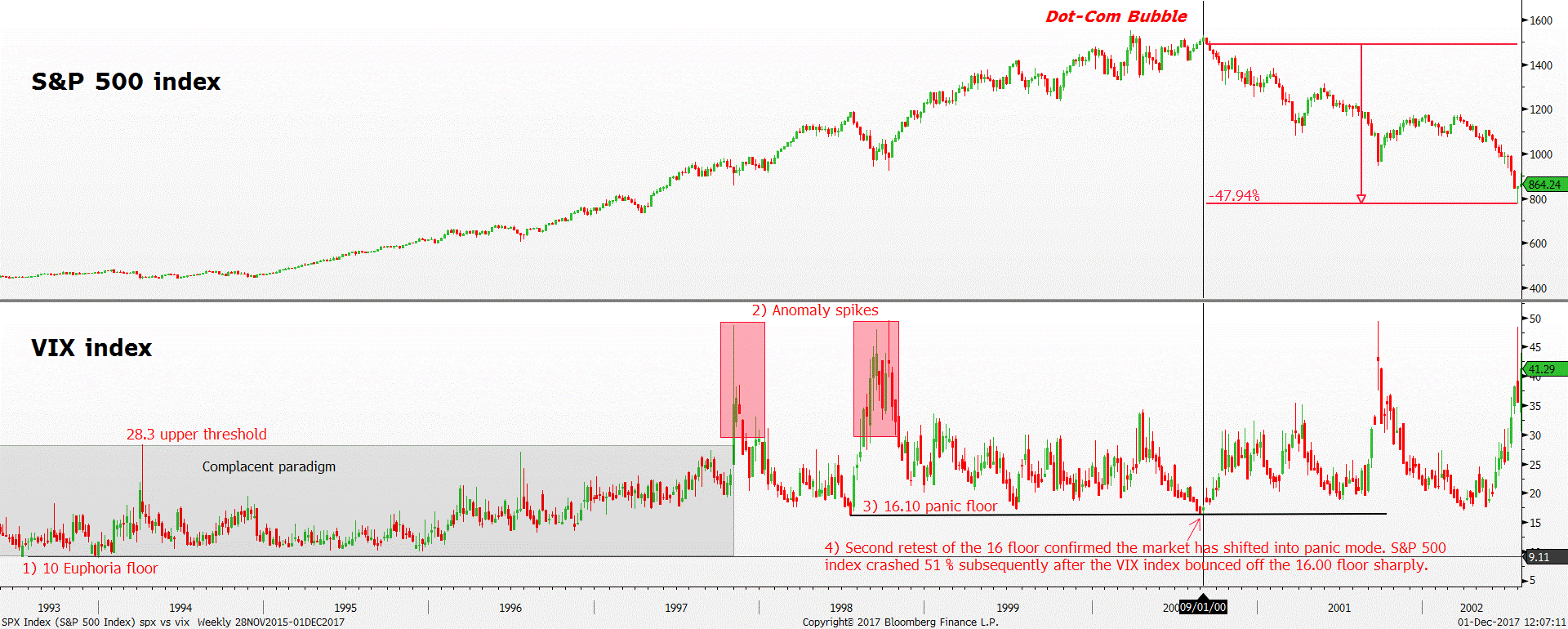

Figure 3: VIX Index – Dot-Com case study

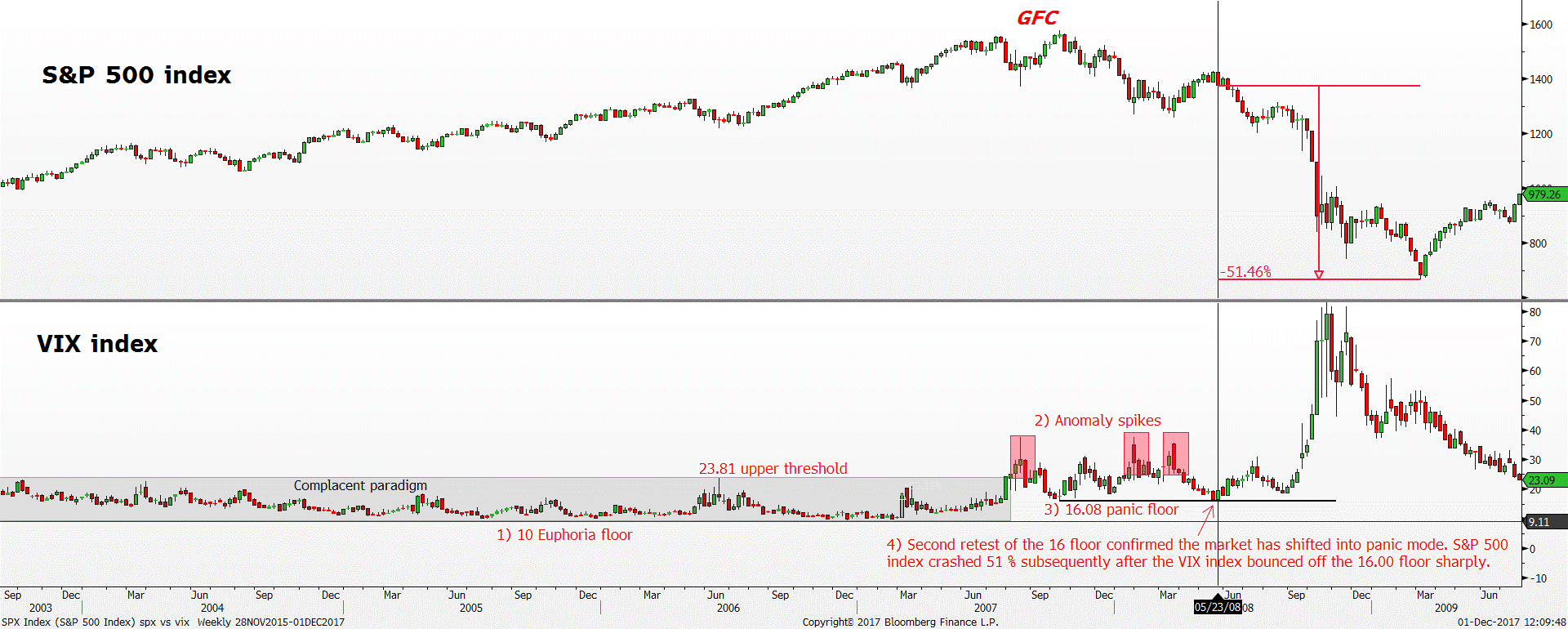

Figure 4: VIX Index – Global Financial Crisis case study

*Vertical line demarcates the point where the VIX index retested the 16 panic floor for the second time where the bearish narrative was confirmed

To illustrate the above better, the housing boom period of 2000 was a good example of using the VIX index to time the market movement especially when the market is reversing starkly from its bubble high.

After hitting a high of 48.46 in July 2002, the VIX index trended lower back to the safe zone. The VIX index fell to a low of 9.39 over the next four years as it stayed comfortably below 15 for most of the time since November 2014 with 10 acting as the euphoria floor. Prior to the panic of the great financial crisis (GFC), extreme euphoria was signalled by the excessive suppression of the VIX index as it traded below 13 for 27 weeks since August 2006. Some sign of panic eventually kicked in in March 2007 as the VIX index spiked 83% in the week ended 2 March 2007. Criteria 2 was only fulfilled subsequently in July 2007 as the VIX index broke above the 23.81 upper threshold. As the VIX index continued to spike to a new high at 37.5 in the following weeks, the subsequent renormalisation of the volatility formed the new panic floor at 16 on 10 December 2007. Ultimately, the second retest of the 16 floor in May 2008 confirmed the market is undergoing great distress. Once the 16 floor was retested on May 2008, volatility sprang back to life and confirmed the gravity of the situation. The S&P 500 index eventually crashed 50% from the point where the VIX index spiked higher after retesting the 16 floor for the second time.

A similar price action pattern also unfolded during the Dot-Com bubble era where the retest of the 16 panic floor for the second time signalled the equity bubble top.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Jeremy specialises in Technical Analysis and has 10 years of experience in studying price action. His areas of expertise include intermarket analysis on the equities, currencies, commodities and bonds market.

He is also a regular columnist on The Business Times - every Monday ChartPoint column.

He graduated with a Bachelor of Science in Banking and Finance from University of London.