The Positive

+ Early mobile price repair in Australia. Optus postpaid ARPU of A$42 is the highest in more than four years. We believe price repair is underway. Competition, especially for entry-level price plans, has eased, and prices are edging higher. Despite the network outage, mobile service revenue grew 3.4% YoY.

The Negative

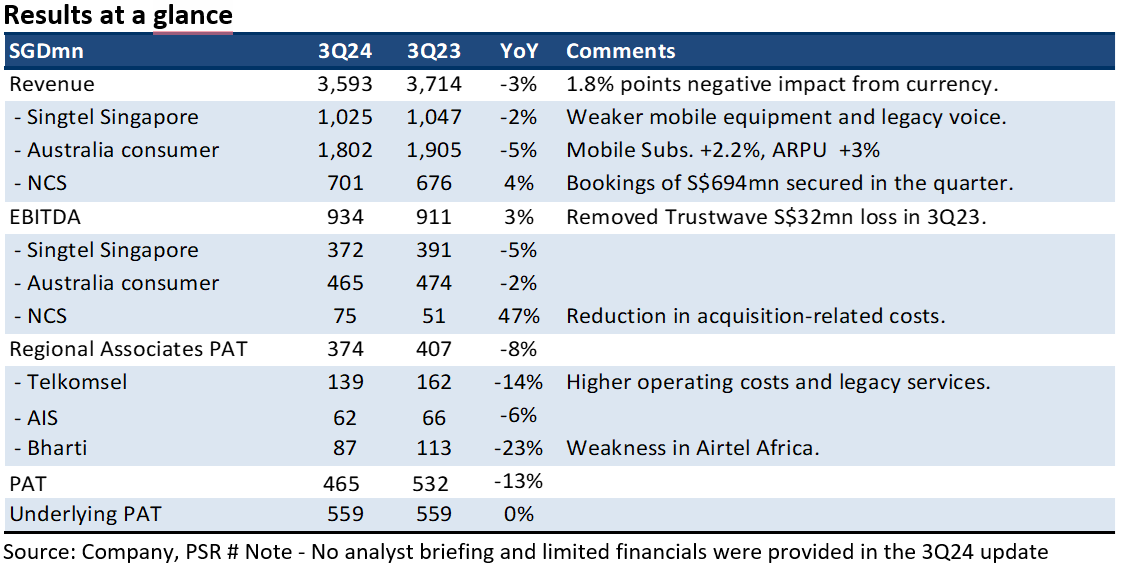

– Airtel Africa currency hit. Contribution from Bharti Telecom declined 23% YoY to S$87mn. Operations in India grew 14% YoY supported by an 8% rise in ARPU to Rp208. Currency took a toll on the results, with a 4% decline in the rupee against the Singapore dollar. A translation loss hit Africa operations due to the weakness in the Nigerian Naira.

Outlook

We expect mobile price recovery in Australia, India, Thailand, and Indonesia to drive earnings growth. An upside surprise in margins will stem from Singtel’s planned S$600mn reduction in core cost, largely in Optus.

Maintain BUY with unchanged TP of S$2.80

Our SOTP valuation is based on 6x EV/EBITDA (in line with peer valuation) for Singtel’s core Singapore and Australia businesses, and associates are marked to market after a 20% discount to reflect volatility in their share prices.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.