SECTOR SNAPSHOT

In the near-term, SREITs earning will take a hit due to the rental waivers extended to tenants, higher vacancy rates as well as lower rental reversions as a result of the softer leasing demand. In the long term, how businesses use space will change. In our opinion, COVID-19 is an accelerator and not a disruptor of the structural changes in the real estate industry and REIT market. However, as the dust settles and economies gradually reopen, we see potential re-rating catalyst for the REIT sector.

1. SREITs and investors are forced to embrace higher leverage, narrowing the gearing gap between SREITs and their global peers.

In July 2019, MAS released a consultation paper on the proposed raising of leverage limits for SREITs with minimum interest coverage ratios (ICRs) of 2.5x from 45% to 50%. Amongst the REIT markets, Singapore and Hong Kong have the lowest gearing limit of 45%, Malaysia imposed a 50% gearing limit while Thailand allowed leverage limits of up to 60% for REITs with investment-grade credit ratings. Other developed REIT markets like Australia, Japan, United States and France do not impose leverage limits. Despite the conservative leverage limits that SREITs are subjected to, gearing ratios for most SREITs ranged between of 28% to 38%, maintaining a minimum of 5% buffer from the statutory leverage limit. Additionally, market participants seem to punish SREITs with higher gearing, indicating that conservatism is preferred.

To help SREITs prevent accidental breaches of the leverage limit due to market forces beyond REIT managers’ control (such a deterioration of asset values) and provide flexibility for REITs to draw on debt facilities to meet cashflow mismatches, MAS raised the leverage limits to 50%, deferring the 2.5x ICR pre-requisite until 1 January 2022.

While we expect SREITs to gradually utilise the higher gearing headroom, the market turbulence induced by COVID-19 forced SREITs and investors to confront and get comfortable with the possibility of higher gearings. We believe this paves the way for a REIT market that is more receptive to higher leverage ratios, which in the long run, allows SREITs to be able to move more swiftly when competing with private funds and other REITs for assets, and allow SREITs the flexibility to optimize their capital structures. The additional 5% of gearing headroom translates to substantial debt headroom for SREITs, depending on the size of their asset base.

2. COVID-19 only accelerated the technology-enabled structural shifts, providing opportunities to make portfolios more future-ready.

Right-sizing, be it through tenants becoming more efficient with their space requirements or averaging down the cost of space through the hub-and-spoke strategy, has been a pre-existing risk for the commercial sector. Similarly, the threat of e-commerce has been a growing threat over the years.

As part of active management, landlords have been exploring various methods to pad demand as well as increase tenant stickiness. New demand from flex space operators have helped to soak up some of the supply in the recent years. We have seen some developers take stakes in coworking operators to get a better understanding of the operations and sustainability of this trend. Retail landlords have embarked on reward programs to drive tenant and customer stickiness, embrace e-commerce trends through the promotion of an omni-channel model and experiment with lease structures with higher risk-sharing.

Office:

Stronger use case for flex space

Right-sizing of space by traditional users of office space (finance, legal and tech companies) has been an ongoing trend. In recent years, new demand from flex space operators has helped to soak up some of the supply. Lockdowns have resulted in 70% to 99% of tenants’ workforce telecommuting and is a test on the necessity and dependence on office space.

COVID-19 has resulted in new uses for flex space – as a scalable solution for business continuity plans. 79 Robinson Road achieved TOP on 5 May 2020, with committed occupancy of 70%, including 10.8% of NLA (56,0000 sqft) of space taken up by Bridge+, CapitaLand’s wholly-owned coworking and flex space operator. As the structural shifts gradually unfold in this uncertain economy, the outlook for flex space is optimistic as an intermediate stage in the change of occupier strategy, as well as scalable space solution for new businesses entering the market.

Retail:

Retail landlords using e-commerce and to future-proof the traditional retail

On 22 May 2020, CapitaLand announced the launch of ecommerce platform (eCapitaMall) and online food ordering platform (Capita3Eats), accessible via CapitaLand’s CapitaStar app and mall website. A move towards digitalisation and an omni-channel experience, eCapitaMall offers shoppers the flexibility to browse online before purchasing in-store or browse in-store before purchasing online. For online purchases, shoppers can opt for home delivery or in-store collection. Separately, Capita3Eats is a food ordering platform that offers consumers three ways to fulfil their food orders – delivery, takeaway or dine-in. CapitaStar member will earn reward points (dubbed STAR$) for transactions made through both platforms. By opening the eCapitaMall and Capita3Eats to non-tenant retailers, CapitaLand is able to direct more traffic and sales to existing tenants as the STAR$ have to be spent at the malls, or converted into CapitaLand vouchers.

CapitaLand has been expanding its ecommerce capabilities, championing the omni-channel retailing strategy. By embracing and using ecommerce and digitalisation to complement the brick-and-mortar model, CapitaLand has provided shoppers with an enhanced shopping experience. The extended period of non-trading (especially for non-essential trades) due to the COVID-19 outbreak provided an opportunity for retail landlords to display their adaptability and build a stronger ecosystem to drive tenant and customer stickiness. The trio of CapitaStar, eCapitaMall and Capita3Eats will not only help tenants during this period of depressed sales, but position CapitaLand-branded malls for the future.

The silver lining in the move towards risk-sharing

The COVID-19 situation has highlighted the vulnerable positions retail tenants are in, with their thin margins, as well as the market’s expectation for landlords to have “more skin in the game”. During the circuit breaker, approximately 25% of mall tenants were operational.

In the long run, higher risk-sharing may increase the demand for retail space as the lower fixed rents makes it more economically viable for new-to-market brands to give the brick-and-mortar model a go, or brands looking to embark on the omni-channel route. We have seen CMT employ this strategy with Funan, which has a comparatively higher number of tenants on lease structures with a larger GTO component – 30% of Funan’s tenant are new-to-market brands. While this may result in more variable revenues, we believe active tenant management through due diligence in tenant selection will help manage the risk.

3. Tried and tested: REITs remain an attractive yield play – testament to the leasing strategies and portfolio attributes REITs have embedded in their portfolios

REITs have implemented leasing strategies and portfolio attributes that will help maintain stable distributions. These include long WALEs, well-distributed leases and debt expiries, balanced of stable and growth leases and prudent interest rate and FX management strategies. DPUs for most REITS are expected to be lower in FY20. However, this is largely due to the rental rebates granted to tenants during these unprecedented times. Barring such extreme events, and in spite of the structural shifts that will unravel in the following years, we believe REITs that have incorporated sufficient stabilising attributes will continue to provide stable distributions.

Through the postponement of some government land sales, as well as landlords exploring redevelopments and change-in-use, we believe supply will adjust to help the real estate sector achieve a healthy equilibrium. While leasing activity is expected to be softer in the near term, construction slippage and higher renewals (due to companies delaying expansion and relocation plans) will provide some near-term support.

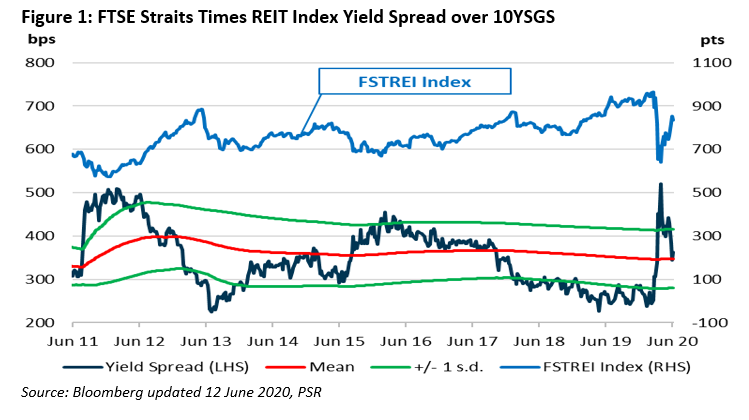

4. Better entry price – yield spread at 0.24 SD level

Recovery in the REIT sector is under way, with the FTSEREI Index dividend yield of 4.6% matching the 2019 average yield of 4.6%. With interest rates at depressed levels, the dividend yield spread of 3.6% compares favorably with 2019’s average of 2.6%, an attractive return for a stable yield investment. The FTSREI Index is currently trading at the mean (0.24 SD), a better entry compared to the -1.0 to -2.0 SD levels seen in the last 2 years (figure 1).

5. Recovery in prices and low interest rates presents a conducive environment for acquisition.

The lower interest rate environment presents a conductive environment for REITs given that interest expense accounts for c.30% of expenses for REITs. With the recovery of share prices, acquisitions which are usually financed through a mix of equity and debt will start looking accretive. Well-capitalized REITs will seize the opportunity to pick up distressed assets at attractive valuations.

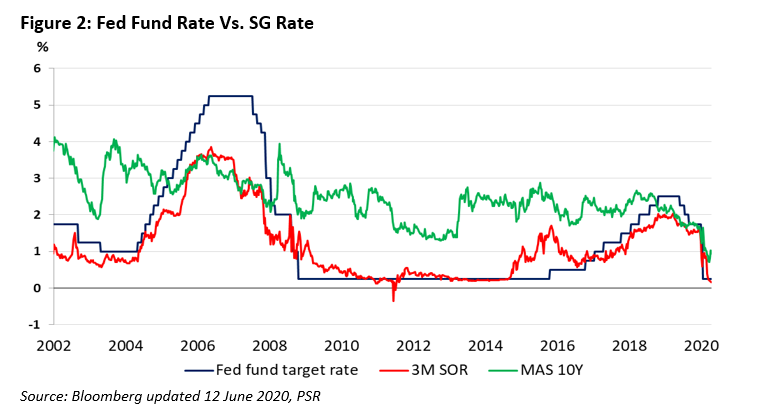

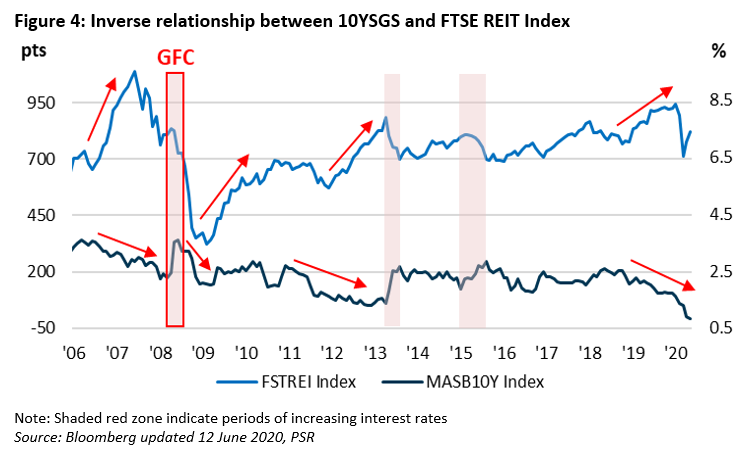

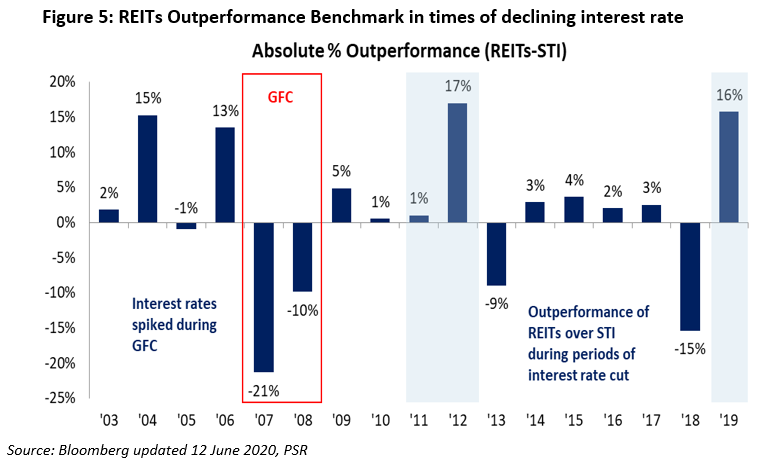

Historically, REITS have exhibited an inverse relationship with interest rates, with periods of declining interest rates leading to a strong price appreciation for REITs (figure 4) and the outperformance of the REIT index against the STI (figure 5).

No further extension of circuit breaker – gradual reopening of economy in three phases from 2 June 2020. While the lifting of the circuit breaker is positive, most retail, service and dine-in F&B will only be allowed to resume in Phase 2. According to the government, Phase 1 will see 75% of the economy resuming operations, with more Singaporeans allowed to go back to work. However, employees who can telecommute are advised to continue doing so. If community infection rates remain low and stable over two weeks, Singapore could enter Phase 2 before the end of June.

Rental Relief Framework for Small and Medium Enterprises (SMEs) may result in additional rental relief for commercial and industrial landlords and exacerbate arrears and cashflow mismatch. On 3 June 2020, the Ministry of Law introduced amendments to the COVID-19 Bill to enhance the relief for SMEs by way of:

According to Singstats, SMEs account for 99% of enterprises in Singapore in 2018, defined as companies with less the S$100mn in annual turnover recorded in 2019.

Through the Resilience and Fortitude Budgets, the Government will provide an equivalent of approximately 2 months of rent for qualifying commercial properties (interpreted as retail), and approximately 1 month of rent for industrial and office properties, which landlords must match. This mandatory rental relief by landlords affects Commercial and Industrial REITs more than Retail REITs as Retail REITs have already committed between 2 to 3.5 months out-of-pocket of rental waiver to tenants, while commercial and industrial REITs’ more targeted approach of offering selected tenants 0.5 to 1.5 months of rental waivers may results in rental waiver top-ups.

Up to 9 months rental arrears installment for tenants that qualify for landlord relief. SMEs that qualify for landlord relief may also elect to serve notice on their landlords to take up a prescribed repayment scheme for rental arrears accumulated from 1 February up till 19 October 2020. Upon serving the notice, tenants must start payment of the first instalment no later than 1 November 2020. Under the repayment scheme, tenants can pay for a specified portion of their arrears over an extended period of time (up to 9 months, or the remaining term of the tenancy, whichever is shorter) in equal instalments, with the interest payable on such arrears capped at 3% per annum.

INVESTMENT ACTIONS

Maintain OVERWEIGHT on the S-REITs sector

We continue to view REITs as a stable yield investment. We believe that SREITs may emerge stronger will more future-ready portfolios, resulting in a re-rating of the SREITs sector due to:

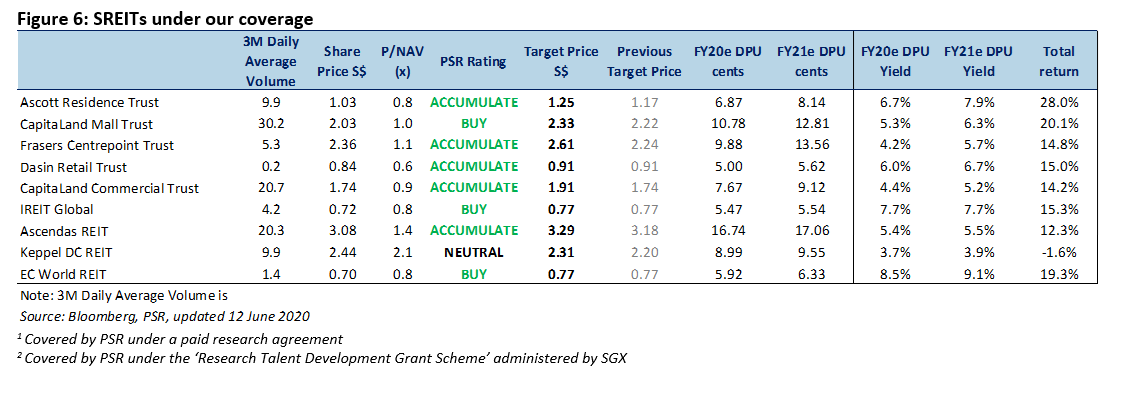

We revise our target prices for Singapore-focused REITs, ART, CMT, FCT, CCT, AREIT and KDC, incorporating a lower risk-free rate, as well as lower market-risk for the retail and commercial REITs. The changes in our target prices are summarised in figure 6.

Top-down view (unchanged)

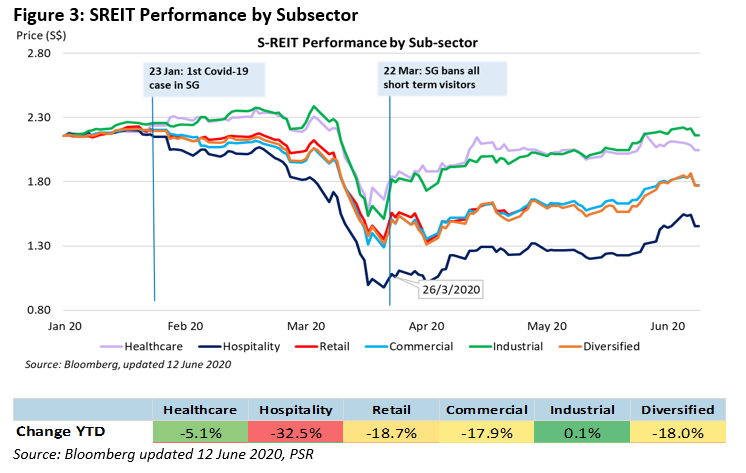

We like the Commercial and Industrial sub-sectors due to tapering office supply after the surge in supply in the prior two to three years, and the AEI and redevelopment opportunities for the Industrial sector. The tenants in these two sectors are also less affected by the COVID-19 outbreak. We are cautious on the Hospitality and Retail sub-sector due softer tourism sentiment and retail outlook, exacerbated by lingering fears of another wave of COVID-19 outbreak.

Tactical bottom-up view (unchanged)

REITs that can better weather through the rising interest rate environment would be those with:

1) Low gearing; 2) High-interest coverage; 3) Long weighted average debt to maturity; and

4) A high proportion of debt on fixed interest rates; 5) Higher percentage of guaranteed revenue through “fixed” or “stable” leases.