The positives

The negatives

Outlook

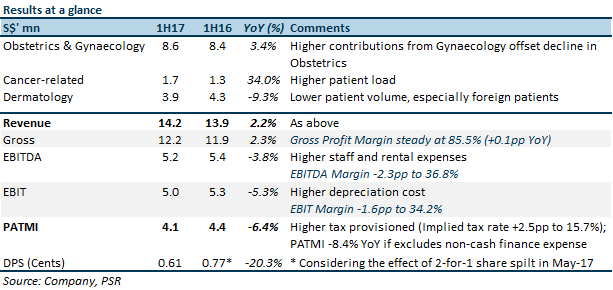

We are cautiously optimistic on the Group’s FY17e profitability. We are cognizant of the margin pressures arising from sluggish birth rate, slowing medical tourism, higher operating costs, and the latent period of the new Paediatric services.

Nonetheless, we remain upbeat of the Group’s ability to deliver organic growth. We deemed the slower obstetrics business in 1H17 to be a one-off event due to negative sentiment arising from an extraordinary event. We expect 2H17 a recovery in birth numbers in 2H17 as the adverse Zika effect subsides. In addition, historically, the second half has stronger performance compared to the first half. Meanwhile, SOG has ramped up marketing activities for dermatology products and services via its internal channels. New product development or successful marketing of existing products to drive greater profitability for Dermatology business.

The Group will add its second paediatric clinic in the heartland of Tiong Bahru estate by Nov-2017. The new paediatric specialist would be able to tap onto the potential young patient pool of over 4,000* babies and adolescents within the vicinity. (*Source: 2016 Population Trends, Singapore Department of Statistics)

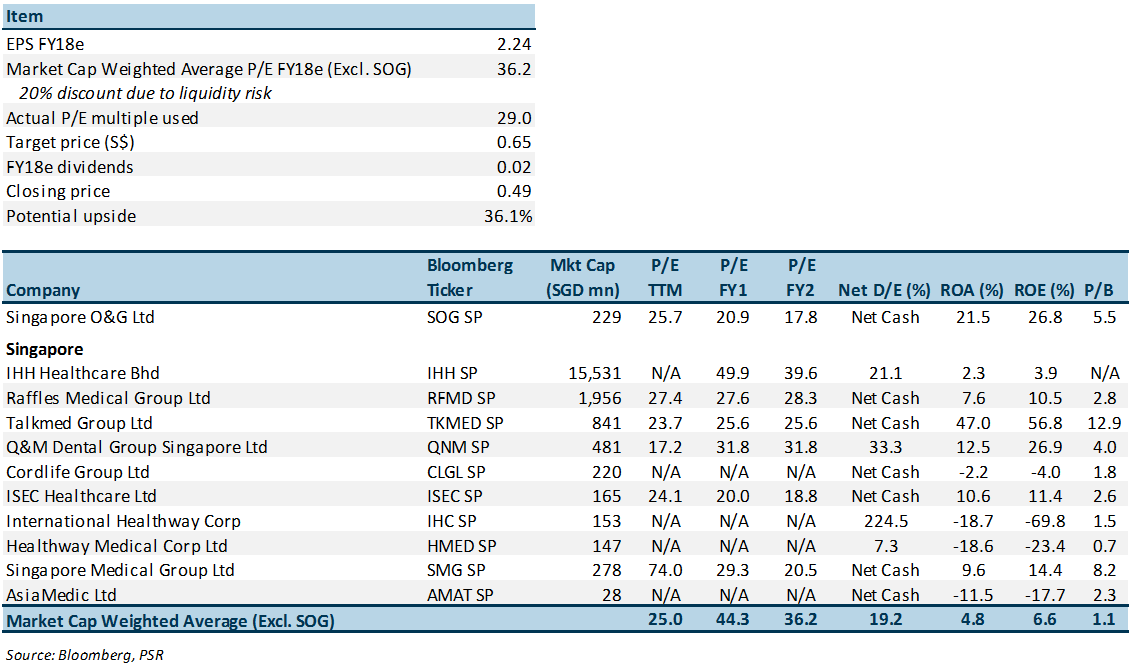

Upgrade to Buy with lower TP of S$0.65 (previously S$0.79) based on FY18e EPS of 2.24 SCents pegged to a lower forward PER of 29x.

We cut our FY17-18e revenue and earnings by 12% to 16% on slower patient load and margin pressures. These translate to a lower FY17-18e EPS of 1.84 SCents and 2.24 SCents. We believe that the stock has been oversold. SOG could ride through the headwinds with (i) its stable market position, and (ii) higher profitability from Cancer-related business. The Group has also been actively seeking for new recruits of medical practitioners to expand its four growth pillars. Its healthy financial position with zero debt and a war chest of S$17.65mn as at end-June 2017 enable the Group to pursue its expansion strategy, both organically and inorganically.

Potential re-rating catalysts:

Figure 1: Valuation

Dehong covers primarily the REITs and property developer sector. He has close to 7 years experience in equities related dealing and research roles.

He graduated with a Masters of Science in Applied Finance from SMU and Bachelors of Accountancy from NTU.