The Positive

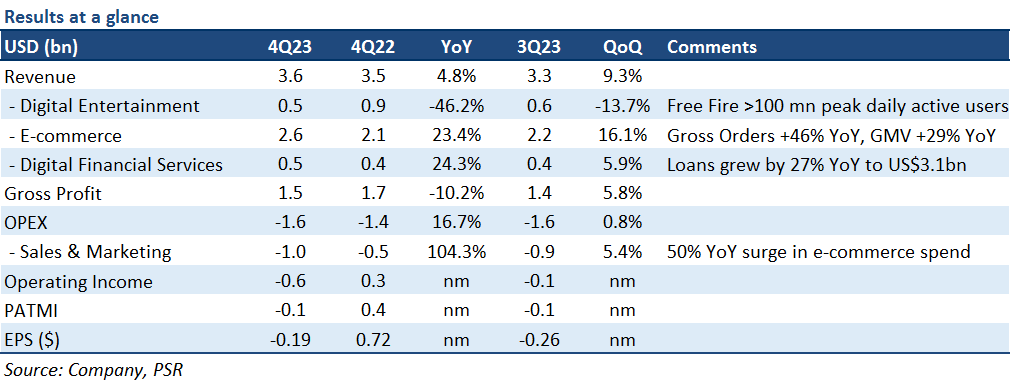

+ Investments in Shopee are paying off; gaining market share. Shopee’s strategic pivot to reinvigorate its topline growth through ramped up investment to competed aggressively for market share since July last year has paid off, helping Shopee gain more market share: there was a renewed surge in its GMV and gross orders (29%/46% YoY). Revenue grew 23% YoY in 4Q23. Shopee focuses on the expansion of last-mile delivery facilities and optimising routing, which cuts costs and improves delivery speed. Both market gain and improved logistics signal long-term growth for Shopee.

+ Shopee expected to see high-teens GMV growth in FY24e. Shopee has guided high-teens GMV growth YoY in FY24e as its investment in gaining market share starts to bear fruit. Its new initiative live-streaming e-commerce business continues to gain traction due to its leadership position and economics of scale. It now accounts for 15% of order volume by the end of FY23. SE claims to be making adjustments in take-rates, especially in ads, which has a sizable room to grow compared to global peers. SE has disclosed their confidence of returning Shopee to positive EBITDA in 2H24 even as competition picks up.

+ Gaming guidance is a pleasant surprise. Despite gaming continuing to show a 52% YoY revenue decline, SE has surprisingly guided a positive outlook for Free Fire. Both user base and bookings of SE’s largest and most profitable game are expected to increase by double digits in FY2024, indicating a rebound in gaming earnings after two years of decline.

The Negatives

– Nil.

Helena covers Hardware/Marketplaces/ETF. Helena graduated with a master degree in Financial Technology from Nanyang Technological University