SATS LTD – Focus on refinancing debt and managing costs March 4, 2024 183

PSR Recommendation: REDUCEStatus: Maintained

Last Close Price: 2.53Target Price: 2.31

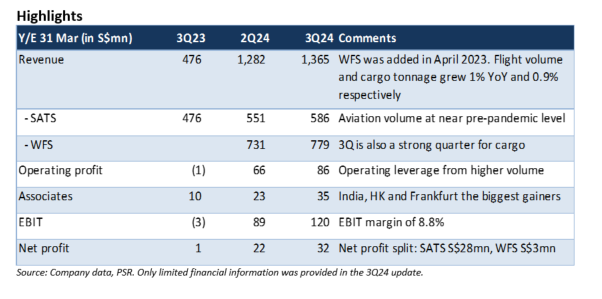

SATS reported 3Q24 net profit of S$31.5mn, which included S$3.1mn profit from WFS. The 9M24 net profit of S$23.7mn is in line with our FY24e estimates of S$66mn, before an estimated S$30mn amortization of intangible assets. The amount will be finalized in March 2024.

SATS group operations (excluding WFS) have nearly returned to pre-pandemic volume – flights handled was 86%, meals served, cargo handled and ground handling were 94% to 99% as of Dec 2023. Looking ahead, growth will be led by overseas operations in China, India and Indonesia, and lower interest costs through refinancing of debt. Net debt was flat QoQ at S$2.2bn, and net gearing was 0.9x.

Maintain our FY24e earnings forecast and REDUCE call. We raised our DCF-derived TP to S$2.31 (prev. S$2.23), as we roll over to the next financial year.

The Positives

SATS continued to improve on net profit by 45%, QoQ, due to continued recovery in air travel demand and 3Q being a seasonally strong quarter for aviation and cargo. Associates’ contributions improved, led mainly by India, Hong Kong, and Frankfurt.

The Negatives

3Q24 EBIT margin of 8.8% is still below the mid-teens level during pre-pandemic. The aviation industry has pressures from manpower crunch. With the inclusion of WFS, staff costs have risen by 241% YoY in 9M24 and now account for 60% of total expenditure (9M23: 49%).

Net debt is flat QoQ at S$2.2bn as at Dec 23. Of these, about €580mn (S$847mn) matures in May 2024 and needs to be refinanced.

3Q24 annualised ROE at 5.4%. This is dragged down mainly by WFS, contributed only S$3.1mn to 3Q24 net profit.

Subscribe

0 Comments

Inline Feedbacks

View all comments

About the author

Peggy Mak Research Manager PSR

Peggy has been a sell-side equity analyst for 22 years and a fund manager for 15 years.