The Positives

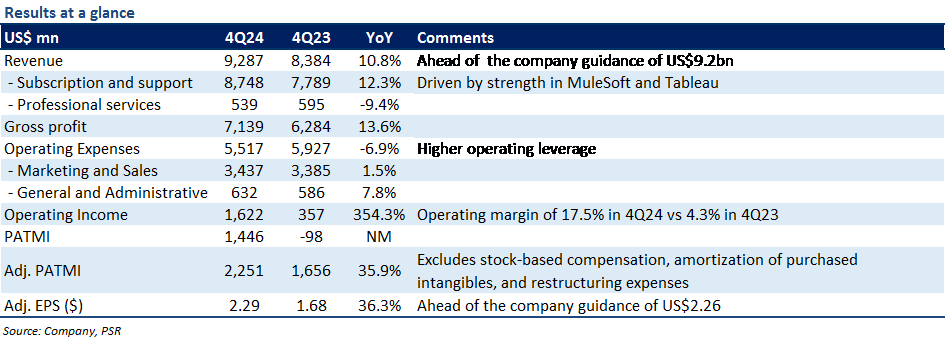

+ Multiproduct deals continued to drive growth. 4Q24 revenue grew 11% YoY (10% in constant currency) to US$9.3bn, 1% above the top end of company guidance, driven by higher subscription sales. On a product level, Sales/Service Cloud demand remained resilient with revenues growing by 10%/12% YoY to US$2.0bn and US$2.2bn, respectively. Integration and Analytics revenue delivered robust growth of 21% YoY to US$1.6bn, driven by strength in MuleSoft and Tableau offerings. Management highlighted that the number of large enterprise deals (those greater than US$10mn) grew by 78% YoY, with over 86,000 multiproduct deals. This was mainly driven by continuous product enhancements and its pricing and product bundling strategies. For instance, Salesforce Starter suite bundles Sales, Service, and Marketing tools together in one platform leading to significant surge in average sales price.

+ Margins continue to improve. Gross and operating margins expanded by 200bps and 1,300bps YoY, respectively. Operating income spiked more than 4-fold to US$1.6bn. The margin improvement was mainly due to top-line upside and higher operating leverage (OPEX down 7% YoY) from prudent headcount control and lower sales-related costs. In FY23, Salesforce cut jobs by 10% and closed some offices.

The Negative

– FY25e revenue guidance below our forecast. For FY25e, Salesforce expects total revenue to grow 9% YoY to US$37.9bn at the midpoint, which was below our estimate of US$38.6bn. This was because the company expects foreign exchange currency rates to negatively impact its revenues by US$100mn. In addition, Salesforce’s professional services business (revenue down 9% YoY in 4Q24) is expected to continue to be impacted due to the compression of larger transformation deals.