The Positive

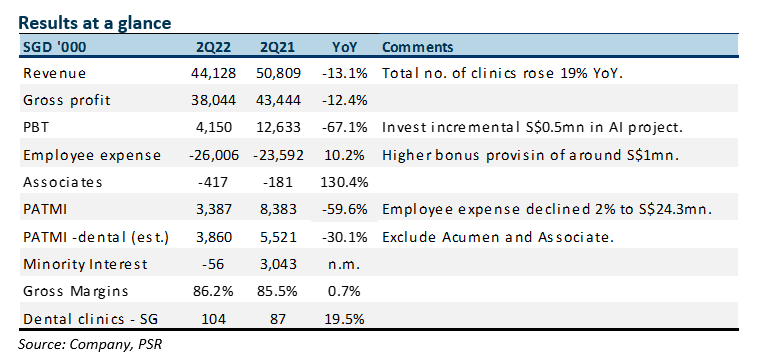

+ Surge in number of clinics. There were 8 new clinics opened in 2Q22. It is a 19% YoY jump to 149. 1H22 has seen the opening of 13 new clinics, tracking our modelled 25 new clinics this year. Headcount especially nurses is a major bottleneck in the expansion of clinics. Despite the rise in the clinics, revenue rose by only 5%. Revenue per average clinic has declined to 10% YoY to S$293k. We believe it will take time for new clinics to ramp up. Group utilisation rate is still at 60-70%.

The Negative

– Rise in expenses. 2Q22 staff cost and depreciation jumped by 12% YoY to S$30mn despite the decline in revenue. We attribute the rise in expenses due to additional $0.5mn spent on the AI project, $1mn in bonus provision and S$0.7mn in equipment. AI expense was higher than expected. Bonus provision is allocated evenly across each quarter compared to a lumpy 4Q recognition.

Outlook

Investment into Artificial Intelligence (AI) project will continue into 2H22. Revenue per clinic should improve as clinics mature. Further, the company aims to raise the utilisation of current chain of clinics by adding new dentists in existing clinics rather than adding new clinics. AI software has received approval as a Class B medical device. It is being rolled out across Q & M’s dental clinics to independently generate dental plans for patients. Next phase is to deploy to other clinics in Singapore. Acumen’s focus is on sepsis, colon cancer and pharmacogenetics screening.

Maintain BUY with lower TP of S$0.60 (prev. S$0.71)

2022 is a transition year as the company invests in the AI project, accelerates the roll-out of more clinics and Acumen pivots away from the COVID-19 PCR test to other test kits.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.