The Positive

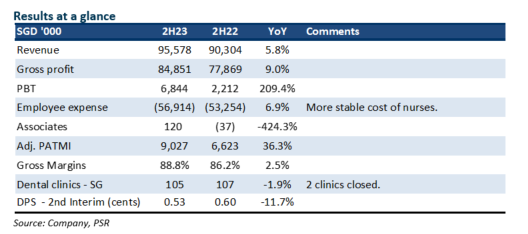

+ Recover in revenue and margins. 2H23 revenue growth is the fastest over the past two years. Despite fewer clinics, revenue expanded from higher revenue per patient. Using data driven treatment, Q&M can ascertain and provide a more intensive treatment for patients. Margins recovered from operating leverage and a stable number of staff or nurses.

The Negative

– Declining number of clinics. 2023 saw the first decline in the number of clinics in six years. Q&M closed two clinics in Singapore. The restructuring was to close loss-making clinics. Q&M is still looking to expand its clinics but for larger sites.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.