The Positive

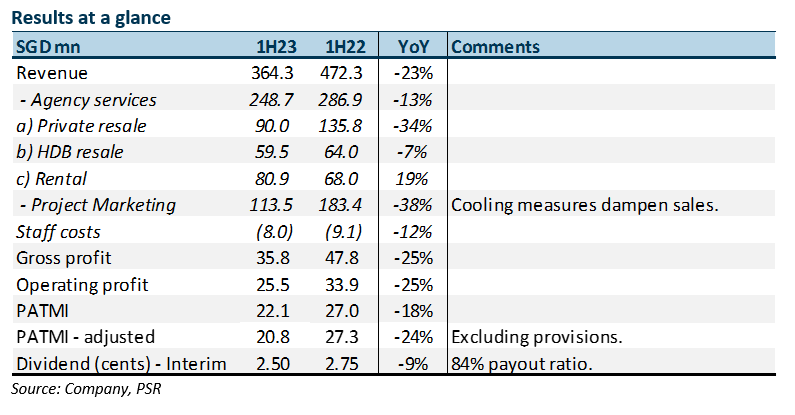

+ Returning the surge in cash-flow. The highly cash generative model was evident despite the weakness in earnings. FCF generated in 1H23 improved to S$30.0mn (1H22: S$23mn). Capital expenditure remained minimal at S$0.5mn. The net cash was generally stable at S$139.6mn (1H22: S$133.9mn). PropNex announced an interim dividend of 2.5 cents by raising the payout ratio from 75% to 84%. Our forecast dividends of 6.5 cents or S$48mn is well sustained by FCF and strong net cash balance sheet.

The Negative

– Weakness in revenue. Revenue contraction has been larger than expected. Weakness was especially in private new launches and resale. Lack of new launches over the six months 4Q22 till 1Q23 and softness in sentiment post cooling measures drove volumes down.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.