|

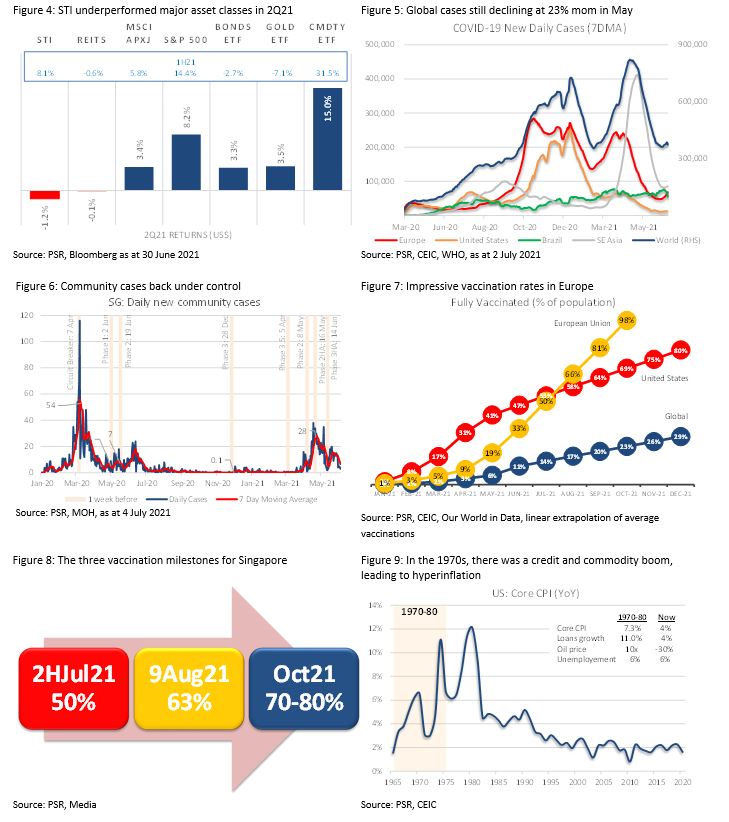

Review: After a sizzling 1Q21, the STI was back to its old penchant. The 1.1% contraction in 2Q21 led to its underperformance against major asset classes (Figure 4). Our bullish expectations did not pan out. After touching a high of 3,237 at end-April, the index succumbed to tighter social-gathering measures announced on 4 May. Restrictions were further tightened on 18 May, under Phase 2HA. Unlike the circuit breaker, the impact was narrowed to the entertainment, retail and service sectors as social interactions were limited to two and work-from-home again became the default. Sentiment nosedived on fears over another infection wave. During the quarter, a handful of mid-cap sectors did rally. Property agencies jumped as much as 58% on the back of a resilient residential property market. Malaysia-based iron-ore producers skyrocketed 65% as iron-ore prices spiked 40%. Outlook: We remain positive on equities. Unlike 6-12 months ago, vaccinations are underway globally (Figure 7). Visibility of normalcy is slowly appearing. Attitudes towards COVID-19 have also changed dramatically in Singapore. The disease is now considered endemic and managed like the common flu. We will not even be reporting daily infections soon but only patients in intensive care or requiring oxygen lifelines. A broad timeline has been laid out for a return to normalcy. Each milestone in vaccinations will lead to more community activities and eventually, an easing of border restrictions (Figure 8). The second half of July will mark the first milestone of full vaccination for 50% of the population. National Day is expected to be celebrated with a two-thirds achievement. The aim is to reach 70-80% by October. Travel between countries with rising vaccination and falling infection rates may be permitted without stay-home-notice requirements. The news cycle is almost daily dominated by inflation. Although U.S. inflation is climbing, we do not expect the hyperinflation of the 1970s (Figure 9). Economic conditions are vastly different this time. From 1970 to 1980, core CPI rose an average 7.3% p.a., from only 1.2% in the early 1960s. Accompanying the spike was a credit boom of 11% p.a., a 10x oil-price leap, trade union bargaining power and 6% unemployment. Today, U.S. loan growth is 4%, oil price is down a third from a decade ago and trade unions, hardly noticeable. Only unemployment is at similar levels. Without the threat of raging inflation, we expect the Fed to raise interest rates only in late 2023. Fed commentaries indicate a job-recovery priority over transient inflation. Our target for the STI is kept at 3400 (PER 16x forward). A 10% premium to a historical average of 14x, warranted in view of low interest rates and better earnings growth. |

Recommendation: Our strategy is to position for an aggressive relaxation of group activities and eventual border re-opening. The caveat for this is the country’s ability to meet vaccination rates for its population, vaccine availability and containment of vaccine-resistant variants. Sectors we favour include entertainment, hospitality and land transport. While we do not cover the entertainment sector, by year-end, we can expect cinema operations and concerts to return to pre-COVID arrangements. In hospitality, our preferred stock is Ascott Residence Trust. Around 30% of its assets are found in Europe and the U.S., where vaccinations and travel are picking up faster than the rest of the world (Figure 10). In land transport, ComfortDelgro is our pick. As work and social arrangements return, we expect a healthy recovery in earnings. Balance sheet has improved. Net cash rose from S$64mn in 2019 to S$279mn in 2020 (Figure 11). Lower capex, grants and a cash-generative business yielded free cash flows of S$377mn in 2020. Share price is down 30% from pre-COVID levels. We expect the stock to claw back some of its losses. Banking remains Overweight. We expect another leg in their rally from a recovery in loan growth (Figure 14), net interest margins and relaxation in the dividend cap. Building materials should profit from a resumption of construction work. Construction demand is expected to rise 20% this year (Figure 15), albeit from a low base.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.