The Positive

+ Leasing momentum doubled YoY with net effective rents improving 3.4%. MUST signed 654k sq ft, or 12% of NLA, in FY21, 2.3x the NLA executed in FY20. Traditional office tenants such as finance and insurance and government agencies accounted for 47% and 20% of leases signed. Reversions came in at -0.8% (FY20: +0.1%), weighed down by leases signed at Michelson. Michelson’s expiring rents were above market rents due to the 2-3% annual escalation on long leases, leading to negative reversions when the leases were renewed at market rates. Excluding leases signed at Michelson, reversions would have been +3.3% (FY20: +4.7%). More importantly, net effective rents grew 3.4% YoY, as the rent-free period and tenant incentives eased. While improving, net effective rents are still 10-15% below pre-pandemic levels. Leases signed in FY21 were for an average term of 4.0 years, slightly shorter than the 6.4 years for leases signed in FY20.

The Negative

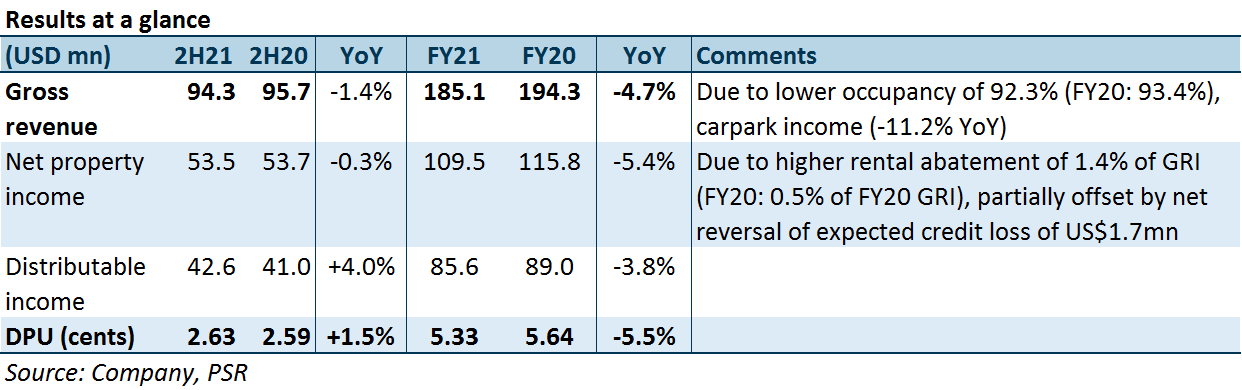

– Occupancy hurt by non-renewals and downsizing. Portfolio occupancy slid 1.1ppts YoY to 92.3%, 3.5ppts below FY19 levels. This compares with the average occupancy of 88.2% for Class A offices. Lower occupancy was due to non-renewals and downsizing with notable occupancy losses at Figueroa (-4.4 ppts), Penn (-5.4 ppts), Phipps (-5.5 ppts) and Capitol (-5.0 ppts).

Outlook

FY21 physical occupancy at MUST’s properties ranged from 25-30%. MUST provided rental abatement of US$2.4mn, or 1.4% of GRI, for F&B and retail tenants in FY21 (FY20: 0.5% of GRI). More pronounced return-to-office is expected to lift carpark income and lower rental abatement burden.

The US office market continues to show signs of recovery. This can be seen from (1) improving net effective rents; (2) lower TIs; (3) longer lease tenures signed; (4) decline in subleasing; and (5) improving rental growth outlook for MUST’s cities. About 8.1% of GRI is up for renewal. FY22 renewals could yield positive reversions, given that passing rents are 2.1% below market rents.

Future acquisition is still focused on markets with high representation of tech, healthcare and life science tenants. MUST is eyeing assets with cap rates ranging 6.5% to 7.5% in sunbelt and magnet cities — Seattle, Salt Lake City, Austin, Boston, and Raleigh. Following the acquisition of three properties in Phoenix and Portland in Dec21, MUST’s exposure to tech and healthcare tenants increased from 9.5% to 12.8% of GRI. It hopes to increase its exposure to new economy tenants to 20% of GRI.

Upgrade from Accumulate to BUY, DDM TP raised from US$0.84 to US$0.86

FY21 occupancy came in lower than we anticipated. As such, we lower FY22e-24e DPUs by 2.1-6.3% to factor in the gradual recovery in occupancy from the current, lower-than-forecasted portfolio occupancy. DDM-TP rises due to higher later-period DPU forecasts. The US office market appears to be at an inflection point, showing recovery in leasing momentum. Catalysts include stronger-than-expected leasing and portfolio reconstitution. Current share price implies FY22e/FY23e DPU yield of 8.6%/8.9%.