Keppel DC REIT (KDCREIT) offers investors access to a unique asset class of data centres. Underlying growth drivers come from the explosive growth in data creation and data storage needs. Newly acquired Milan DC, Cardiff DC and KDC SGP 3 to bolster gross revenue growth by 30% in 2017. However, geographical diversification also introduces country risk and currency risk exposure.

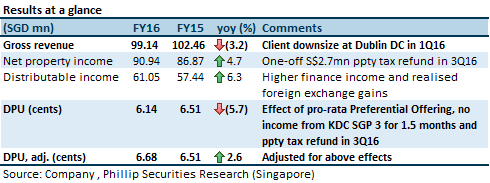

FY16 DPU missing the Street’s expectations was not due to portfolio weakness

In fact, the manager reportedly signed a major 5-year lease at approximately 3% higher than the preceding rent. While the headline FY16 6.14 cents DPU appears to have missed the Street’s expectations of 6.60 cents, we believe this is nothing to be alarmed. 3QFY16’s DPU of 1.90 cents was not distributed and was likely not adjusted by the Street to account for the Preferential Offer in 4QFY16. KDCREIT makes distributions on a half-yearly basis, so the new Preferential Units created in 4QFY16 are also entitled to 3QFY16’s distribution for the 2HFY16 distribution. Had the Street made the adjustment, consensus expectations would have been closer to 6.19 cents, in line with the actual 6.14 cents declared.

Income visibility from limited vacancy risk for the next four years

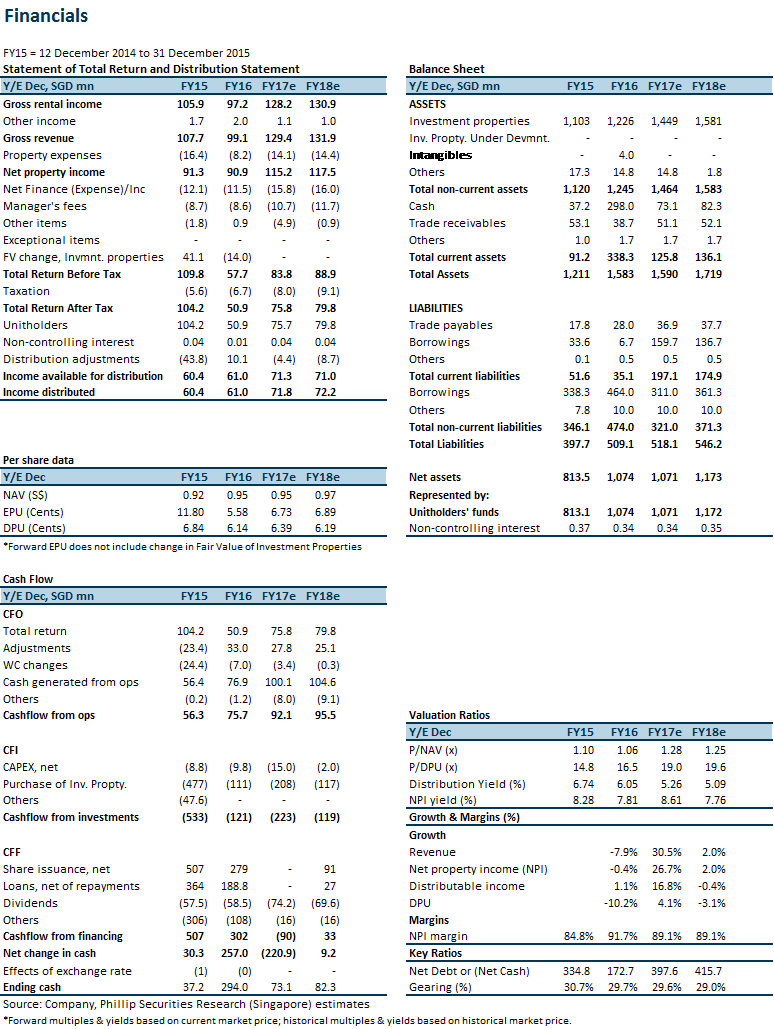

Lease expiry profile for 2017, 2018, 2019 and 2020 stands at 14.6%, 0.6%, 2.1% and 1.6% respectively of by leased lettable area. Vacancy risk in 2018 to 2020 is negligible, in our view. 2017 expiries come from four leases expiring in 1H2017. The manager has already come to in principle agreements with three of the tenants to renew (one in Singapore and two overseas), and is in the final documentation stage. The fourth lease is from the Basis Bay full-fitted lease, which accounts for 5.4% of portfolio lettable area.

Income stability from limited foreign currency and interest rate uncertainties

As a reminder, KDCREIT’s foreign currency policy is to hedge its expected foreign currency cash flow two years out. As such, the manager has already hedged forecasted foreign cash flow up to the end of 2018. Interest rate exposure has been mitigated by fixing 83% of borrowing costs; only 17% remaining floating. Only 0.7% of debt matures in 2017, but we expect to see some debt refinancing activity this year, as the manager tackles the 34.9% of debt maturing in 2018.

Downgrade to “Neutral” rating with lower target price of S$1.15 (previous: S$1.26)

As the portfolio has increased its exposure to Western Europe, we have included a country risk premium component into our cost of equity estimate, but increased our terminal growth assumption. We believe that the attractiveness of the asset class has been adequately priced in. Our target price is 1.21x FY17e P/NAV.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.