The positives

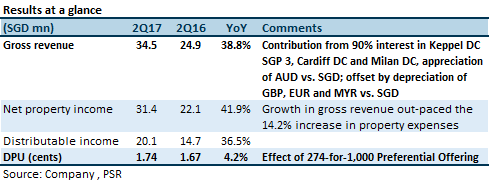

+ YoY growth in gross revenue driven by inorganic growth: 90% interest in Keppel DC SGP 3 acquired in January 2017, Cardiff DC and Milan DC both acquired in October 2016.QoQ longer weighted average lease expiry (WALE) from 9.2 years to 9.4 years: Client at Basis Bay Data Centre in Malaysia renewed the lease for another five years.

+ QoQ longer weighted average lease expiry (WALE) from 9.2 years to 9.4 years: Client at Basis Bay Data Centre in Malaysia renewed the lease for another five years.

+ Aggregate leverage of 27.7% is among the lowest in the S-REITs universe: This affords a debt headroom of ~S$300 million (based on 40% aggregate leverage), potentially growing the portfolio by ~20%.

The negatives

– QoQ lower occupancy from 95.1% to 93.1%: Client at Basis Bay Data Centre only renewed two of the three data centre floors. However, limited impact to the portfolio, as Basis Bay Data Centre contributes less than 3% of FY17e gross revenue, by our estimate. The manager will start marketing the vacant floor soon.

– Keppel DC Dublin 1 is still under-utilised: Occupancy is 56.3% and we believe it will continue to be challenging to find tenants to take up the remaining space until the power supply has been upgraded. S$15 million upgrading works are scheduled to commence and complete in 4Q 2017. After which, we believe the data centre will be more attractive to prospective tenants, and should be easier to backfill.

Outlook

The outlook remains stable. The two remaining major leases that are due for expiry in 2017 have been agreed in-principle and are pending finalisation of lease documentation. However, 3Q17 DPU could be lower YoY, as there was a one-off distribution of 0.23 cents arising from net property tax refund in 3Q16. It has been a dry spell in terms of acquisitions in 1H 2017. Any pick up in deals in 2H 2017 would be a favourable development to drive inorganic growth.

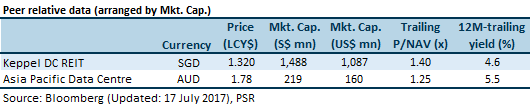

Maintain Neutral with higher target price of $1.28 (previous $1.15)

We raised our FY17e/FY18e DPU forecast by 3.5%/6.0% as we tweak our revenue and property expenses assumptions. Our target price represents an implied forward 1.35x FY17e P/NAV.

Relative valuation

KDCREIT is relatively over-valued in terms of trailing P/NAV, in comparison to its Australia Stock Exchange (ASX)-listed peer, Asia Pacific Data Centre.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.