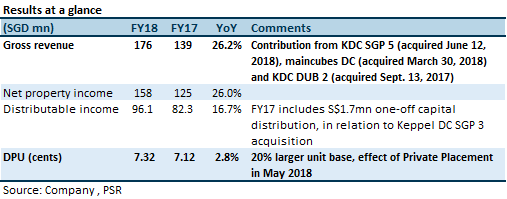

The Positives

The Negatives

Outlook

The outlook is positive. Data centre demand remains robust, underpinned by increasing cloud adoption, rapid digital transformation, data centre outsourcing and data sovereignty regulations. The Manager achieved the S$2bn AUM target set for 2018 but does not have a new target for 2019. The Manager articulated that it intends to maintain the pace of acquisitions. However, we think the pace could be hampered by tightening capitalisation rates. The Manager commented on the difficulty in finding assets to buy with a limited deal flow, as owners are holding on and not willing to sell. The asking capitalisation rate for those prepared to sell are very tight.

Maintain ACCUMULATE; new target price of $1.52 (previously $1.45)

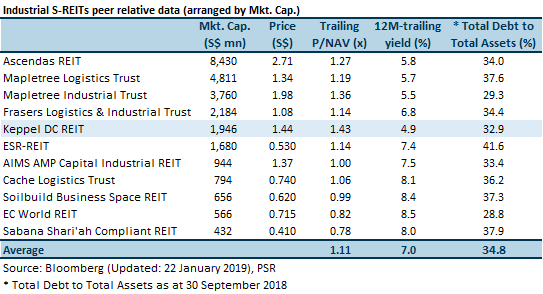

While the long-term demand drivers for data centre remains intact, downside risk may arise from the rich valuation with the implied 1.37 times FY19e P/NAV multiple.

Relative valuation

KDCREIT trades at a higher P/NAV multiple compared to other listed S-REITs. We believe this is a reflection of the burgeoning demand for the unique asset class of data centres.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.