The Positive

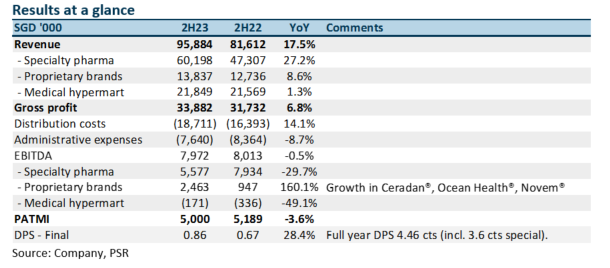

+ Rebound in specialty pharma revenue. Despite the loss of Biosensor’s S$5mn revenue contribution in 2023, revenue in 2H23 rose 27% YoY to a record S$61mn. The addition of new specialty products, namely Laboratoires Gilbert S.A.S, drove growth in the export sector. Revenue from other countries (Indonesia, Phillippines) tripled in 2H23 to S$13.7mn.

The Negative

– Weaker gross margins and higher opex. EBITDA margins declined 1.5% points YoY to 8.3% in 2H23. We believe a combination of higher export sales, an increase in headcount costs and additional expenses from DocMed drove down margins.

Outlook

Investments in a larger management team has resulted in more aggressive expansion in principals, products and distribution. We believe Hyphens is on a faster growth trajectory:

Maintain BUY with unchanged TP of S$0.35

Hyphen enjoys a dividend yield of 4% and trades at a PE ratio of 7x FY24e.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.