The Positive

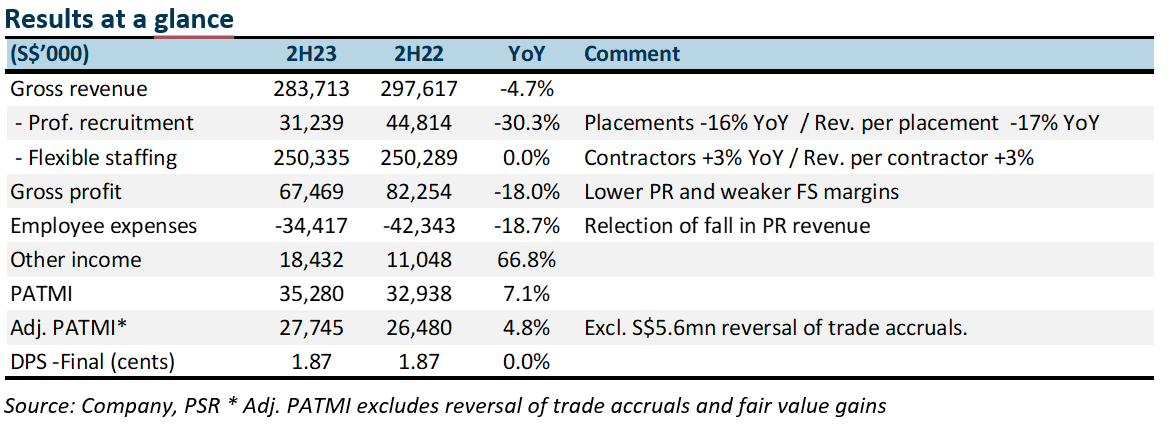

+ Flexible staffing (FS) is the key performer. Around 94% of FS revenue is from Singapore. 2H23 FS revenue in Singapore rose 1.8% YoY. Despite the decline in number of contractors, the rise in wages supported revenue. Government policy to drive up wages of the lower income also pushed income from government subsidies to S$6.6mn in 2H23 (2H22: S$1.2mn).

The Negative

– Professional recruitment (PR) is still the weak spot. The number of PR hirings in 2H23 fell 17% YoY to 2,856, due to hiring freezes and cautious sentiment. Revenue per placement declined 17% YoY as more placements were completed for junior roles.

Outlook

We are forecasting a 5% contraction in volumes for PR. There are limited indications corporates are ramping up their hiring of managerial roles in this region. FS revenue is expected to grow stronger from higher wages and improvement in volumes especially in Taiwan. The FS operations in Taiwan is beginning to hit scale and gain more traction with corporates.

Maintain BUY and lower TP of S$0.85 (prev. S$0.88).

HRnetGroup enjoys net cash of S$303mn with barriers of scale with more than 500 full-time recruitment consultants across 17 cities. There is another S14mn outstanding in their committed share buyback programme.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.