The Positives

+ ASPs for main China development projects maintained despite cooling measures: HBL continued to make sales progress on their residential projects in China despite cooling measures, with prices maintained or higher. Average transacted prices for Yanlord Western Garden, Shanghai (HBL’s biggest project in China) for example are at now at RMB60k/sqm, up 13% from start of the year.

+ Recurring income office portfolio remains stable: The Metropolis at Buona Vista, a Grade A suburban office tower which takes up 38% of HBL’s total GAV maintained a near 100% occupancy going into its second rent renewal cycle since operating in 2013. Average passing rents have held stable YoY at S$7+/psf.

The Negatives

– Price and transaction volume pickup for residential properties in Core Central Region not yet translating to Sentosa condominium market: HBL’s 3 condominium projects in Sentosa remains held for lease and occupancy is around 80% currently. We believe market conditions there have not picked up significantly enough for management to consider other monetization options.

Outlook

HBL’s local and overseas rental properties (66% of total GAV) provide stable recurring income for the Group. We expect the Group’s Singapore office portfolio to benefit from a recovery in office rents. Their London office properties are mostly on long leases of 5-10 years with built in rental escalations which would enable it to ride out Brexit uncertainties in the short term. Buying activity for Sentosa Cove bungalows have improved this year with the highest volume transacted since 2013. While still not evident in the Sentosa condominium market, we expect interest and transaction volumes to gradually return to the overall high-end market due to 1) lack of supply 2) increasing cooling measures implemented in other countries 3) widening price gap with other top cities over the years and narrowing price gap vs suburban (Sentosa condos have fallen 50% from peak). This will benefit the Group’s 3 Sentosa condominium projects held for lease currently.

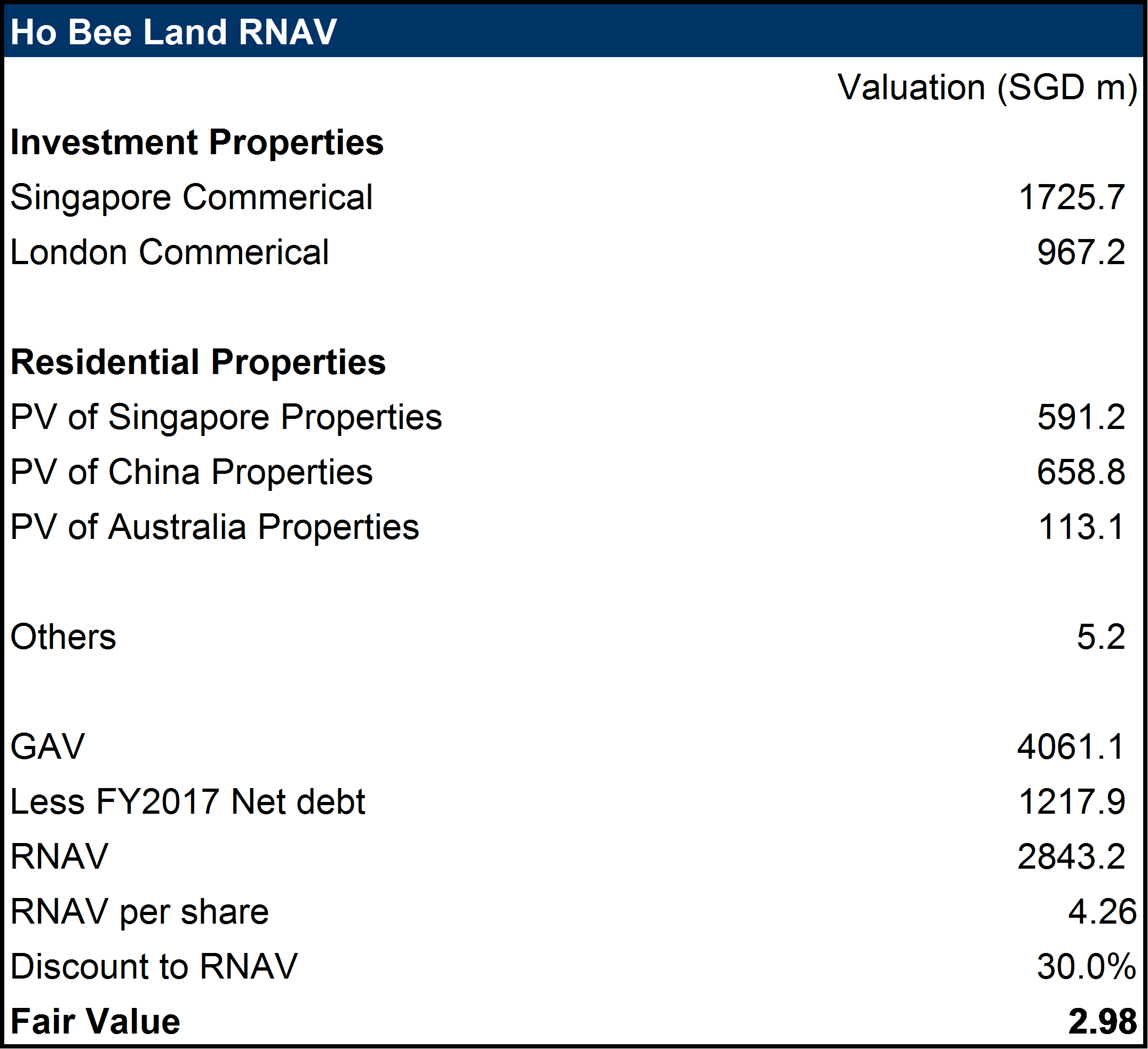

Maintain ACCUMULATE with unchanged RNAV-derived target price of S$2.98.

HBL trades at one of the largest 42% discount to NAV amongst the large cap property developers (Figure 3). We expect the discount to narrow as interest and transaction volumes gradually return to the high-end market in Singapore. Recurrent income is around S$180mn per year, sufficient to cover 3.8x their present S$47mn dividend per annum.

Figure 1: RNAV Table

Figure 2: HBL trades at below post-GFC P/NAV

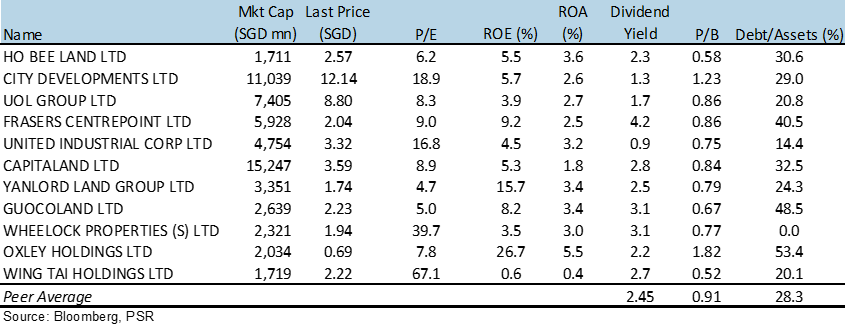

Figure 3: Peer Comparison – HBL and Wing Tai trade at the largest discount to RNAV amongst large caps

Dehong covers primarily the REITs and property developer sector. He has close to 7 years experience in equities related dealing and research roles.

He graduated with a Masters of Science in Applied Finance from SMU and Bachelors of Accountancy from NTU.