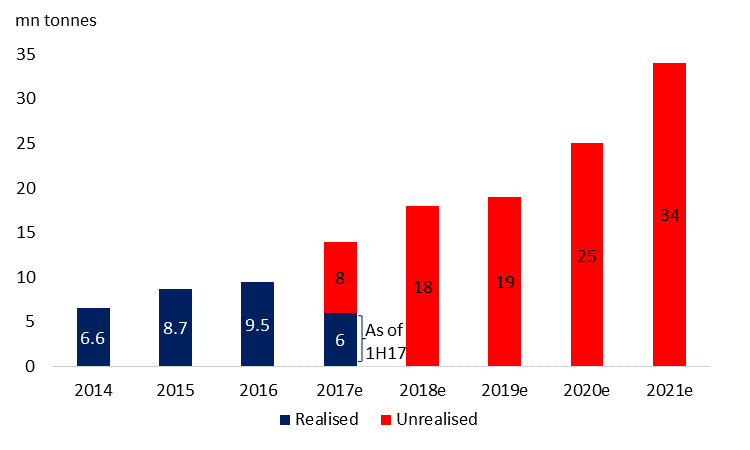

In FY16, GEAR produced 9.5mn tonnes of coal, out of which 7.5mn tonnes and 2 mn tonnes were from BIB mine and KIM mine respectively. As of 1H17, the group completed 43% of the FY17 target production of 14mn tonnes (BIB: 12mn tonnes, KIM: 2 mn tonnes). GEAR longer-term target is to more than triple production in five years to 34m tonnes in 2021.

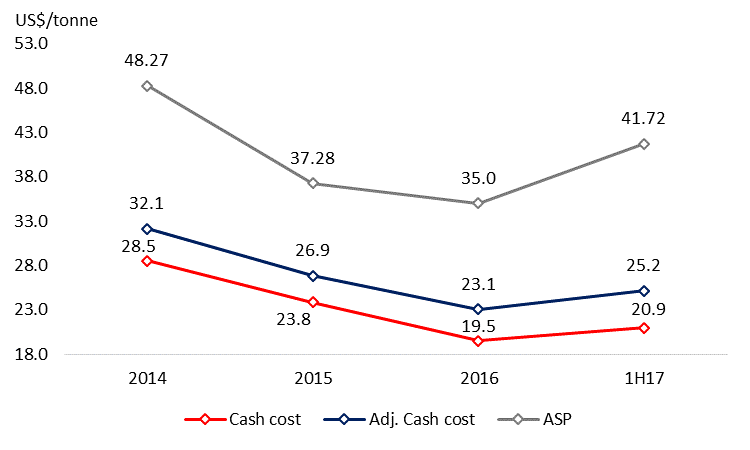

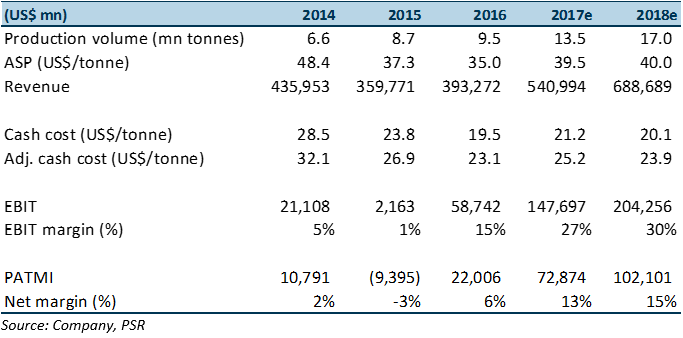

The average life-of-mine strip ratio of BIB mine (key mine) is estimated at 4.1. In FY16, the average cash cost and ASP were reported at US$19.5/tonne and US$35.0/tonne respectively. As of 1H17, the cash profit (ASP minus cash cost) was reported at US$20.8/tonne. The average cash cost for FY17e and FY18e is estimated to be US$21.2/tonne and US$20.1/tonne. Industry cash cost is around US$40-50/tonne.

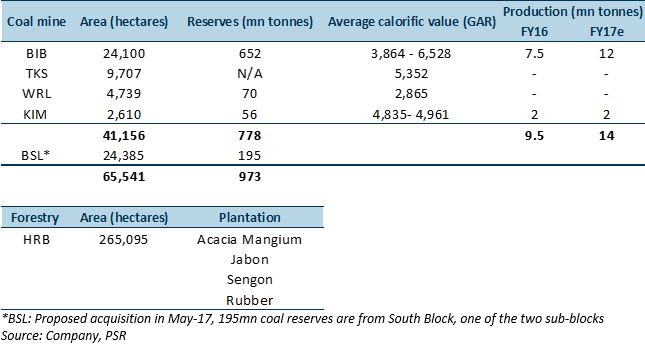

Currently, GEAR owns four key coal mining concessions and large total reserves of 778mn tonnes. In May-17, the group proposed to acquire a mine, BSL. Upon the completion of the acquisition, the total reserves are estimated to be 993mn tonnes.

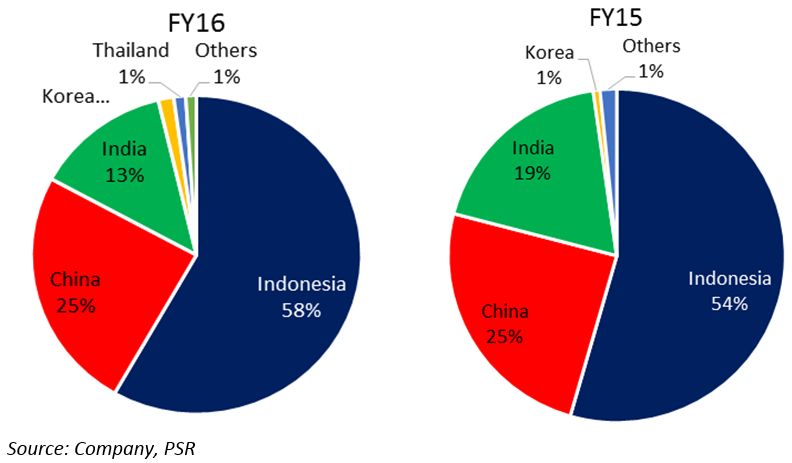

The domestic market took up more 50% of the coal sales in FY15 and FY16 respectively, followed by China (>20%) and India (>10%). The group is aligning the production with the rising domestic coal demand as well as complying with policies that prioritise coal for domestic needs.

Background

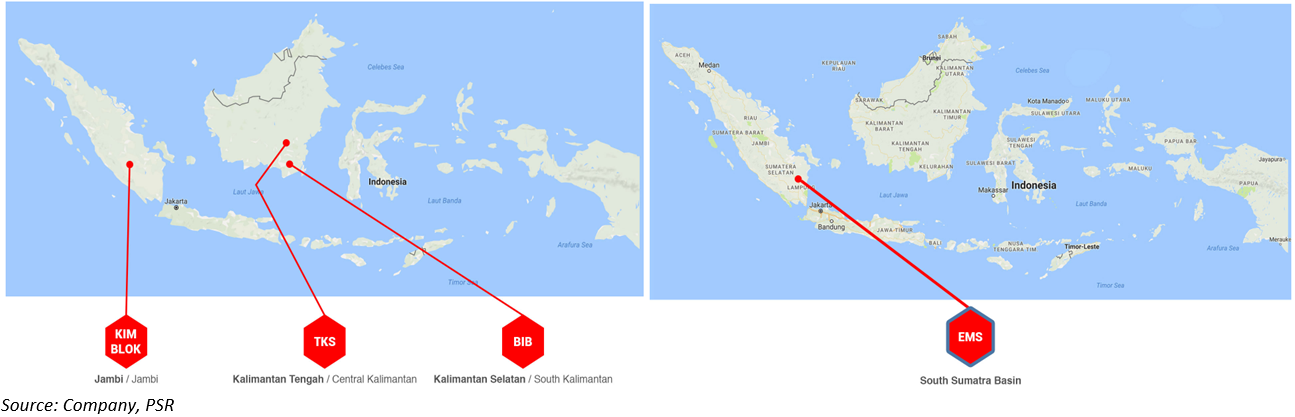

Golden Energy and Resources Limited is the largest coal producer listed in Singapore. The Company sources thermal coal from its coal mining concession areas, covering an aggregate of approximately 42,904 hectares in South and Central Kalimantan, Jambi (a province in Sumatra), and South Sumatra Basin Indonesia.

Investment action

Based on FY18e EPS of 4.34 US cents and a forward PER of 10x (USD/SGD 1.36) we derive our target price of S$0.59. This implies an upside of 32.6% from the last closing price.

Investment Merits

Currently, GEAR owns four key coal mining concessions, namely PT Borneo Indobara (BIB), PT Trisula Kencana Sakti (TSK), PT Wahana Rimba Lestari (WRL), and PT Kuansing Inti Makmur (KIM), shown in Figure 23. As of Dec-16, reserves excluding TKS’s arrived at 778mn tonnes. Together with PT Barasentosa Lestari (BSL) which the Group proposed to acquire in May-17, total reserves under GEAR reach 973mn tonnes. It is able to support GEAR’s development for more than 40 years provided the production will be maintained at 20mn tonne per annum. Coal produced in the BIB mine has a wide range of calorific value (CV), meaning that coal supply from the mine caters to both power generation (low CV coal demanded) and metallurgy (high CV coal demanded). Diversity in coal grades enables the group to buffer the impacts from the cyclical fluctuation of coal demand since electrification is not necessarily correlated with a metallurgical boom.

Furthermore, GEAR owns a broad field of forestry resources, and the concession of which is held by PT Hutan Rindang Banua (HRB). The listed plantations as consumer products will cater to demand from growing domestic middle class. Though pulp log sales are trivial in terms of revenue contribution as of now, there are a lot of untapped resources awaited to be utilised. For instance, 13,523 ha of land have land rent-use right, representing areas of overlapping mining permits with third parties who have encroached onto the group’s forestry concession land to carry out mining activities. In other words, GEAR will receive compensation from these third parties as an extra income.

Figure 23: Coal and forestry reserves

Figure 24: Locations of the existing mines

2. Diversified sales channels lower geopolitical risks

GEAR sells coal to multiple countries across Asia. Amongst all, shown in Figure 25, China is the biggest coal export market, followed by India. Korea, Thailand, Malaysia, Singapore, UK, and Philippines purchased coal from GEAR though revenue from them accounts for less than 5%. Domestic coal sales increased by 4ppt to 58% in FY16 in Indonesia which remains a major market for GEAR’s coal.

Diversified sales channels are an important stabiliser to the group. As we mentioned above, coal trading is substantially sensitive to government policy changes wherever it occurs in the domestic or overseas market. For GEAR, shifting it target market is critical as it captures this next wave of coal consumption. In other words, the group is aligning the production with rising domestic coal demand as well as complying with policies that prioritise coal for domestic needs. Therefore, more than close to 60% of the turnover is sheltered with a promising demand. Indonesia coal is still in demand in both China and India for a relatively long period in the future. However, both governments, who mediate between internal supply and external import, prioritise interests of domestic coal producers undoubtedly. Hence, geopolitical risks such as banning coal import and levying higher customs exist constantly. Maintaining respective China and India a relatively small portion of coal sales buffers the group when policies turn.

Figure 25: Revenue breakdown by geographic locations

3. Significant ramp-up of production volumes

Shown in Figure 26, in FY16, GEAR produced 9.5mn tonnes of coal, out of which 7.5mn tonnes and 2 mn tonnes were from BIB mine and KIM mine respectively. As of 1H17, the group completed 43% of the FY17 target production of 14mn tonnes (BIB: 12mn tonnes, KIM: 2 mn tonnes). Moving forward, GEAR aims to achieve 34mn tonnes of production by 2021, and more importantly, the plan only takes BIB mind and KIM mine into account. Outputs from the rest mines, especially the recent being acquired (BSL), will be icing on the cake. Therefore, it is expected to realise production expansion in the near term.

Figure 26: Production visibility till 2021

Source: Company, PSR

4. Low mining cost and strip ratio

As of 1H17, GEAR’s coal production was mainly from BIB mine where average life-of-mine strip ratio is estimated at 4.1 (4.1 tonnes of overburden are removed to extract 1 tonne of coal). The low rate level results in low production cost, shown in Figure 27. The gap between cash cost (Adj: adjusted) and average selling price (ASP) has been widening, because coal price bottomed out in 2016 while operating expenditures only grew mildly. ASP tracks the volatile International coal price which is beyond company’s control, but mining costs are comparatively stable. Low cash cost benefits GEAR in two ways, enhancing profit margin when ASP soars and buffering the downturn when ASP collapses, and the latter merit is important for sustainable growth in the long term.

Figure 27: Low cash cost on a downtrend

*Cash cost: including COGS & selling expenses; excluding royalty fees

**Adj. Cash cost: cash cost including royalty fees

Source: Company, PSR

How do we view GEAR

The outlook for GEAR is bright. In the short-term, it will ramp up production capacity to take advantage of favourable macro conditions, including a boom in domestic electrification as well as coal price recovery. Within the next couple of years, we are positive that the group is able to deliver stable growth. In addition, GEAR also benefits from diversification of end-customers as well as trading partners, which lower the geopolitical risks and trading risks. In a long-term view, the mining operation is backed by abundant coal reserves that reach approximate billion tonnes once the acquisition of BSL mine is completed. The total reserves are expected to support the ongoing production for several decades if GEAR produces 20mn tonnes per annum. Moreover, the average life-of-mine strip ratio for BIB mine, the key mine as of now, is low, resulting in low mining costs that provide more room for the profit margin.

Key assumptions

Figure 28: Key variables assumption

Valuation Methodology

Based on FY18e EPS of 4.34 US cents and average 12-month forward PER of 10.0x, as well as USD/SGD exchange rate of 1.36x as the FX rate, eventually, we derive our target price of S$0.59 for FY18, which implies an upside of 32.6% from the last closing price.

(This report is part of the Coal Sector report published on the same day.)

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Guangzhi graduated from Singapore Management University with a Master degree in Applied Finance and from South China University of Technology with a Bachelor degree in Electronic Commerce.

The current sector coverages include Energy, Utilities, and Mining sectors. He has 3 years experience in equity research in both Hong Kong and Singapore market. He is the mandarin spokesperson for Phillip Securities Research in relation to China-related projects and all mandarin seminars and client events.