Executive Summary

30% downside for the U.S. Dollar

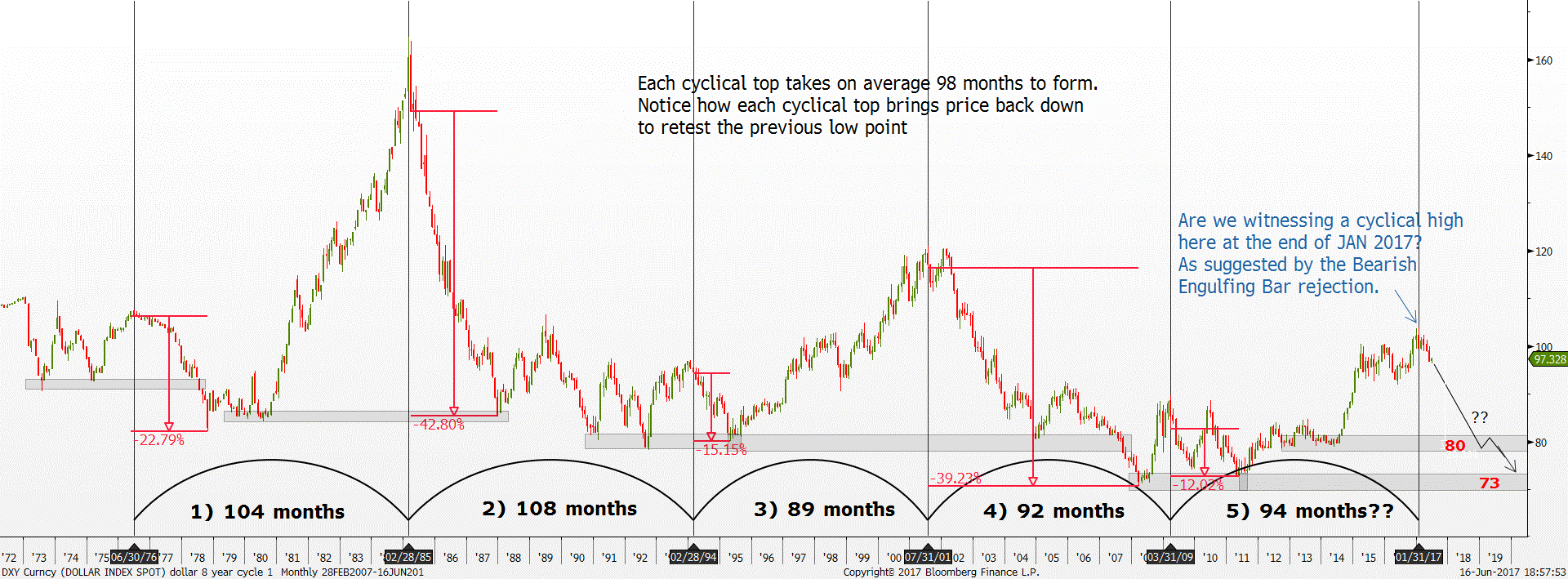

As suggested in a previous report by our technical analyst, we believe there is still room for the USD to fall. In summary, the dollar index (DXY) has reached a 98 months cyclical top in January 2017. A massive selloff of 12% to 42% will usually follow after the cyclical top.

Figure 1: 98-month cyclical top is formed, calling a 30% downside in DXY

Source: Bloomberg

DXY: The US Dollar Index is an index of the United States dollar relative to a basket of foreign currencies, mainly against the Euro, Japanese Yen, Pound Sterling, Canadian Dollar, Swedish Krona and Swiss France.

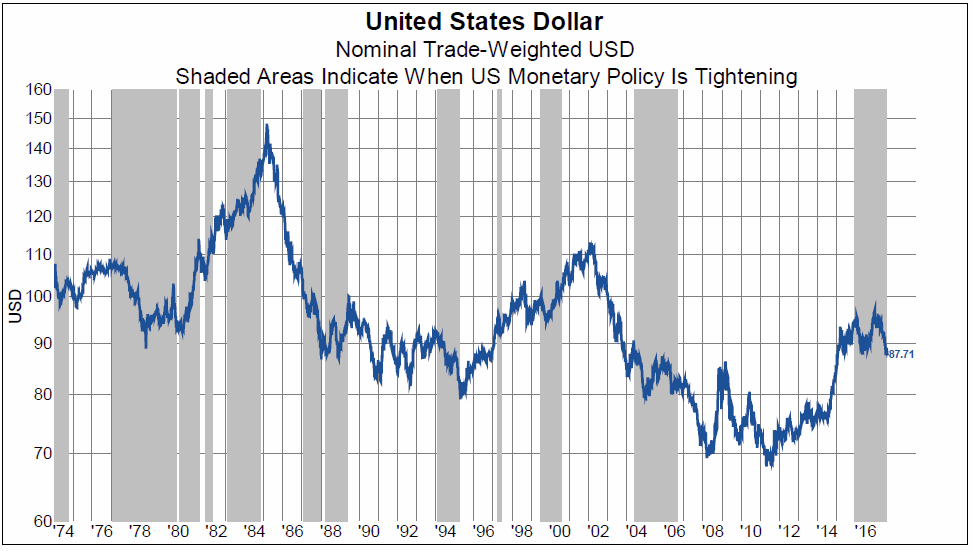

Tightening monetary policies don’t necessarily support a strong USD

There is a common misperception that the USD will strengthen as the Federal Reserve (Fed) embark on a tightening monetary policies regime. However, history dispels this misconception as shown in Figure 1. USD movement is not consistent with monetary policies but relates more to U.S. aggregate saving and the confidence in its current Administration.

Figure 2: U.S. dollar behaviour is de-linked most times from monetary policy

Source: Knowledge Leaders Capital, LLC

Loss of confidence in the U.S. Dollar

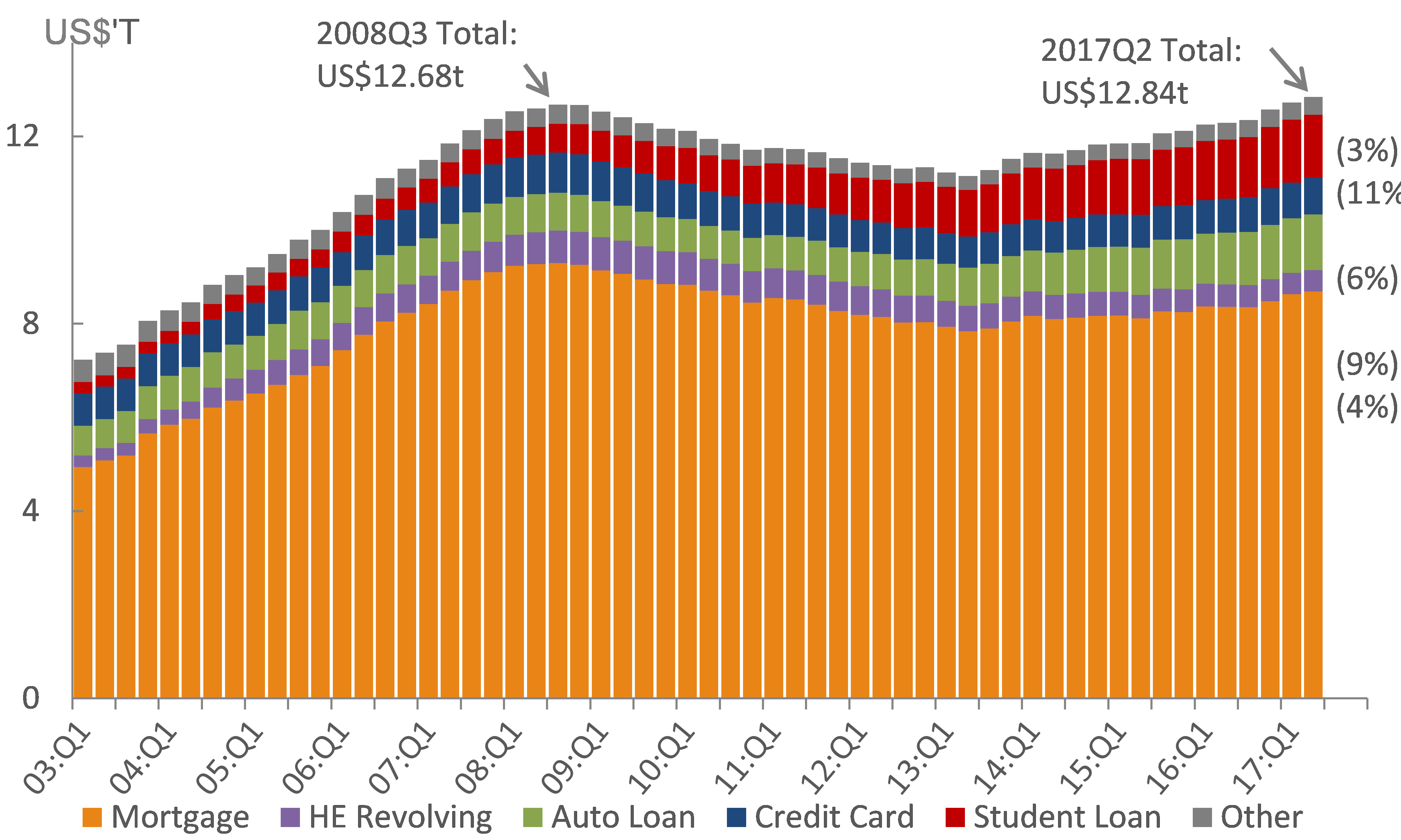

We believe that the loss of confidence in the dollar is structural and this might mark the end of the U.S. dollar hegemony. As of today, U.S. has never been more leveraged than any point in their history. The private household debt and the national public debt are at record high, easily surpassing the historical high of the Great Financial Crisis (GFC) in 2008.

Although total mortgage loans were pared down briefly during the years after the GFC, other non-housing debts have started to gain traction. Auto loan debt, student loan debt and credit card debt have reached unpreceded record size. However, unlike mortgage loans which have the underlying property as collateral, auto loan, credit card debts and student debts are unsecured debt. This means that there will be no salvage value if these unsecured credits were to default.

This debt overhang handicapped the U.S. economy from expanding through further credit expansion.

Figure 3: Total Household Debt back above 2008 high

Source: New York Fed Consumer Credit Panel/Equifax

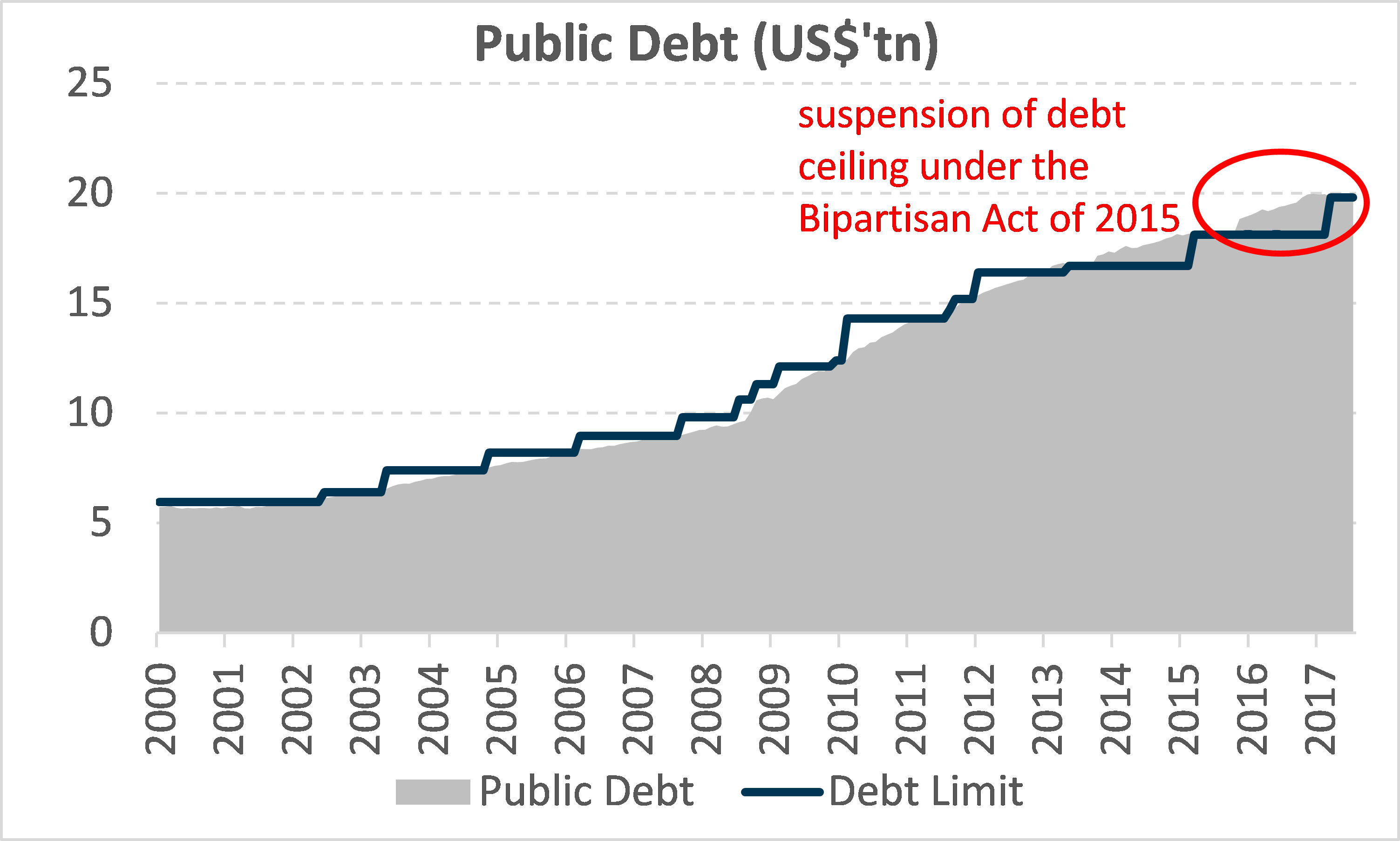

Since 15th March 2017, the Bipartisan Act of 2015 to suspend the debt ceiling was lifted, and the ceiling was adjusted to reflect the current debt level then. Without an agreement to raise the debt ceiling, the U.S. Treasury will not be able to issue more U.S. Treasuries notes or bills to fund their ongoing liabilities.

The U.S. Treasury has since, deployed extraordinary measures to prevent the U.S. government from going into default. Such extraordinary measures were expected to exhaust around September to October.

A bill was passed on the 8 of September, postponing the debt ceiling negotiating to December 2017. The bill raised the nation’s borrowing limit for the next three months, funding the government and providing US$15.3 billion in aid for victims of Hurricane Harvey. The bill sailed through Congress with an overwhelming vote as no member of Congress wanted to be blamed for delaying aid relief to the victims of Hurricane Harvey.

Figure 4: Public debt will remain in limbo without longer term plans

The congressional debt ceiling brinkmanship in 2011 had led Standard & Poor’s to downgrade the credit rating of the United States. This time around, Moody Credit Rating Agency has also hinted that the 2017 debt ceiling impasse may instigate the agency to downgrade the credit rating of U.S. together with the outlook for U.S. economy. However, they added that prioritising the liabilities of U.S. Treasury might help to mitigate the situation.

If Moody were to downgrade, they would be the second major rating agency to rate U.S. credit at AA+ following Standard & Poor’s downgrade in 2011. Although U.S. will still hold on to their investment grade rating, this will inevitably raise questions about U.S. credibility. This can be damaging for the Dollar.

Overleverage does not end well with rising interest rates

In this period of high indebtedness, U.S. Fed is trying to normalise monetary policies by raising the interest rate. Theoretically, an increasing rate environment tends to lead to a higher default rate as interest expenses grow larger as a percentage of income. Empirically, this was proven to be true when the Federal Reserve started raising interest rate in May 2004. The tightening monetary policies ultimately lead to the subprime crisis and GFC. We believe the moral hazard of “easy money” will surface again during this new period of interest rate hike cycle.

US Administration remains unsettled

We can usually infer the stability of a nation from the political party in power. And the high turnover in the Trump administration has left many doubts on the ability of the administration to lead the nation.

Since President Trump took over the white house, there has been a number of personnel that have either been fired or decided to resign from his/her post. Among this personnel, the more notable leavers were;

From the list above, it is clear that it was not the junior staffs that were leaving but rather, high-profile positions that were vacated. Such “easy-fire” policy had not been observed in prior presidential terms. The high staff turnover has shaken the confidence for the administration.

In addition to staffing problem, the Trump’s administration has disappointed on his campaign promises as well. They had lost the vote in repealing and replacing the Affordable Care Act aka “Obamacare”. Until now, there has been no substantial tax reform proposed by Trump and his administration too. More worring is the ongoing Special Counsel Investigation on the link between Trump’s 2016 presidential campaign and the Russian government. The worst case scenario will see an impeachment of Donald Trump.

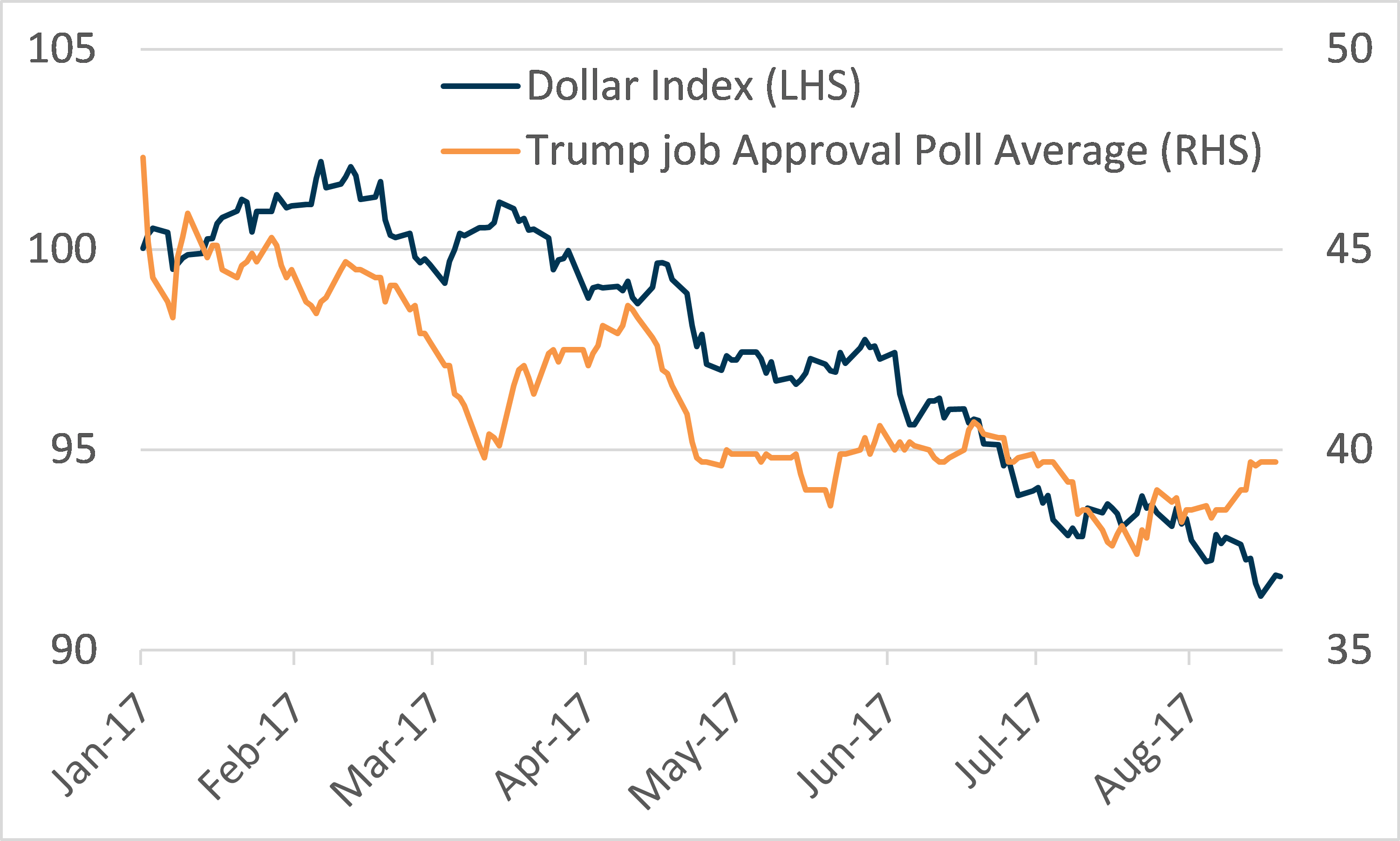

Although it is just eight months into his Presidential term, it is safe to say that Trump has not met the expectation of the public. This has anecdotally affected Trump’s approval rating with a causation of a weaker U.S. dollar.

Figure 5: Confidence in new administration is waning and it is affecting the U.S. dollar

Source: Bloomberg, PSR

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Sai Teng covers the global macro research. He has more than 6 years investment experience primarily in portfolio construction and asset allocation. He graduated with Bachelor of Science in Banking and Finance from University of London.