Description

GameStop Corp. (NYSE:GME) is a video game retailer. The Company distributes video game hardware, physical and digital video game software, video game accessories, as well as mobile, consumer electronics and other merchandise through its stores. The Company’s segments consist of retail operations, engaged in the sale of new and pre-owned video game systems, software and accessories. The stores sell various types of digital products, including downloadable content, network points cards, prepaid digital, prepaid subscription cards and digitally downloadable software and also sells mobile and consumer electronics and collectible products. Its Technology Brands segment includes its Spring Mobile and Simply Mac businesses.

Source: Thomson Reuters

Investment Rationale

GME reported positive Q3 earnings, with EPS of USD0.54, beating consensus estimates of USD0.43. Revenue was also 1.5% higher YoY, coming in at USD1.99bn, beating consensus estimates by USD30mn. GME cited stronger same-store sales growth as well as strong demand for the Nintendo Switch as reasons for the positive earnings. As stated in our previous trading note on GME, we believe that while GME is facing headwinds in its core product line, it has been unfairly punished and there are several positive catalysts for the stock on the horizon.

Recent Price Action: Since our previous Trading Note on GME, the stock had hit out target price of USD23.96 before tumbling below our stop loss of USD19.95. The stock then fell further to its 52-week low of USD15.85 and has since recovered to its last done price of USD16.73 on the back of its positive Q3 results.

Video game Hardware Sales: The current generation of hardware consoles, the PS4 and the XBox One, arrived close to 4 years ago in November 2013. This coincided with a huge run up in GME share price prior to the release of the consoles. With the release of the Nintendo Switch in March 2017, and its massive popularity, we believe that this might signal a new cycle for Video game Hardware, which GME might benefit from. GME reported that New Videogame Hardware sales came in at USD309.5mn for the quarter, up 8.8% YoY, on the back of strong demand for the Switch. As of end October, Nintendo reported that the Switch had sold more than 7.6mn units and had increased their expectations for the console, expecting it to sell 14mn units, up from initial estimates of 10mn, in its first year.

Strong Console sales also equate strong game sales, as consumers buy the games to play on their consoles. GME reported new Video game software sales came in at USD649.9mn, up 5.4% YoY. High demand for the Switch’s line up of games help drive GME software sales. Legend of Zelda: Breath of the Wild, sold more than 4.7mn copies since release, and Super Mario Odyssey, which released on 27 October, has already sold more than 2mn copies.

Additionally, Microsoft recently released its update to the Xbox One, the Xbox One X, on 7 November. Early numbers for the console has been very positive, with UK numbers coming in at 80,000 units in its first week. The PS4 Pro, Sony’s equivalent, took 4 weeks to hit that figure.

With the holiday season coming, we believe that Hardware and Software numbers should continue to boost GME’s sales.

Transitions: GME has not been sitting idly while their core market segments are being eroded. With the acquisition of ThinkGeek, GME has reported strong results for its collectible segment, with an increase YoY of 26.5% to USD138.4mn. GME also expected collectibles to grow 30% to 40% in FY17. GME mentioned that they are shifting their in-store product mix to be 50-50 games and collectibles, which should help boost collectible growth.

GME is also attempting to adapt to the trend of digital downloads for games by branching out as a game publisher, launching GameTrust last year to publish indie games. GME mentioned that digital sales increased 11.9% YoY, though on a reported basis the sales declined to 16.8%, Non-GAAP digital sales increased 1.8%, due to the sale of Kongregate, a mobile game developer.

Valuations: GME closed at USD16.73 and trades at a PER of 5.03, with a dividend yield of 9.09%. GME has total debt of USD816mn, with USD262mn in Cash and equivalents. GME’s annual net income has also been relatively consistent despite headwinds, at USD353mn in FY16 and USD402mn in FY15. GME also pays a very high dividend, yielding 9.09%. This amounts to an annual payout of about USD155mn. GME is expected to generate more than USD400mn in Free Cash Flow, and even its worst year in the past 5 years, GME managed to generate USD300mn in Free Cash Flow. GME’s high yield dividend is very well covered and should not be in any danger of cuts despite the fears over its business. As such, we believe that GME is very much undervalued at this price despite the headwinds they are facing.

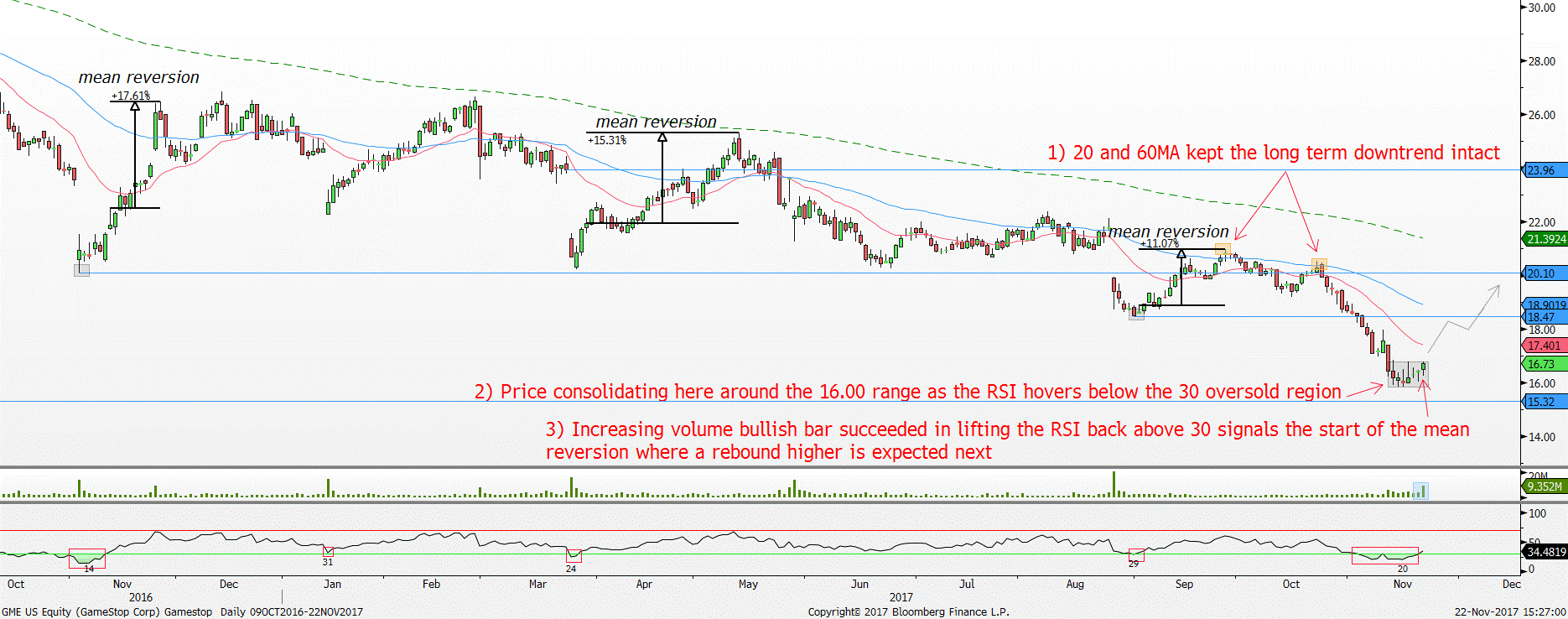

Technicals: GME continued to move in a long-term downtrend with sharp rebounds occurring along the way when the Relative Strength Index (RSI) signals oversold condition. RSI measures momentum and a reading below 30 suggests oversold condition. This oversold RSI mean reversion pattern has been working perfectly since January 2016 where GME experienced five of such price action pattern. On average, the rebound off the respective lows was around 17%.

GME Daily chart – Mean reversion higher next due to the oversold RSI

Support 1: 16.00 Resistance 1: 18.47

Support 2: 15.32 Resistance 2: 20.00

Red line = 20 period moving average, blue line = 60 period moving average, Green line = 200 period moving average

Since the last update on 7 April 2017, GME continued to move in a general downtrend. It gapped down significantly on 25 August 2017 and subsequently took the RSI into oversold condition. The RSI hit a low of 29 on 31 August 2017, and once the RSI closed back above 30 the following day, the mean reversion pattern took over, and GME rebounded sharply up 11%.

Even after the recent mean reversion since August, the rebound in price appeared short-lived. The 20 and 60-day moving average once again capped the bullish recovery in GME where the long-term downtrend retook control. The downtrend managed to bring price down to break a new 52 week-low, and as a result, the RSI entered into the critical oversold region since 3 November 17.

With the mean reversion pattern still fresh in mind, the recent price action suggests a possible bottoming process. GME began consolidating around the 16.00 range as the RSI dipped below the 30 oversold region. On 21 November 17, a more decisive bullish price action appeared. There was an increasing volume bullish bar that succeeded in lifting the RSI back above the 30 oversold region. That price action validates the mean reversion pattern is happening where a rebound higher to the 18.47 resistance area followed by 20.00 is expected.

Bear in mind a stronger support area lurks in the background suggests limited downside. The 2012 low of 15.32 should keep a floor on the share price in the short run.

Conclusion: We are bullish on GME due to 1) New Hardware sales, 2) Transition plan and 3) Strong financials and dividend yield. As such, we believe that stock is undervalued and with recent signs of recovery, we are bullish.

![]()

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: