What is the news?

Cache Logistics Trust (Cache) has launch an underwritten and renounceable 18-for-100 Rights Issue to raise S$102.7mn. 162,565,716 new units will be created in the Rights Issue. Pro forma distribution per unit (DPU) is 10.9% lower, due to the enlarged unit base.

How do we view this?

The bulk of the proceeds will be used to pare down debt. Aggregate leverage is expected to reduce to 35.5% from 43.4% (as at 2Q 2017). We estimate debt headroom of S$238mn after the Rights Issue (assuming 45% target aggregate leverage), compared to existing portfolio value of S$1.24 bn (as at 2Q 2017).

Cache does not have any debt maturing in 2017. For 2018, there is A$30.0mn and S$192.0mn of debt maturing. We infer that the bulk of it should be in 2H 2018, as there is only S$6.73mn of current debt reflected in the latest 2Q FY17 balance sheet. Hence, there is no major debt maturing within the next 12 months. There was also no acquisition announced in conjunction with the Rights Issue.

In our recent Industrial REITs Sector Report (18 August 2017), we highlighted the negative impact of year-end property valuations on aggregate leverage. We think the Rights Issue could be a pre-emptive move by Cache: either before its aggregate leverage exceeds the statutory limit of 45%, or that the manger is already considering a pipeline of properties for acquisition.

Maintain Neutral; lower target price of $0.82 (previously $0.86)

Changes to our FY17e/FY18e forecast are 6.8%/18.6% lower interest expense, 2.0%/5.3% higher distributable income and larger unit base from the Rights Issue. The net effect is 5.7%/10.5% lower FY17e/FY18e DPU forecast from previous. Our target price represents an implied FY17e forward P/NAV multiple of 1.09x, which compares against the FTSE REIT Index forward 12-months P/NAV multiple of 1.05x.

We also raised our terminal growth assumption to 0.0% from -0.5% due to the execution of the Rights Issue. The lower aggregate leverage results in an improved debt headroom to support inorganic growth.

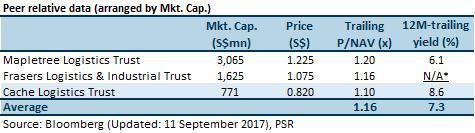

Relative valuation

Cache is under-valued relative to logistics peers in terms of trailing P/NAV multiple.

* Frasers Logistics & Industrial Trust does not have a 12 month track-record.

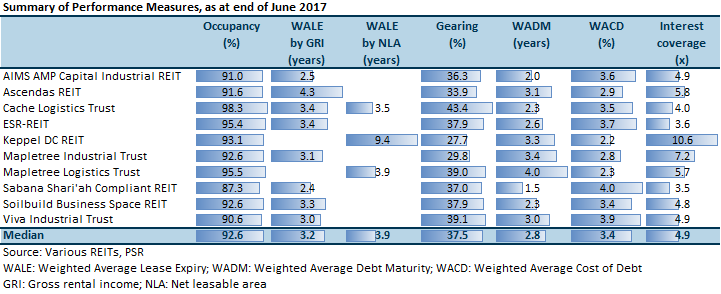

Performance Measures of Industrial S-REITs

Cache has the highest aggregate leverage among the Industrial REITs (as at 30 June 2017) and was the only one with an aggregate leverage greater than 40%.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.