The Positives

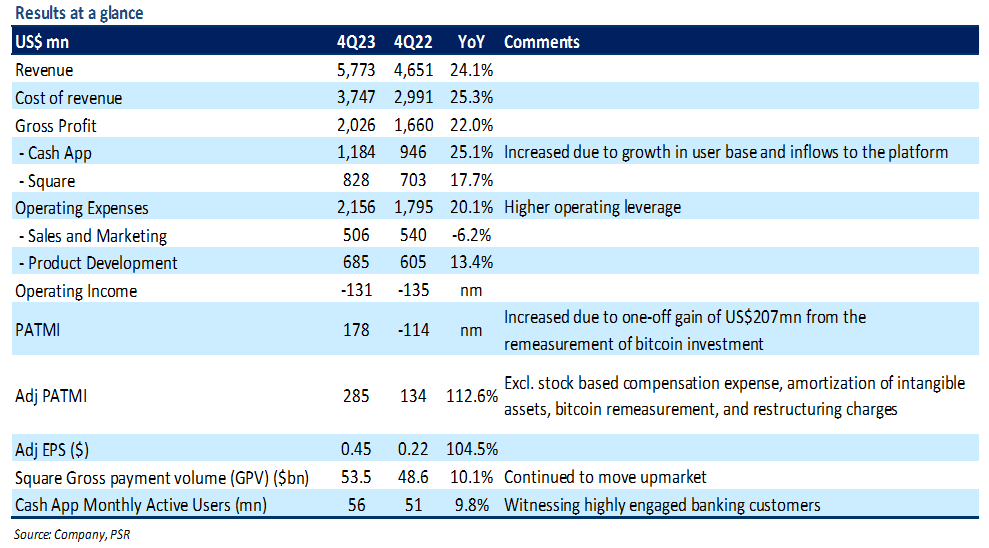

+ Strength in Cash App revenue. Block’s Cash App segment, which offers digital banking and investing services to consumers, reported revenue growth of 31% YoY to US$3.9bn (ex-bitcoin was up 20% YoY to US$1.4bn) and gross profit growth of 25% YoY to US$1.2bn. The growth was mainly driven by a 10% YoY surge in its monthly transacting active users (MAUs) to 56mn led by continued product enhancements and addition of new features like free overdraft coverage and a 4.5% annual interest on savings balances. Block reported a 20% YoY jump in Cash App debit card active users to 23mn. In addition, inflows per active user grew by 8% YoY to US$1,137, leading to increased adoption of its Cash App products and services, including debit cards, ATM withdrawals, investing in stocks/bitcoin, and Cash App Pay.

+ Higher operating leverage. Block expanded its adj. net profit margin by 200bps YoY to 5%, with adj. PATMI also more than doubled to US$285mn. This was mainly because the company continued to show improvements in cost efficiencies as OPEX growth slowed to 20% YoY (4Q22: 45% YoY) – Sales & Marketing expenses were down 6% YoY. Management highlighted that the company met the goal of reducing the number of employees to under 12,000 compared with 13,000 employees as of 3Q23.

The Negative

– Square’s GPV growth further decelerates. Square segment, which enables merchants to accept payments, processed US$53.5bn of gross payment volume (GPV) in 4Q23, an increase of 10% YoY compared to 14% YoY growth in 4Q22. Management highlighted that the severe weather conditions in the US in January had a 3% to 4% moderation in GPV growth, specifically lower in-person discretionary spending within food and beverages and retail categories. Notably, Visa also reported a slowdown in US payments volume growth in January due to cold weather.