The Positives

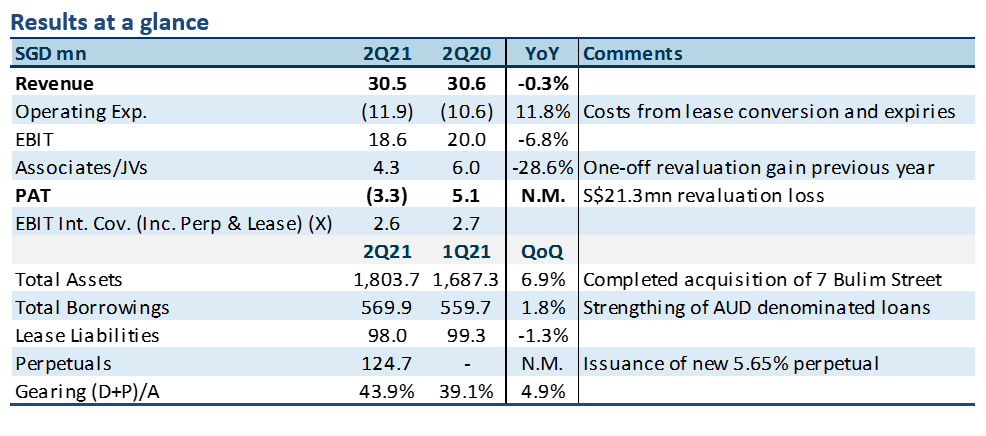

+ Completed acquisition of 7 Bulim Street. This was the main contributor to asset base increase of 7%. The acquisition is yield accretive at a yield of 7.07% compared to the 5.65% coupon perpetual bond issued to fund it. Aggregate leverage improved to 33.6% from 35.4% in the previous quarter due to the S$125mn perpetual bond issuance.

+ Significant debt headroom. AAREIT has a debt headroom of S$234mn or 35%, and a property loss threhold of S$467mn or 28% before the MAS 50% gearing limit is breached. This represents significant buffers. We note that the property with the largest percent loss in the latest revaluation exercise as at 30 September 2020 was 103 Defu Lane 10 at 7%.

+ Healthy liquidity. Cash/ST borrowings stood at 2.2x with no debt maturing until November 2021. Adjusted interest coverage ratio, which included amounts reserved for distribution to perpetual holders stood at 3.6x, compared to the 2.5x minimum by MAS set to effect on 1 January 2022.

+ Leasing resilient amid logistics and warehouse demand. AAREIT secured 5.7% of total NLA of leases in the quarter, with 11.8% of leases by GRI remaining to expire in FY21 (YE 31 Mar 2021). Occupancy notched up to 94.5% from 93.6% QoQ. Weighted average rental reversion for renewed leases was stable at -0.8% in 2Q21 compared to previous quarter of -9.0%.

The Negatives

– Nil.

Outlook

The outlook is resilient for industrial REITs. AAREIT’s low gearing gives it ample buffers against asset losses, and its top tenant Optus Administration, a subsidiary of SingTel Group, contributing 13% of 2Q21 GRI provides higher cash flow certainty.

Valuation

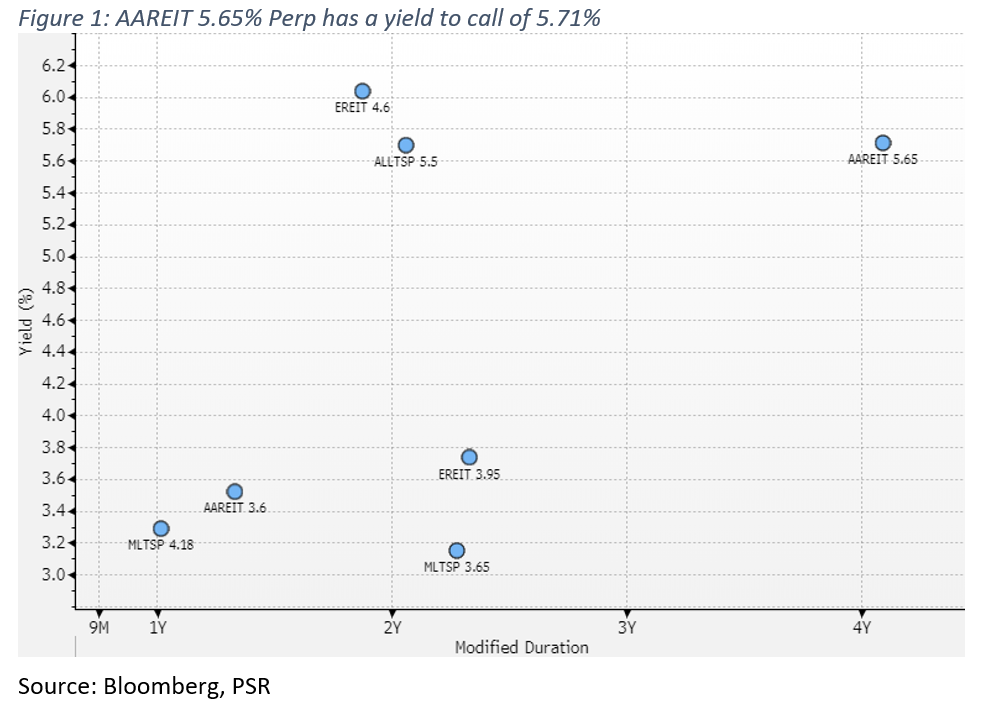

We are Overweight on the AAREIT 5.65% Perp NC5 (SGD). The bond trades at an attractive yield of 5.7% compared to AAREIT’s dividend yield of 6.6% based on 26 October 2020 closing share price. We think the bond to dividend yield spread difference of 0.9% is narrow. As a comparison, the ESR-REIT EREIT 4.6% Perp NC5 (SGD) bond with a yield to call of 6.0% trades at a 1.3% yield difference to the dividend yield of 7.3%, while the Mapletree Logistics Trust MLTSP 3.65% with a yield to call of 2.8% trades at a 1.1% yield difference to the dividend yield of 3.9%.

The bond’s first call date falls on 14 August 2025 and the coupon resets based on the 5-year SGD Swap-Offer Rate (SOR) plus 5.207%. The current 5-year SOR is 0.4825%.

No pricing indicators for the AAREIT 3.6% 22Mar22 Corp (SGD) and AAREIT 3.6% 12Nov24 Corp (SGD) bonds.

About AIMS APAC REIT

AIMS APAC REIT (“AA REIT” or the “Trust”) is a real estate investment trust which was listed on the Main Board of the SGXST on 19 April 2007. AA REIT is externally managed by AIMS APAC REIT Management Limited (the “Manager”). The principal investment objective of the Manager is to invest in a diversified portfolio of income-producing real estate assets located in Singapore and throughout the Asia-Pacific region that is used for industrial purposes, including, but not limited to warehousing and distribution activities, business park activities and manufacturing activities. The Manager’s key objectives are to deliver stable distributions to Unitholders and to provide long-term capital growth. The Group has a portfolio of 28 industrial properties, 26 of which are located throughout Singapore, one industrial property located in Gold Coast, Queensland, Australia and one business park property located in Macquarie Park, New South Wales (“NSW”), Australia.