The Positives

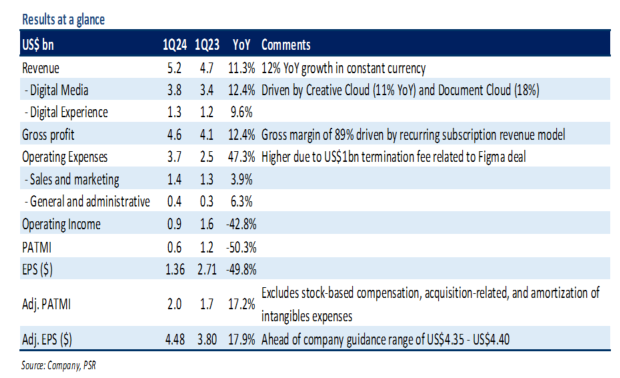

+ Revenue beat top-end of guidance. In 1Q24, Adobe’s total revenue rose 11% YoY to US$5.2b, which came 1% ahead of the top end of company guidance. Revenue from the Digital Media segment grew 12% YoY to US$3.8bn, with Creative Cloud revenue growing to US$3.1bn (up 11% YoY) and Document Cloud growing to US$0.8bn (up 18% YoY). This growth was mainly fueled by continued demand for its photography and video editing applications (Photoshop and Illustrator) and Acrobat PDF and e-signature solutions. Management highlighted that Acrobat Web’s monthly active users, or MAUs, spiked 70% YoY and surpassed 100mn users in the quarter.

+ Margins continue to improve. Gross and adj. net profit margins expanded by 80bps and 200bps YoY, respectively. The margin improvement was mainly due to top-line upside and higher operating leverage, including careful sales and marketing spend. Adj. PATMI increased by 17% YoY to US$2bn.

The Negative

– Soft 2Q24e revenue guidance. For 2Q24e, Adobe expects total revenue to grow 9% YoY to US$5.3bn. Management highlighted that the slowdown is mainly because of tough comparisons as price increases over the last two years has started to roll-off. Meanwhile, the new pricing for Creative Cloud apps with Firefly AI tools would become a tailwind towards the end of FY24e as it hits larger customer base at renewals. In addition, Adobe faces increasing competition from startups such as Midjourney and OpenAI’s Dall-E, which offer gen-AI services similar to Adobe’s Firefly like generating images from text prompts.