|

Report type: Weekly Strategy |

“The Commodity Storm, LNG Plants and the COVID-19 Regulations Easing Market”

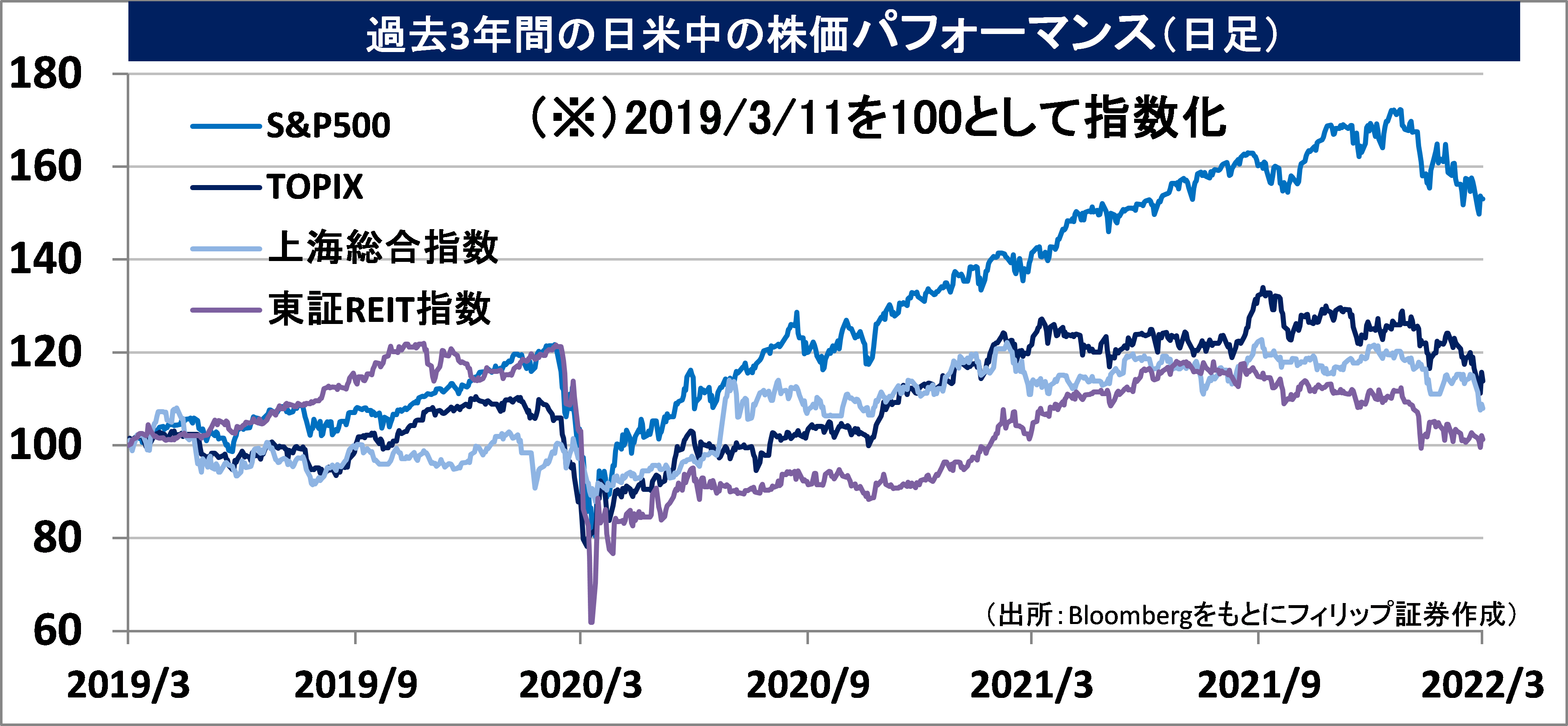

After Russia’s invasion of Ukraine, it invoked a sharp rise across the entire commodity futures market, such as energy, resources and grains. Also due to an evening-up of big shorts, the LME nickel futures, which was at a level of 20,000 dollars per tonne on 4/3, rose sharply to 100,000 dollars per tonne on the 8th, forcing it to an extraordinary situation where the exchange considered cancelling trades and suspending trading. Although the market rises sharply in the short-term due to a forced evening-up of shorts in order to avoid a remargin in the futures market, once it settles, it would be difficult to maintain a high price after a sharp rise. In terms of judging whether the price of futures or underlying assets of futures (spot) are being overbought in the short term, there is a need to look at the price difference (spread) between the expiration months of the futures. In particular, in commodities, if the prices of near futures are higher than distant futures, there will likely be a need to be wary of short-term market overheating. Also, regarding stocks related to energy, resources and materials, there may also be a need to note that daily stock prices tend to get caught up in violent fluctuations in the commodity futures market.

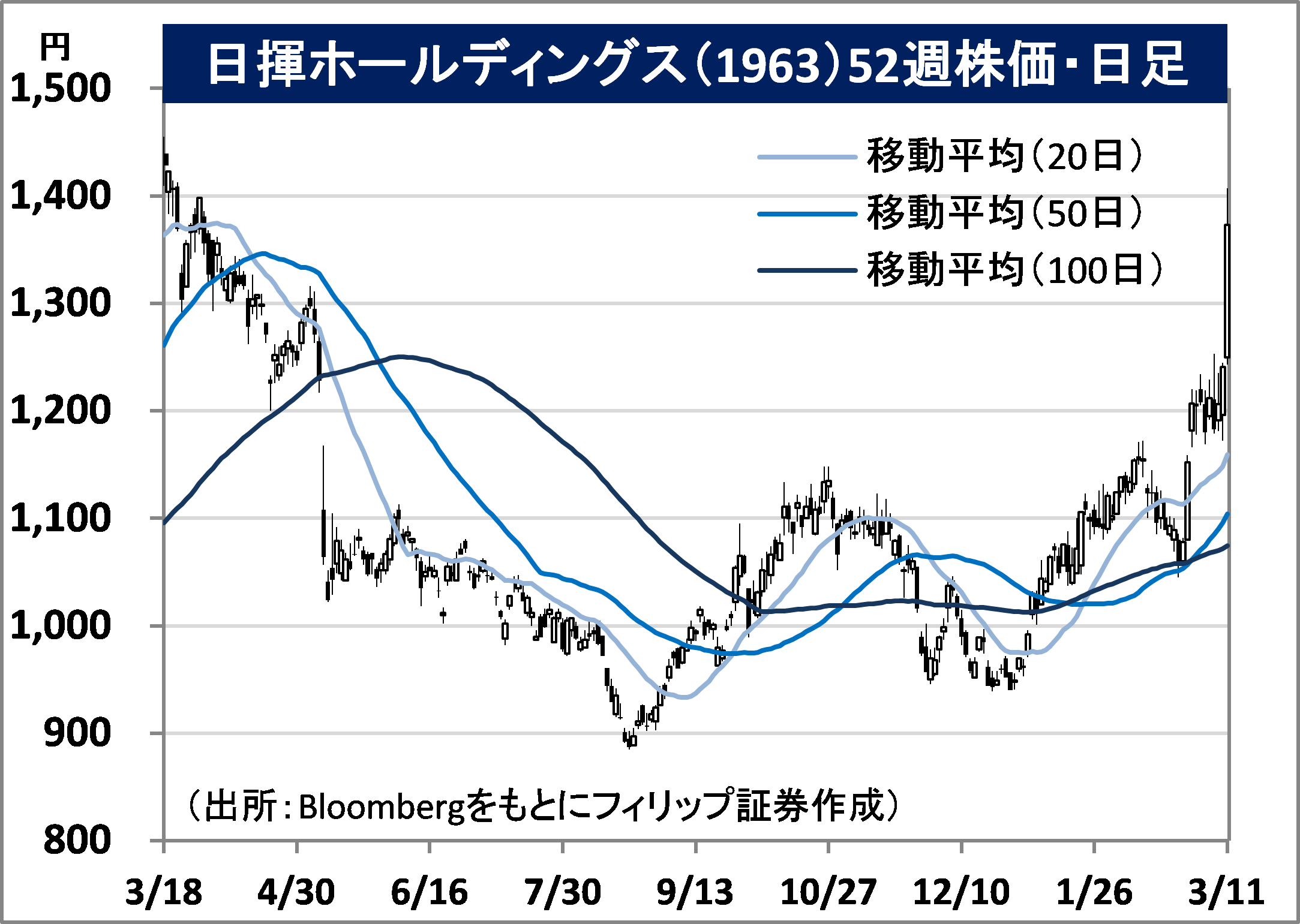

At the extraordinary energy ministers’ meeting (online) held on the 10th in response to Russia’s invasion of Ukraine, reducing the reliance on Russia for natural gas in Europe was pointed out as “a particularly urgent issue” and investment in the LNG (liquefied natural gas) field is needed. In the plant engineering industry involving LNG plants, the 3 giants in Japan are said to be JGC Holdings (1963), Chiyoda Corporation (6366) and Toyo Engineering (6330). JGC, the industry’s largest, has achievements across a wide range of fields, such as petroleum / natural gases and renewable energy. Chiyoda Corporation is recognised for technological development involving the large volume shipping and storage of hydrogen in addition to having the highest sales distribution ratio of LNG plants out of the 3 giants at above 50%. Compared to the other two companies, rather than LNG plants, Toyo Engineering has strengths in plants related to chemical fertilisers, such as urea and ammonia, etc. It just so happens that there are also concerns of a supply shortage of ammonia due to reinforced economic sanctions on Russia by various countries in the world.

With various countries in the world removing COVID-19 regulations and starting to allow foreigners to enter the country without quarantine as long as vaccination is complete, the Japanese government’s policy is to also present a new way of thinking on the 11th concerning the “semi-emergency coronavirus measures” which could be lifted if a decrease in hospital bed usage is expected in spite of new infections remaining at a high level. Also, regarding national border measures, in addition to increasing the limit of persons entering Japan daily from the current 5,000 to 7,000 from the 14th onwards and accepting 1,000 per day in a separate category for students studying abroad, it was reported that they are considering accepting all foreign students wishing to enter Japan by end May. Perhaps the other side of chaos of the Ukraine situation may lead to a “COVID-19 regulations easing market”. There will likely be a need for “compound-eye investment”, which keeps one eye on immediate concerns and another on anticipating the next course.

In the 11/3 issue, we will be covering JGC Holdings (1963), Shionogi & Co. (4507), TOTO (5332) and Kyoritsu Maintenance (9616).

・Established in 1928 as Japan Gasoline Co., Ltd. Expands a functional materials manufacturing business which carries out the manufacture and retail of catalysts and fine products, etc. in addition to a comprehensive engineering business which manages various plants, facility design, procurement and construction, etc.

・For 9M (Apr-Dec) results of FY2022/3 announced on 10/2, net sales increased by 4.8% to 319.442 billion yen compared to the same period the previous year and operating income decreased by 11.5% to 15.332 billion yen. Despite a deficit in net income from the recording of an extraordinary loss involving the Ichthys LNG Project, there has been progress in investment, such as in renewable energy power generation in Asian regions and a resumption of facility investment plans in various oil and gas-producing countries.

・For its full year plan, net sales is expected to increase by 8.3% to 470 billion yen compared to the previous year and operating income to decrease by 12.6% to 20 billion yen. In response to Russia’s invasion of Ukraine, on 10/3, an extraordinary energy ministers’ meeting was held online among 7 major countries (G7). A joint statement was consolidated which included the necessity to invest and increase the supply of LNG (liquefied natural gas) and addressed the “particularly urgent issue” of reducing reliance on Russia for natural gas in Europe. This will likely benefit the company.

・Founded in 1878 by the founder Gisaburo Shiono. Carries out the research and development, manufacture and retail, etc. of pharmaceuticals. In addition to having strengths in the areas of infections, aches and central nerves, they are proactively developing cancer treatments and vaccines. Their anti-HIV (AIDS) drug became mass produced.

・For 9M (Apr-Dec) results of FY2022/3 announced on 31/1, sales revenue decreased by 2.1% to 219.6 billion yen compared to the same period the previous year and operating income decreased by 42.5% to 60.4 billion yen. The decrease in royalty revenue for the dyslipidaemia drug “Crestor” and the entry of the antidepressant “Cymbalta” in generic drugs have affected, leading to a decrease in revenue. The increase in research and development costs for the COVID-19 vaccine and treatment have also influenced the decrease in profit.

・For its full year plan, sales revenue is expected to decrease by 1.1% to 294 billion yen compared to the previous year and operating income to decrease by 23.4% to 90 billion yen. On 25/2, the company applied for the manufacturing approval for the orally-administered COVID-19 drug with the Ministry of Health, Labour and Welfare and sought application for the “conditional early authorisation system”. They have advantages in terms of having lesser medicines prohibited to be used in combination compared to the U.S. Pfizer’s “Paxlovid”, which has already been approved as a special instance in Japan. On 28/2, Prime Minister Kishida also answered in the response to the Diet deliberations regarding the supply of required amount.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: