The Positives

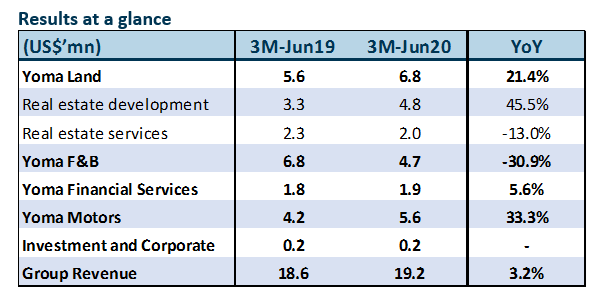

+ Yoma Land’s revenue is well supported by backlog of unrecognized revenue. Although sales were minimal this quarter (8 units of CityLoft and 1 unit of Peninsula Residence) amidst cautiousness in big-ticket expenditure and delays in paperwork, Real Estate Development registered a 45.5% YoY revenue increase. It is largely attributable to the revenue recognized from the completion of City Loft. Unrecognised revenue now amounted to US$17mn as at 3Q20 vis-à-vis more than US$20mn in 2Q20. Real Estate Services revenue was lower YoY due to lower occupancy levels and rental rates at Pun Hlaing Estate and StarCity. However, the lower rental rates and the amenities and services offered amidst COVID-19 had driven a partial recovery in occupancy levels in recent months.

+ Yoma Motors registered revenue growth of 33.3% largely attributable to the Heavy Equipment segment; Passenger and Commercial Vehicles (PCV) segment held up. Despite the COVID-19 impact from border closures and falling crop prices, more tractors and implements were sold due to pent up demand after many quarters of weaknesses arising from the exceptionally heavy monsoon last year. New Holland sold 124 tractors in the quarter compared to 61 tractors in 3M-Jun2019. Higher PCV revenue was driven by the sale of 16 Volkswagen vehicles and 22 Ducati motorbikes. Mitsubishi and Hino also saw significant improvements with 184 Mitsubishi vehicles (65 vehicles in 3M-Jun19) and 26 Hino trucks (9 trucks in 3M-Jun19) being sold. Mitsubishi sales were boosted by the popular Xpander model and there remains c.US$7.5mn backlog of unfilled orders.

+ Revenue from Yoma Financial Services increased by 5.6% YoY underpinned by an enlarged finance lease portfolio in Yoma Fleet; Wave Money remains EBITDA positive despite weaker transaction numbers. Vehicle numbers for Yoma Fleet grew by 11.1% year-on-year to 1,290 vehicles and third-party assets under management stood at US$45.6 million as of 30 June 2020. As finance leases carry higher gross profit margins, we are expecting a larger flow-through from Yoma Fleet to the bottom line in 2H20.

Due to the Thingyan holidays amidst the Myanmar New Year in April and COVID-19 measures, Wave Money’s OTC business was largely affected, which resulted in a decline in revenue and transaction numbers of 16.5% and 25.3% respectively from the previous quarter. However, its e-wallet business continued to record double digit growth rate month-on-month as more people opt for cashless transactions and is on track to reach its 1.3 million MAUs target by December 2020. EBITDA for Wave Money remained positive due to economies of scale and cost control.

The Negatives

– Yoma F&B revenue was down 31% YoY due to COVID-19 measures. 3Q20 revenue declined 31% YoY due to government-imposed lock downs, curfews and prohibitions on dine-in between April to mid-May and temporary store closures in severely affected trade zones. The month of April was most affected as revenue fell 50% YoY. During the initial stages of COVID-19 there was a large shift towards delivery, which mitigated some of the shortfall in dine-in revenue. Delivery accounted for 40% of the total sales in April at the peak, which normalised to 15%-20% as restrictions eased and some of these customers return to restaurants. June recorded a smaller decline of c.25% YoY since the Myanmar government allowed restaurants to resume operations conditional upon adherence to certain guidelines at the end of May.

Outlook

Pre-COVID, CityLoft has been recording a healthy booking rate at >50 units per month. Amidst COVID-19, interest in the property remained high as the team continued to engage customers through virtual show flats. However, CityLoft’s booking rate slowed significantly from April to May. As the economy started to reopen at the end of May, buying interest noted a recovery. Booking rate was nearing half of pre-COVID levels by July.

According to World Bank’s June report, the agriculture sector had been resilient and is expected to grow by 0.7% for the year. This is mostly due to an increase in production of crops, such as rice, and beans and pulses. Meanwhile, the Myanmar government and NGOs are also supporting the agricultural industry by providing lower-interest loans for buying inputs and giving greater flexibility on loan repayments. These initiatives will spur demand for tractors which is beneficial for Yoma Motors.

During this period, Wave Money will continue to work with various organisations such as Myanmar Agricultural development to disburse loans for farmers and Social Security Board to disburse medical and COVID-19 quarantine relief through the adoption of Wave Pay. We are expecting the growth of the e-wallet business to be fast-tracked by these schemes to make up for fewer transactions in the OTC business.

Yoma F&B witnessed improved performance MoM as business starts to recover in the coming quarter. Sales for July was nearing-pre-COVID level with same store sales growth recorded in certain days. The accelerated adoption of delivery services positioned Yoma F&B better to capture sales thwarted due to dine-in prohibitions. Yoma’s target of opening 2-3 KFCs by the end of 2020 remains unchanged.

Maintain BUY with an unchanged TP of S$0.460. Our target price translates to a total upside of 58.6%. Property and financial services will constitute 68% and 19% of the valuation respectively. A conglomerate discount of 20% has been applied (Fig.1).

The report is produced by Phillip Securities Research under the ‘Research Talent Development Grant Scheme’ (administered by SGX).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: