The Positives

+ Better margins can be expected. In FY16, US$4mn of sales came from the lower margin wholesale channel. We estimate this amount to be significantly less in FY17 as the group moves more aggressively to online marketplaces. This transition will lead to higher margins in future.

+ Contribution from additional book publishers not yet factored in. Sales from additional publishers have not materially started. We expect to see contribution from the various publishers in FY18.

The Negatives

– Increase in commission & fulfilment in online marketplaces. This affected the whole industry. Marketplaces have raised their fees in exchange for greater direct access to the consumer. Such cost will be mitigated by the rise in overall sales and improving scale for the company.

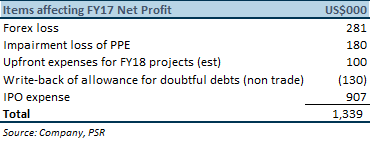

– Headline results in FY17 affected by several one-off items. FY17 net profit was affected by several one-off expenses, notably the following:

Outlook

We remain upbeat on the outlook of Y Ventures. We expect strong sales growth stemming from its current publisher, maiden contribution from new book principals, launch of the recently secured 20 consumer brand names and momentum in its own branded products.

Downgraded from BUY to NEUTRAL with unchanged target price of S$0.70

We downgraded our recommendation to NEUTRAL due to the share price performance, up 54% since our recent initiation. There has been no change in our fundamental view of the company. Y Ventures is riding on the boom in e-commerce through new product categories, expanding customer base and new project initiatives.