|

Report type: Weekly Strategy |

“Turning Into Ukraine’s ‘Distant War’ and a Possible Recovery in Japan Inbound?”

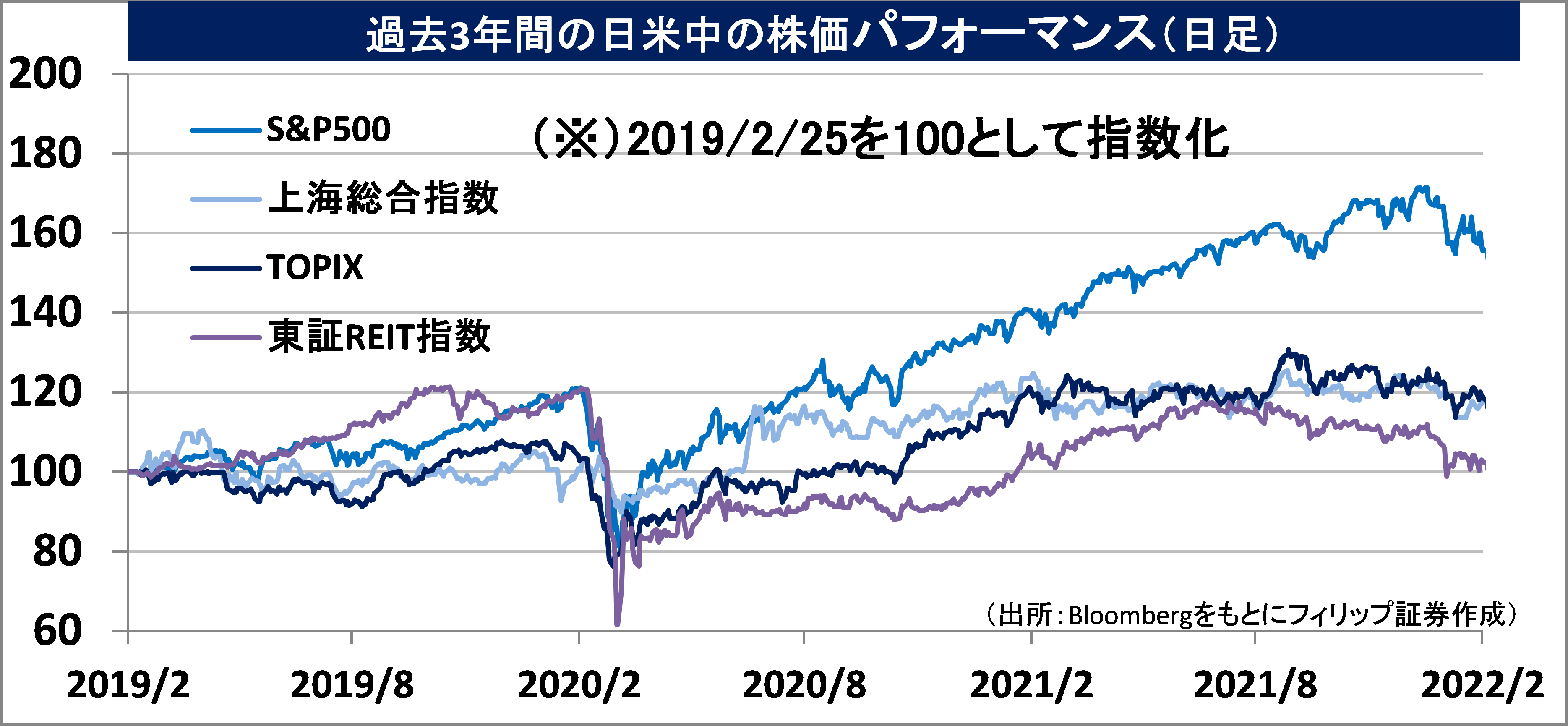

The Russian invasion of Ukraine raged throughout the stock market as well. On 21/2, Russia approved the independence of Donetsk People’s Republic and Luhansk People’s Republic in the Donbas region of eastern Ukraine and dispatched special troops called the “peacekeeping forces” on the 24th for the purpose of safeguarding residents. An actual invasion began which led to a military operation. On the afternoon of the 24th, it was also reported that attacks by the Russian army were made on the capital Kyiv and the Nikkei average ended up falling to 25,775 points. At that point, perhaps the stock market had attempted to incorporate the possibility of an increase in concerns of risks spiralling, such as by expecting the scenario of U.S. President Biden removing the Russia from the international payment network SWIFT (The Society for Worldwide Interbank Financial Telecommunication) as a form of economic sanction on Russia and the subsequent financial system pandemic from a credit default for Russia, etc. After the end of trading hours in the Japanese stock market, the WTI Crude Oil Futures price rose sharply to exceed 100 dollars a barrel last since 2014 and the CMX Gold Futures price also soared to 1,976 dollars an ounce.

In response to this, the trend reversed as a result of economic sanctions announced by U.S. President Biden not including the removal of Russia from SWIFT, which were limited to sanction measures on 4 new banks that include Russia’s No.2 bank, VTB bank, and export regulations on high-tech products as well as speculations on whether the situation will cool off in the short-term due to the Russian army’s oppression of Kyiv, etc. Around 5am Japan time on the 25th, there were violent price fluctuations, such as the price of the WTI Crude Oil Futures falling to the 92 dollar-level and CMX Gold Futures falling to around 1,900 dollars. For the time being, the stock market perceives the Ukraine situation to be an issue that is focused on the Euro area, and perhaps there is now a greater possibility of Japan and

Asia, which do not have stakes as countries involved, finding opportunities for a buyback from a selling lead in the U.S. from next week onwards as a “distant war”.

On the 21st, the U.K. announced a complete end to COVID-19-related regulations in England. The rule for the mandatory isolation of those infected have also been removed from the 24th. Prime Minister Johnson declared that based on having achieved sufficient immunity levels in its residents, it has become possible for a full transition from infection countermeasures centring on government intervention to a policy focusing on vaccination and treatment. In response to the strong performance in accommodation demand in the year-end holiday season in Europe and the U.S., the FY2021 Oct-Dec net sales for 3 U.S. hotel chain giants: Marriot International, Hyatt Hotels and Hilton Worldwide Holdings, have increased across the board by more than twice the same period the previous year. If the number of infections decrease in Japan as well, there is a possibility of the emergence of anticipated movements, such as of the recovery in inbound demand from overseas with a focus on tourism and leisure-related stocks, etc. According to a joint survey between the Development Bank of Japan and the Japan Travel Bureau Foundation, Japan is the No.1 country people from Europe, U.S. and Australia want to visit after COVID ends.

In the 28/2 issue, we will be covering Nissui Pharmaceutical (4550), Towa Pharmaceutical (4553), Round One (4680) and Idemitsu Kosan (5019).

・Established in 1935 as a subsidiary of Nippon Suisan Kaisha (1332). Mainly manages 2 businesses, which are the diagnostic pharmaceutical business that carries out the manufacture, procurement and retail of diagnostic drugs and reagents, test equipment and materials, and the pharmaceutical business, which handles health foodstuff and pharmaceuticals.

・For 9M (Apr-Dec) results of FY2022/3 announced on 27/1, net sales increased by 39.0% to 11.609 billion yen compared to the same period the previous year and operating income increased by 2.2 times to 1.209 billion yen. In addition to Shimadzu (7701) and Tosoh (4042)’s COVID DNA reagent and Shimadzu’s DNA reagent used for testing the Omicron variant, those related to cell culture in the regenerative medicine field have been strong.

・For its full year plan, net sales is expected to increase by 19.9% to 14.35 billion yen compared to the previous year and operating income to increase by 57.8% to 1.27 billion yen. Growth is expected in functional displayed food which blends DHA (docosahexaenoic acid) and EPA (eicosapentaenoic acid) nutrients that are effective in reducing triglycerides and are commonly found in the fat of bluebacks. Also, since there is a high percentage of trading with the parent company, a capital review is expected from the perspective of the issue of parent-subsidiary listing in corporate governance.

・Founded in 1951 in Osaka City. Carries out the manufacture and retail of generic drugs. Is one of the 3 powerhouses in Japan in generic drugs. J-dolph Pharmaceutical, Daichi Kasei, which manufactures stock solutions, and the soft capsule Greencaps Pharmaceutical, etc. are subsidiary corporations.

・For 9M (Apr-Dec) results of FY2022/3 announced on 14/2, net sales increased by 9.0% to 125.613 billion yen compared to the same period the previous year and operating income increased by 14.9% to 16.993 billion yen. In addition to orders exceeding production quantities due to a stop in supply following the unauthorised production of drugs by the largest generic drug giant, Nichi-iko Pharmaceutical (4541), etc., the anticonvulsant (E Keppra) which launched in December has contributed.

・For its full year plan, net sales is expected to increase by 7.6% to 166.7 billion yen compared to the previous year and operating income to decrease by 3.1% to 19.3 billion yen. Company dividend forecast was raised to increase by 16 yen to 60 yen (original plan 51 yen). With the persistent uncertainty in generic drug supply, their policy is to construct a 3rd solid preparation block in their Yamagata factory. In addition to room for expansion in the overseas market at 22% in overseas sales distribution in 9M, a synergistic effect is expected from the acquisition of a health-related company.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: