Report type: Weekly Strategy

”Beware of Nikkei Average weighted average PBR, high PBR for IP asset valuation”

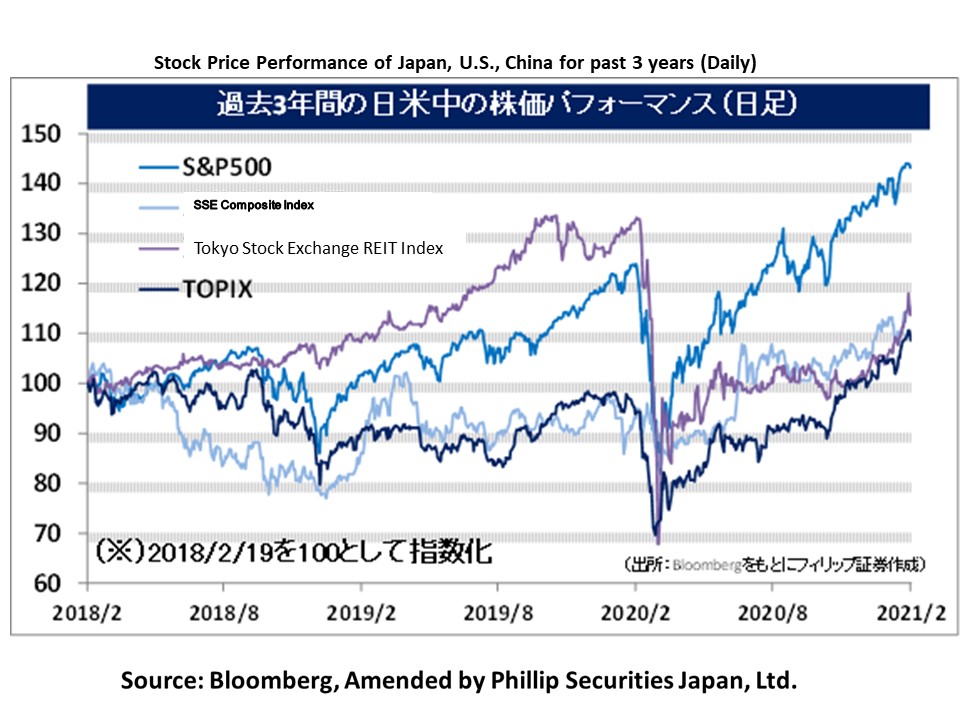

The Nikkei Average broke through 30,000 points on 15/2 and closed at 30,467 points on 16/2. This level is equivalent to 1.32 times the weighted average PBR (price-to-book-value ratio), which is weighted by market capitalization of the Nikkei Average’s constituent stocks, and is the highest level since 2nd February, 2018. At that time, the “Trump tax cuts” were enacted in the US in December 2017, and in Japan, the ruling party won with huge margins in the House of Representatives election in October 2017, resulting in strong stock markets in both Japan and the US. Optimism dominated the market as the VIX index, which is said to be a “fear index” representing investor sentiment in the S&P500 Index, fell below 10%, and the Nikkei Average soared from a low of 19,239 points on 8/9 of the same year before the dissolution of the House of Representatives to a high of 24,129 points on 23/1, 2018. Closing price on 2/2 was 23,122 points.

Under such an environment in the Japanese and US stock markets, the yield on 10-year US government bonds rose from around 2.05% in September 2017 to around 2.85% in early February 2018, and the VIX index soared from 6/2 onwards. It can be recalled that the “risk parity” strategy of lowering the ratio of risky assets being held in response to increased volatility caused the global stock markets to plunge simultaneously, and the Nikkei Average fell to a low of 20,347 points on 26/3, 2018. Since then, the weighted average PBR has exceeded 1.3 times for the first time in about three years, and, as was the case then, a rise in US long-term interest rates is expected. Therefore, in some respects, the conditions for a downward adjustment are in place.

Turning to the PBRs of individual stocks, the share price of Fast Retailing (9983) has exceeded 100,000 yen and its PBR has reached about 11 times. High PBR stocks should be viewed in terms of PBR adjusted for the addition of intangible assets to net asset, such as IP (Intellectual Property), which have economic value that does not appear on the balance sheet. Comparing the company’s share price with the market capitalization of Spain’s Inditex, the world’s largest apparel maker in terms of sales (equivalent to 10.3 trillion yen as of the closing price on 18/2), there is room to see growth potential in the value of UNIQLO and subsidiary brands. On the other hand, since it is the largest contributor amongst the constituent stocks of the Nikkei Average, it should be noted that it is likely to be overbought in index-related trading as the number of shares in circulation decreases.

In terms of IP assets of Japanese companies, there is growing interest from overseas in the value of famous titles and characters in the entertainment industry, such as video games. In terms of PBR at the close of 18/2, Toei Animation (4816), which produces “Dragon Ball” and other titles, reached about 6.2 times, while Nintendo (7974) was about 4.8 times. These are higher than that of The Walt Disney Company (DIS) of the US which is about 3.9 times. Netflix (NFLX) of the US has announced a program to support the training of animators in Japan, and has stated a policy of strengthening its own animation production. All these indicate the growing value of entertainment-related IP assets.

In the 22/2 issue, we will be covering Z Holdings (4689), Yamaha Motor (7272), Fukuoka Financial Group (8354), and Kadokawa (9468).

・Established in 1996 as a subsidiary of the current Softbank G (9984). Involved with Ecommerce and media businesses. Had a change in company name from Yahoo Japan on 2019/10. Finalized an agreement for business integration with LINE (3938) on 2019/12.

・For 9M (Apr-Dec) results of FY2021/3 announced on 3/2, revenue increased by 15.0% to 873.815 billion yen compared to the previous period, and operating income increased by 15.1% to 142.226 billion yen. Against the backdrop of stay-at-home demand, ZOZO (3092) became a consolidated subsidiary in November 2019, and sales and earnings growth at subsidiary ASKUL (2678) and eBook Initiative Japan (3658) had contributed to results.

・For its full year plan, revenue is expected to increase by 8.3% amounting to 1.14 trillion yen compared to the previous year, and operating income to increase by 5.1% to 160.0 billion yen. Business integration with LINE is scheduled to be completed in March this year. LINE launched its banking service “LINE BK” in Thailand in October last year as a joint venture with Kasikorn Bank. With the number of accounts reaching one million in less than three months and the balance of loans to individuals reaching 10 billion yen, LINE is gaining recognition in Thailand as a “super app” that provides a full range of services.

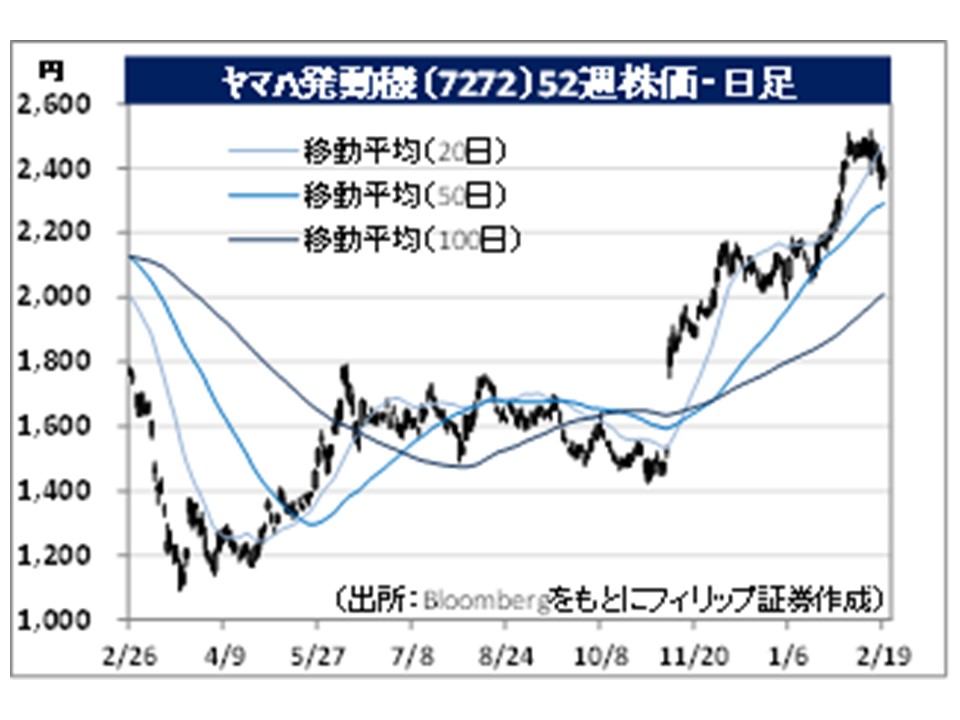

・Established in 1963 by separating from Nippon Gakki Co., Ltd (current Yamaha Corp). Operates the Land Mobility business (motorcycles, etc), the Marine Products business (outboard motors, etc), the Robotics business (surface mounters, etc), and the Financial Services business.

・For its FY2020/12 results announced on 12/2, net sales decreased by 11.6% to 1.4712 trillion yen compared to the previous year, and operating income decreased by 29.2% to 81.672 billion yen. After bottoming out in the 2Q (Apr-Jun) period, company started to recover, with the Robotics and Financial Services businesses seeing increased sales. However, the decline in sales volume of motorcycles in the Land Mobility business and the Marine Products business owing to the Covid-19 pandemic had impacted results.

・For FY2021/12 plan, net sales is expected to increase by 15.5% to 1.7 trillion yen compared to the previous year, and operating income to increase by 34.7% to 110.0 billion yen. Company sees rising transportation costs due to global container shortages and difficulty in procuring parts owing to semiconductor shortages as risks. With Taiwan’s TSMC planning to invest 20 billion yen to establish a development base in Japan for back-end semiconductor manufacturing, company’s strength in back-end bonding and molding equipment is likely to attract attention.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: