Company background

Venture Corporation Limited (VMS) was founded in 1984 as a global electronics manufacturing services (EMS) provider. VMS capabilities expanded from assembly and manufacturing into research, design and development, product and process engineering, design for manufacturability, supply chain management, as well as product refurbishment and technical support across a widely diversified range of high-mix, high-value and complex products. Headquartered in Singapore, the Group comprises more than 30 companies with global clusters in Southeast Asia, Northeast Asia, America and Europe and employs over 12,000 people worldwide.

Investment thesis

Initiate coverage on VMS with a BUY rating TP of S$17.68

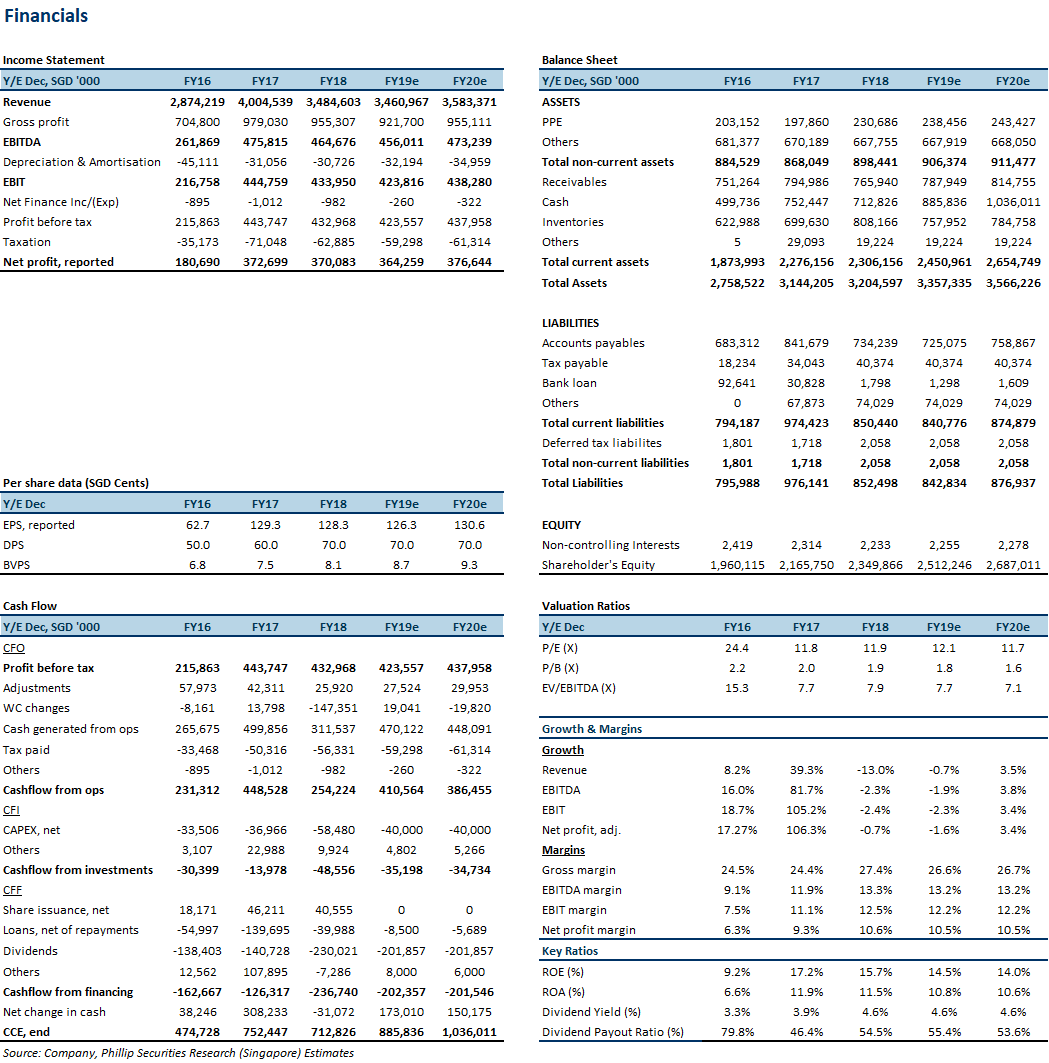

Our valuation is based on a 14x PE multiple. Our valuation is conservative given VMS’s superior return on equity, profit margin and balance sheet. We expect VMS dividend yield to be stable at 4.6%.

Revenue

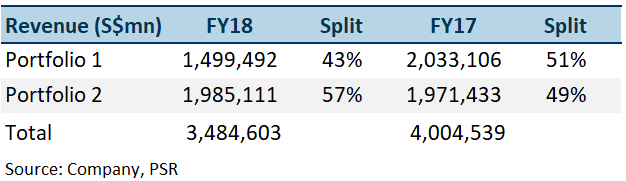

VMS generates revenue by providing technology services, products and solutions. We can essentially split VMS’ revenue streams into two main segments.

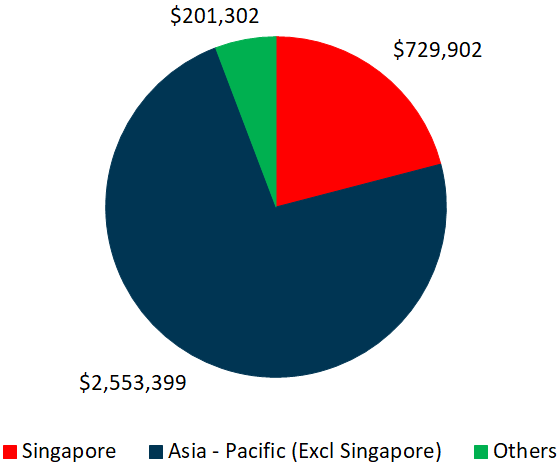

Figure 1: FY18 Geographical breakdown of revenue

Source: Company, PSR

Figure 2: Group revenue by technology domain

Design revenue accounts for more than 50% of total revenue. This is a rare feat in the contract manufacturing space. We believe VMS’ ability to maintain a profit margin of 10.6% is due to its extensive capability in R&D which results in value creation and customer stickiness. VMS generally prices its services by internal benchmarks. VMS is also selective with its customers as it aims for quality growth. Among its peers, VMS is ranked 6 out of 7 in terms of revenue while it ranks first in terms of net profit. We believe portfolio 1 will provide growth for VMS as it shifts away from its legacy businesses (portfolio 2).

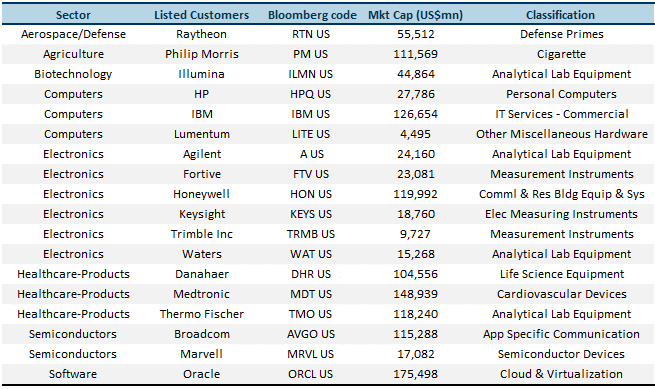

Key Customers – Positive outlook

VMS serves more than 100 customers globally. Figure 3 shows the potential customers of VMS. We think Philip Moris, Illumina and Keysight are likely to be VMS’s key customers.

Figure 3: List of potential customers

Source: PSR

Philip Morris

Philip Morris (PM) is an international tobacco company engaged in the manufacture and sale of cigarettes, smoke-free products and associated electronic devices and accessories.

VMS is one of the few manufacturers producing PM’s I-Quit-Original-Smoking (IQOS) product. IQOS is a smoke-free product which heats tobacco units up to a temperature of 350 degrees without combustion. PM claims IQOS produces less harmful chemicals as compared to normal cigarettes.

Korea and Japan: Despite slight weakness in PM’s sale of Reduced Risk Products (RRP) in Korea and Japan, we believe VMS’ on-going introduction of IQOS products in new markets should offset some of the softness in Korea and Japan.

The United States: On 30 April 2019, the Food and Drug Administration (FDA) approved the sales of IQOS 2.4 in the United States. In recent news, lawmakers in the United States urged the FDA to immediately pull pod-based and cartridge-based e-cigarettes off the market due to an outbreak of lung disease. IQOS faces less regulatory scrutiny than e-cigarettes. This may have a net positive impact to PM’s IQOS heat not-burn-product as consumers have fewer alternatives available.

Figure 4: PM’s heated tobbaco product (IQOS)

Source: Company

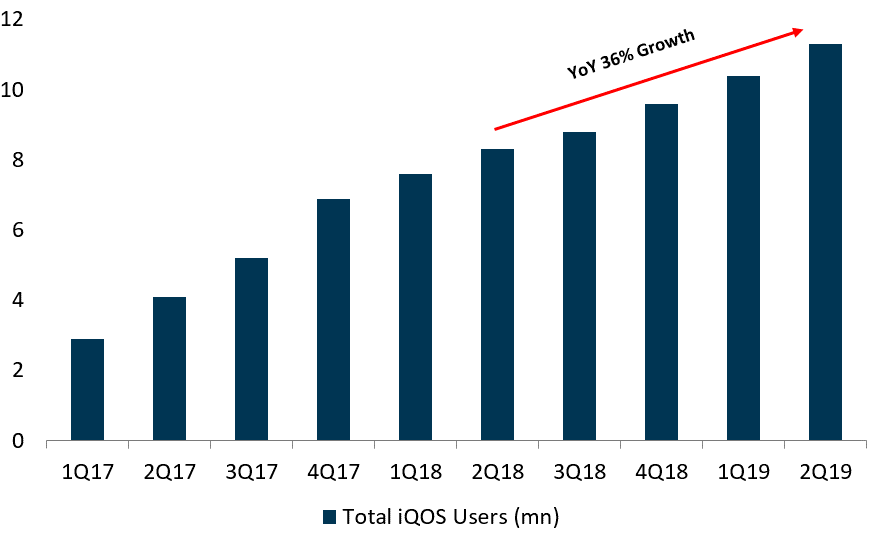

Figure 5: Total iQOS users rising rapidly

Source: Company, PSR

Illumina

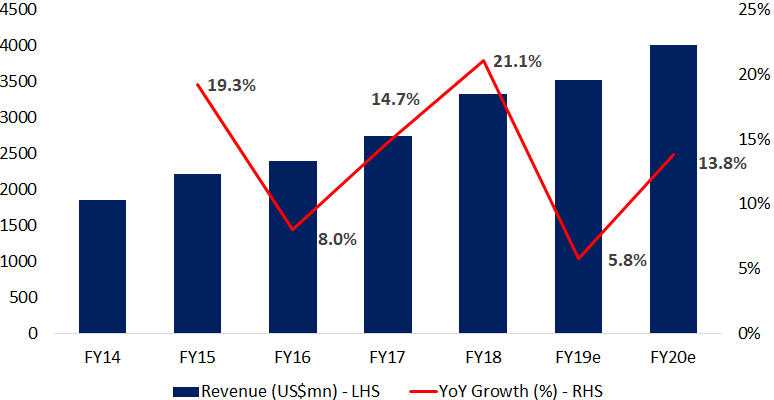

Illumina provides sequencing and array-based solutions for genetic analysis. Its products are designed to accelerate and simplify genetic analysis. Illumina’s products include integrated sequencing and microarray systems, consumables, and analytical tools. Over the last 5 years, Illumina enjoyed revenue CAGR of 12.4%. The outlook for Illumina is positive as it continues to gain market share in genomic sequencing. Illumina is also enjoying healthy growth in its NovaSeq portfolio of products.

Figure 6: Illumina’s revenue trend

Source: Bloomberg, PSR

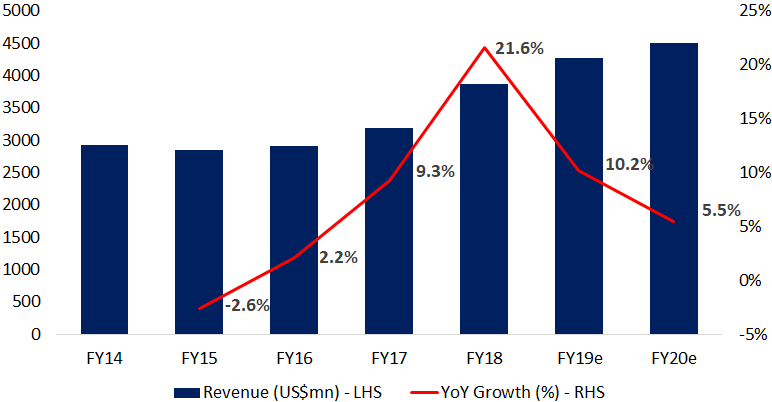

Keysight

Keysight offers electronic measurement services using wireless, modular and software solutions.

In FY18, Keysight achieved revenue growth of 21.6% YoY. As of 3Q19 results, Keysight raised its outlook for FY19 with expected revenue growth of 9% to 10% citing strong enterprise demand and 5G.

Figure 7: Keysight’s revenue trend

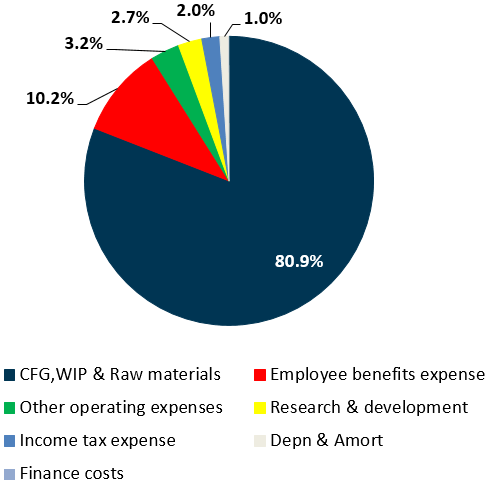

Expenses

Majority of VMS’ expense is made up of changes in finished goods, work in progress and raw materials used, making up 81% of FY18’s total expenses (Figure 8).

Staff costs: VMS currently employs more than 12,000 workers globally, with staff costs accounting for 10% of FY18’s total expenses. VMS margin expansion is in part the ability to keep employee expenses hovering at a steady rate of 10% of total annual expenses since FY15 despite expanding its operations.

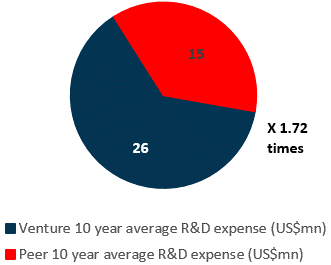

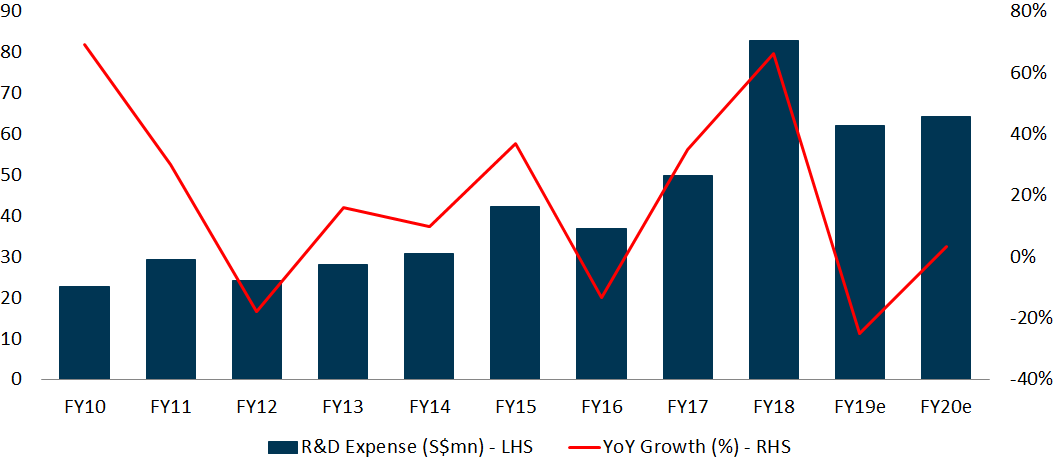

Research and Development (R&D) costs: VMS is spending 1.72x more on R&D as compared to peers over the last 10 years (Figure 9). We believe this has allowed it to provide more value add to the customer, entrench the relationship and penetrate earlier into new projects. In FY18, VMS’ R&D expenditure surged 66% to S$83mn while peers were relatively muted at an average of S$23mn. We believe VMS’ consistent R&D efforts will lead to more value creation to support its impressive profit margin.

We expect R&D expenses to decline from its peak in FY18 (Figure 10). Although R&D expense is commonly used to gauge future turnovers of EMS companies, we think for VMS, it may not hold true. The fluctuations in VMS’ R&D expense may be due to timing differences as it is purely customer-driven. R&D expenses are recognised after reaching certain milestones this is done in different phases. The recognition of milestones is decided by customers and could range from 25% of a new product launch (NPI) to 100% of an NPI. Upon completing an NPI, customers may add or modify its products thereby delaying milestones and hence delaying the recognition of VMS’ R&D expenses.

Figure 8: FY18 expense breakdown

Source: Company, PSR

Figure 9: VMS spends 1.72x more on R&D VS peers

Source: Company, PSR

Figure 10: Research and development expense trend (S$mn)

Tax expenses: VMS recently initiated a tax optimisation programme which centralised all of its taxes. As of 2Q19, the effective tax rate was brought down to 13.7% from 15% a year ago. We expect the steady-state of the effective tax rate to be in a range of 14% to 14.5% going forward. The initiative could potentially save VMS approximately S$2mn in tax expenditure annually.

Gaining industry profit pool

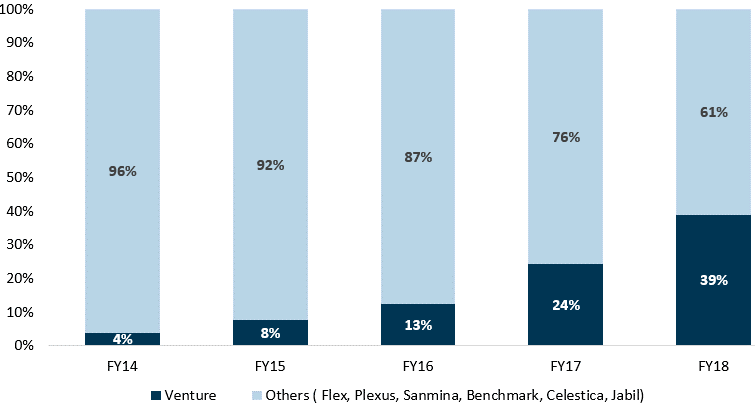

We combined the GAAP earnings of US-listed EMS peers to visualise the gain in profit share VMS accumulated throughout the years. VMS’ profit pool grew from 4% of the industry to 39% in less than five years (Figure 11). We believe VMS’s ability to gain profit share is attributable to its (i) Extensive R&D capabilities; (ii) Adoption of lean cost structure; (iii) Selective customer acquisition; and (iv) Focus on low volume, high mix projects.

Figure 11: VMS is consistent in gaining profit pool amongst peers

Source: Bloomberg, PSR

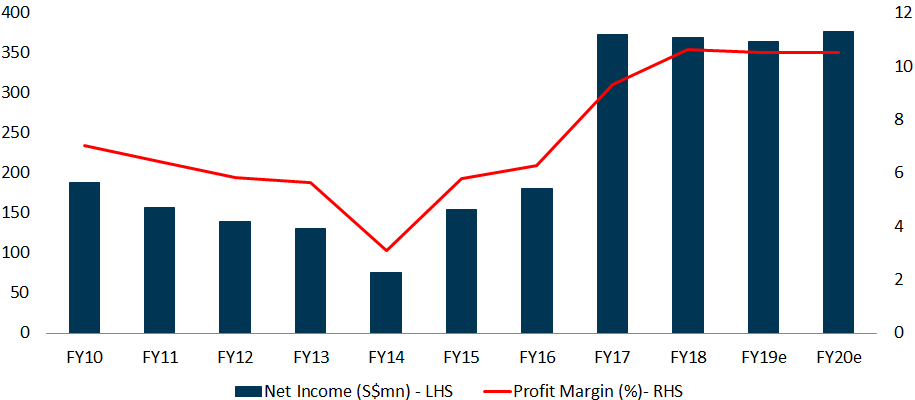

Peer average net profit margins are approximately 2% (inclusive of foreign & local peers) while VMS enjoys 10% (Figure 12).

Figure 12: Net income and profit margin trend

Source: Company, PSR

We forecast an EPS growth of -1.6%/3.4% YoY for FY19e/FY20e respectively. We expect net profit margin to remain stable at 10.5% for both years. NPI should offset any weakness from a slowdown in existing production.

Robust balance sheet – Dividend support

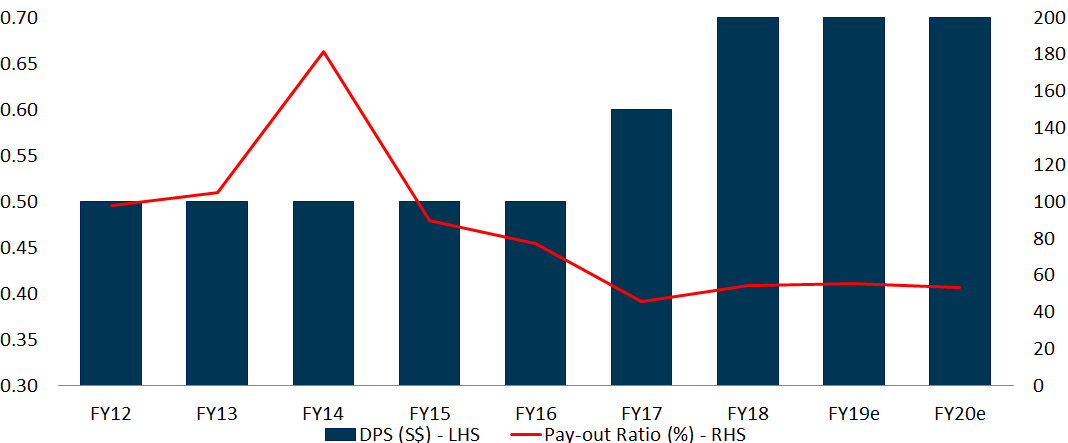

Dividend visibility for VMS is backed by its strong balance sheet. As of 2H19, VMS has a net cash position of S$760mn which is approximately 17% of its market cap. Net cash to equity is at 32%. With a strong cash generation and a robust balance sheet we can expect consistency in dividend payments and potential share buybacks. We forecast VMS to pay S$202mn in dividends in FY19e, this equates to a pay-out ratio of 55% and a yield of 4.6% at current share price.

Figure 13: VMS has expanded dividends 40% over the past 3 years

Source: Company, PSR

Outlook

VMS near term outlook is shrouded by escalating geopolitical tensions and the prolonged trade war. Its focus will be on selected domains that have growth and value creation opportunities. Strong initiatives are in place for building new differentiating capabilities to enhance the Group’s competitiveness. With its strong balance sheet, VMS is well placed to capture growth opportunities as and when they arise.

Strong South East Asia presence

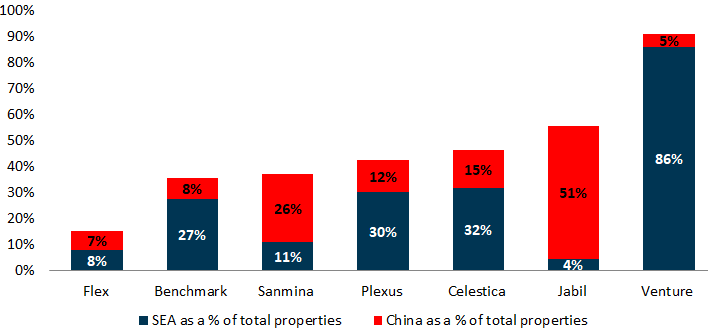

VMS will be a long-term beneficiary from the supply chain disruption in China due to the ongoing trade dispute with the United States. VMS’ exposure in China only accounts for 5% of its total properties (Figure 16). Note that there is less than 2% of turnover directly impacted by the trade dispute.

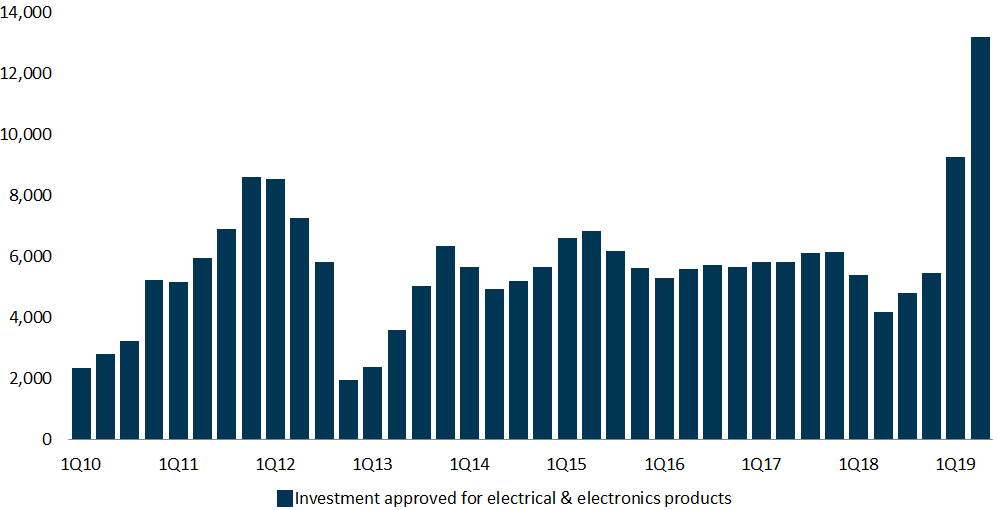

Among its peers, VMS has the largest (86%) proportion of its production facility in SEA (Figure 16), namely in Malaysia (Figure 19). From our discussion with manufacturers and analysis of various announcements, there is an ongoing shift of the electronics supply chain from China into SEA (Figure 15). In addition, we have observed a surge in electrical and electronic investment approvals in Malaysia (Figure 17). VMS is poised to benefit due to its existing production capacity in SEA.

Figure 15: Relocation of electronics manufacturing from China to Malaysia is underway

Source: Nikkei Asian Review, The Edge, NST, Bloomberg, WSJ

Figure 16: VMS has the largest facilities in SEA and is least exposed to China

Source: Company, PSR

Figure 17: Spike in investment approved in electrical & electronics products (MYR mn)

Risk factors

Increased competition. Competitors could ramp up their R&D efforts to mimic VMS’ success and possibly win over VMS’ clientele. This will erode the premium margins that VMS commands. This scenario is rather unlikely because the cost for VMS’ customers to switch may outweigh the benefits, switching entails a long design and development process.

Escalation in the trade war. Increased trade tension could weaken customer sentiment and hence, delay new product launches and tapering down of inventory. Escalation could also further weaken global economies therefore negatively affecting end-user demand.

Stringent regulation. Increased regulation on PM’s IQOS product is likely to hurt turnover.

Investment thesis

Valuation

We initiate VMS with a target price of S$17.68. Our valuation is based on a 14x PE multiple this is in line with peer valuations. Our valuation is conservative given VMS’s superior return on equity, profit margin and balance sheet. VMS also boasts a dividend yield of 4.6% which we expect to be stable (Figure 13).

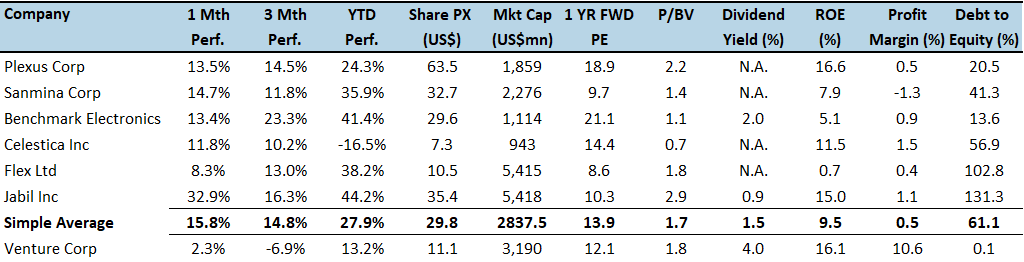

Figure 18: US-listed peer valuations

Source: Bloomberg, PSR

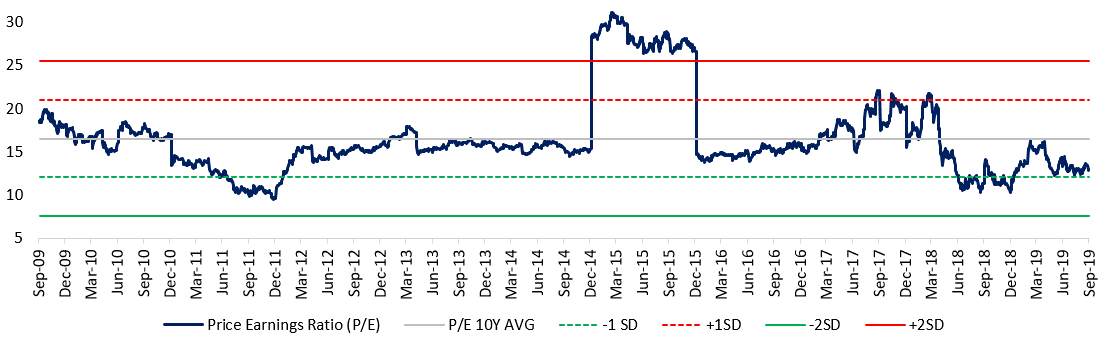

Figure 19: VMS trading at -1SD

Source: Bloomberg, PSR

Figure 20: List of properties

Source: Company, PSR

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Alvin covers telecommunication and technology sector.

He graduated with a bachelor of commerce, majoring in Accounting and Finance from Monash University.