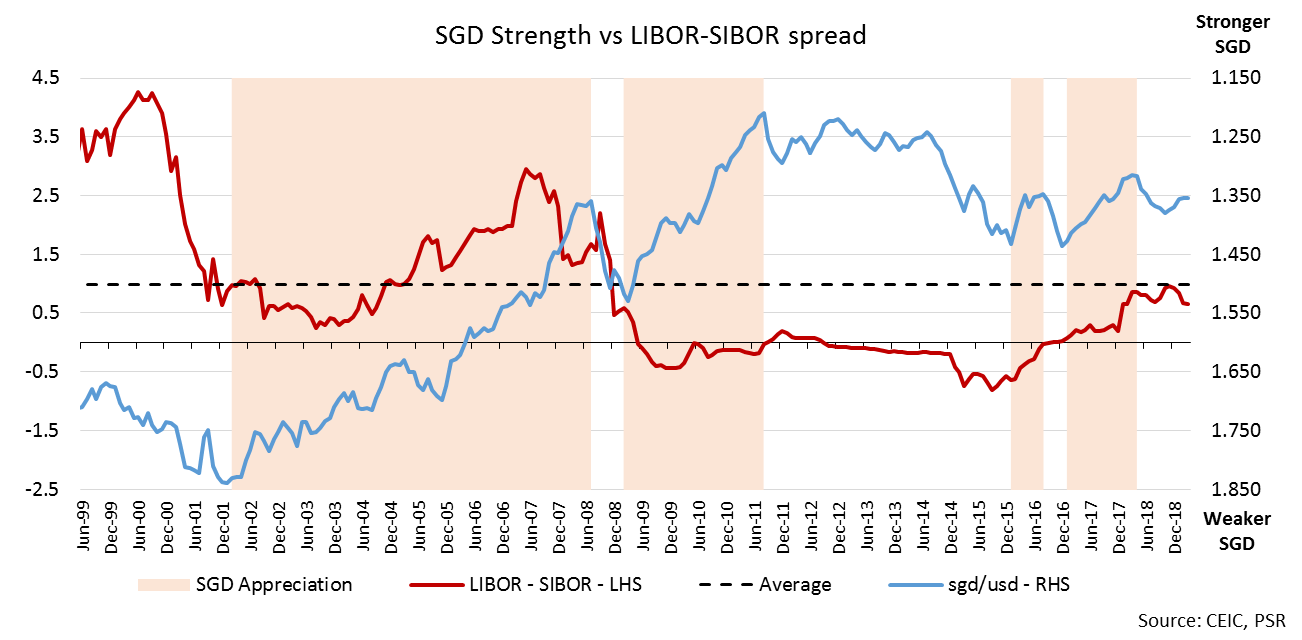

Relationship between SGD strength and LIBOR-SIBOR spread

During periods of strength in SGD, the 3-month LIBOR-SIBOR spread tends to widen (Figure 1). We expect SIBOR to remain elevated. Firstly, the March 2019 LIBOR-SIBOR spread is only at +0.66% as compared to the historical average of +1.00%. Secondly, unless the SGD depreciates significantly, it is unlikely for this positive spread to narrow further. As per Figure 1, the LIBOR-SIBOR spread tends to widen during periods of SGD appreciation and vice versa. Unless there is a significant depreciation of the SGD, we do not expect the LIBOR-SIBOR spread to narrow much more.

Figure 1: When SIBOR is lower than LIBOR, the SGD tends to depreicate against USD

Interest Rates – Lagged effect of interest rate pass-through

We believe there is still room for SIBOR and SOR to rise in the next three months due to the lagged effect of interest rate pass-through from the US Federal Reserve rate hikes. However, with the recent pause in a rate hike and dovish stance from the Fed, now is the best and probably last time for Singapore banks to hike their board rates and reprice their loans before interest rates start to tail down.

NIM supported by an increase in board rates

After the implementation of further property cooling measures in July 2018, mortgage volume fell, and UOB was wary of increasing interest rates too soon. Coupled with their drive to raise fixed deposit funds, UOB was facing pressure on Net Interest Margin (NIM) improvements, resulting in relatively flat NIM in FY18.

NIM growth for 1Q19 and 2Q19 will arise mainly from UOB’s retail mortgage book repricing while SIBOR and SOR remain elevated. Around half of the mortgage book could be repriced from the hike in board rates with the full effect on NIM to be seen in 2Q19. Although wholesale loans are tricker to reprice due to the more substantial bargaining power of institutions, UOB will be able to grow fee income from product and service expansion (i.e. loan restructuring fee).

CASA Deposits – Contracting CASA Ratio in the Sector

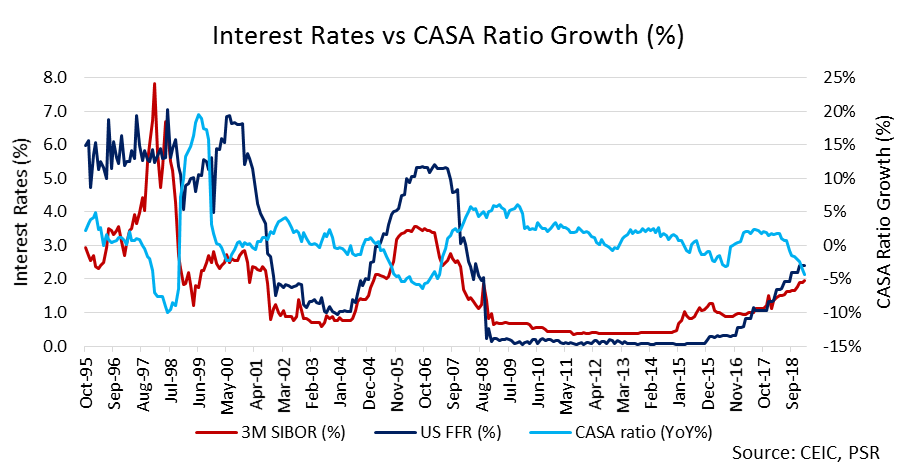

UOB’s 4Q18 CASA deposits growth slowed to 5.2% YoY, the slowest in 3.5 years; while fixed deposits grew 7.8% YoY, faster than FY18’s average of 3.7% YoY. With a higher proportion of fixed deposits in the deposits mix, the cost of funds rises, making it challenging to achieve NIM expansion. However, we expect competition for fixed deposits to taper off in the next 3-6 months and funding pressure to ease since there are no more rate hikes expected in 2019.

Figure 2: The historical trend of CASA ratio growth decelerating whenever the 3M SIBOR rises

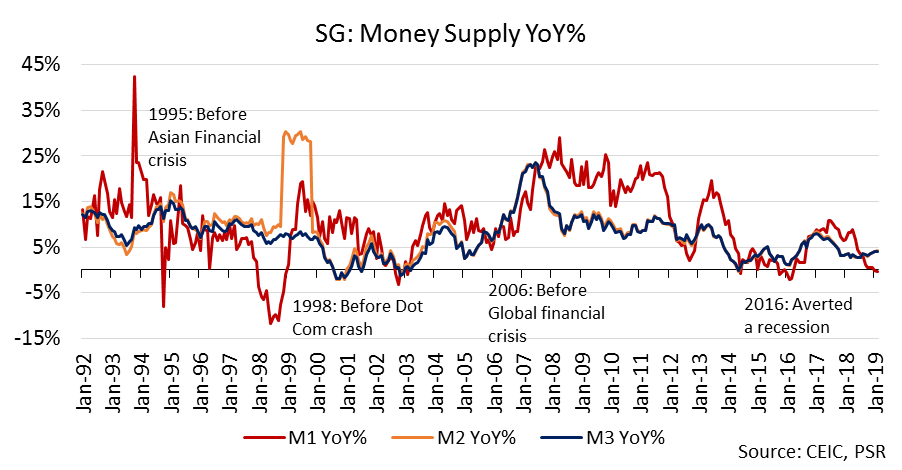

Figure 3: The historical trend of M1 YoY growth decelerating whenever there is a financial crisis

As interest rates rise, the amount of demand deposits decreases as investors redirect their funds into higher yielding investments such as fixed deposits. As a result, we saw the growth of money supply M1 slowing to 0.4% YoY in Feb’19 while M2 and M3 rose 4.2% and 4.1% YoY respectively.

Loans Growth – Weaker in 2019

Mortgage loan growth will still be available for UOB due to the progressive drawdown of the mortgage. We forecast a 4.5% mortgage growth for UOB in FY19e, in line with the low-single-digit guidance. Overall loans growth continues to be held up by demand from non-bank Financial Institutions and Property funds. Property funds have healthy demand for loans in their commercial properties and even data centres development or acquisition activities. UOB’s market share of SGD loans and deposits in Singapore remains sizeable at 23% and 21%.

Asset Quality – Low residual risks from the O&G sector

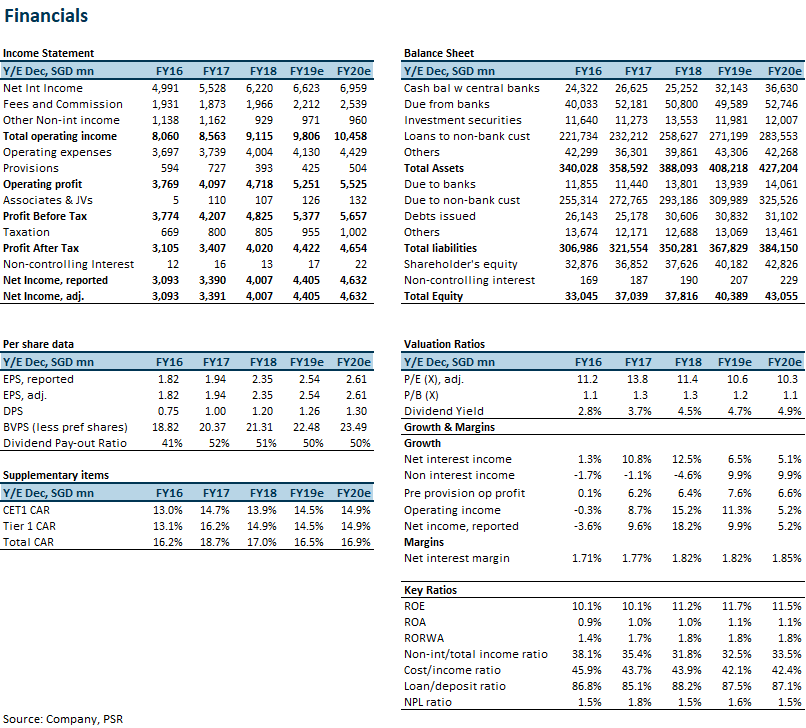

Ample provisioning has been done for the Oil and Gas (O&G) sector loans. UOB provided for as much as 70-80% of its O&G exposure with collaterals marked down by 90% of its asset value. There is currently no systemic issue across the O&G sector. New NPA formation has been trending towards normalised levels of around S$500m each quarter. UOB practices conservative provisioning for wholesale loans, whereby certain loan defaults that have yet to past the 90 days limit (set by the Monetary Authority of Singapore) were classified as Non-Performing Loans (NPLs). All three banks have similar NPL ratio of 1.5% as of FY18. Our FY19e NPL ratio for UOB is 1.55%, in line with guidance.

Dividends – Robust Capital Ratios

UOB’s dividend policy is for full-year dividend payout to be at 50% (including special dividends, if any), subject to a minimum CET1 ratio of 13.5%. As of December 2018, all three banks have similar CET1 ratio of 14%. We expect the robust capital ratios to sustain current payout levels and we forecast UOB’s FY19e dividend yield at 5%.

Prudential Deal

UOB renewed its bancassurance deal with Prudential on 10 January 2019 for 15 years for a sum of S$1.15bn paid to UOB by Prudential. The S$1.15bn income will be amortised over this period. UOB will be distributing Prudential’s suite of products as part of the wealth management services but not limited to Prudential if the requested product by the customer is unavailable.

Digital Bank in Thailand

The newly launched UOB digital bank in Thailand targets the middle-affluent, mobile-savvy millennials who want to be engaged in a new type of banking platform. UOB’s Digital Bank aims is to gather deposits at the moment. The ability to transfer funds that are offline into an online platform was made accessible with the launch of PromptPay in 2017. PromptPay is an interbank mobile payments system backed by the Thai government to enable money transfers at a cheaper rate than those offered by traditional Thai banks. UOB’s Digital Bank partners with the local telecommunication companies to assess the creditworthiness using the phone bill payment history of its customers.

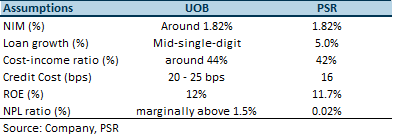

Table 1: UOB guidance vs. PSR estimates for FY19e

Investment Actions

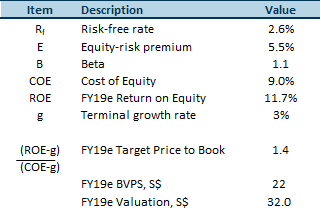

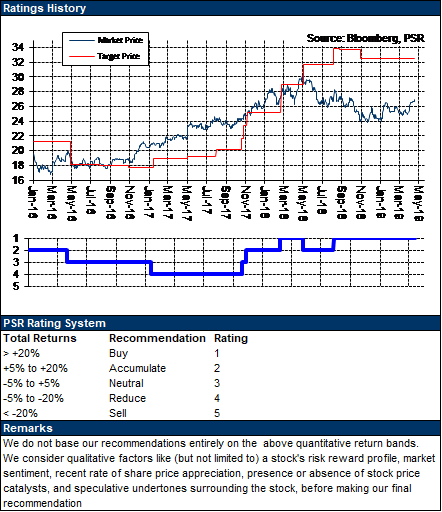

Maintain BUY with a lower target price of S$32.00 (previous TP S$32.50) based on the Gordon Growth Model. Due to the increasing funding pressure from steep growth in fixed deposits and flat loan growth in the banking industry, we pen in a more conservative FY19e NIM forecast of 1.82% (previously 1.84%), resulting in a lower target price. Even after achieving record high ROE in FY18, UOB guided a higher ROE of 12% in FY19e, showing that the effective cost measures, NIM improvement and low provisions should provide further upsides to earnings in 2019. We forecast earnings growth of 7.6% and a dividend yield of 4.7% in FY19e.

Valuation: Gordon Growth Model

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Min Ying covers the Banking and Finance sectors. She has experience in external audit and corporate tax roles.

She graduated with a Bachelor of Accountancy with a major in Finance from SMU.