Company Background

Established in 1989 and listed on the SGX in 2014, UG is a disposable-glove manufacturer with two factories in Malaysia. It makes and distributes gloves under its proprietary “Unigloves” brand to more than 2,000 customers in 50 countries, including the UK, Germany, US, China, Brazil and Nigeria. Around 55% of its gloves are latex and the balance nitrile. Industries served include healthcare, food and beverage, electronics, beauty, etc. Annual production capacity is 2.9bn gloves, with plans to expand to at least 3.2bn by FY21e.

Investment Merits

We initiate UG Healthcare with a BUY rating. Our target price is S$2.70. This is based on 15x PE FY21e. The average discount to peers for UG since listing has been around 40%.

REVENUE

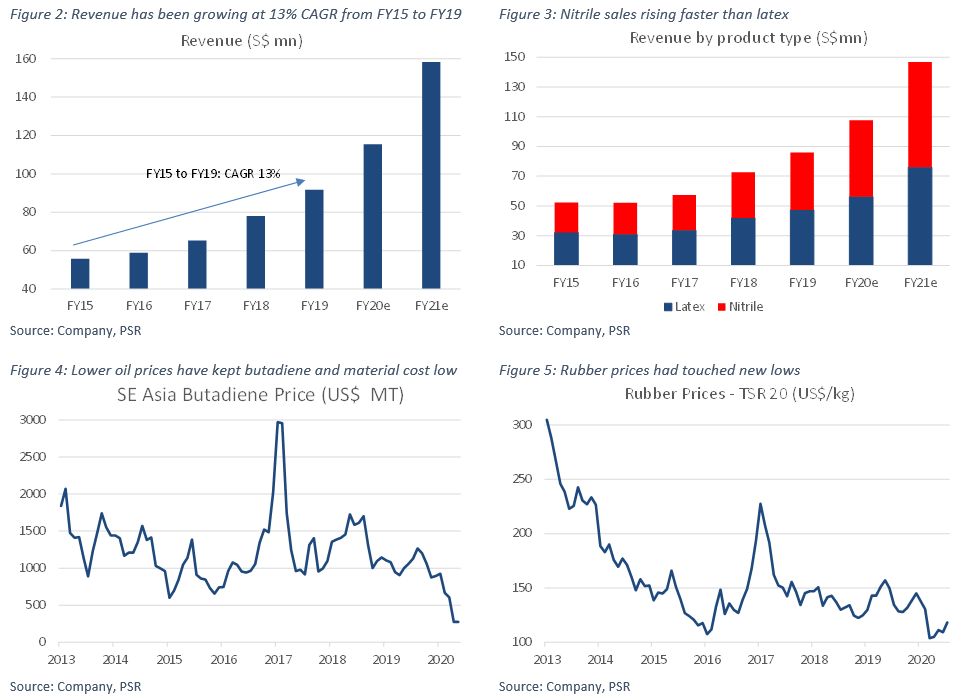

Revenue for UG can be split into two large product types, latex (55% of sales) and nitrile (45%)*. Nitrile gloves are predominantly used in healthcare industries in developed countries due to regulations. Meanwhile, latex is used more in emerging markets due to the lower price, comfort and higher sensitivity of such gloves. UG produces many types of gloves that can be differentiated by their weight, raw material, thickness, colour, scent, barcode, etc. Another source of revenue is the sale of ancillary products such as surgical, vinyl and cleanroom gloves, face masks, and other medical disposables. By geography, the major markets for UG are the UK, Germany, Brazil, China and Nigeria. Revenue for UG has been growing around 13% CAGR from FY15 to FY19 as the company expanded production capacity (Figure 2). In FY20 and 21, we expect revenue to surge due to the spike in selling prices. Nitrile gloves are expected to grow faster than latex (Figure 3).

*Latex gloves are made from natural rubber and can be classified into powdered and powder-free. In the past, latex gloves were powdered with cornstarch for easier donning and to prevent sticking. But this can cause a sensitive or allergic reaction to the skin when worn for long periods. Powder-free gloves undergo chlorination that provides a slippery effect on the glove surface to ease donning and removal of the glove without the need for powder. Nitrile gloves are made from petroleum-based synthetic rubber.

EXPENSES

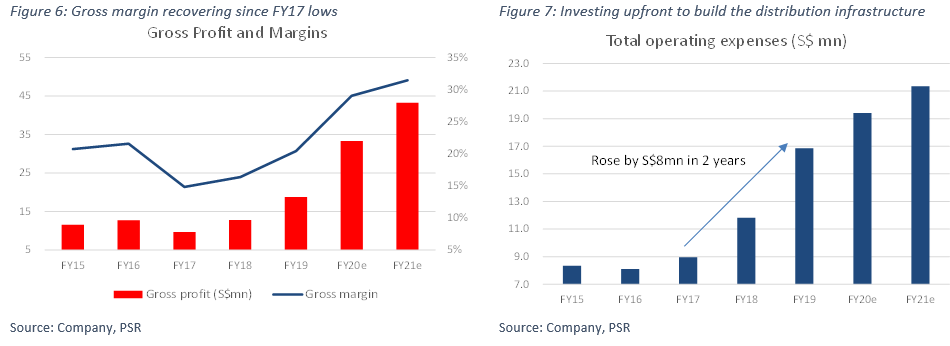

The breakdown of manufacturing cost are raw materials (55-60%), labour cost (10-11%) and other overheads such as utilizes, depreciation (30-35%). The type of raw material for natural latex gloves is natural rubber latex. Meanwhile, nitrile gloves are made from synthetic rubber (i.e. nitrile latex). The feedstock in the production of nitrile is the petrochemical butadiene. The prices of butadiene have been stable in-line with the weaker crude oil price (Figure 4). Rubber prices similarly are at record lows (Figure 5).

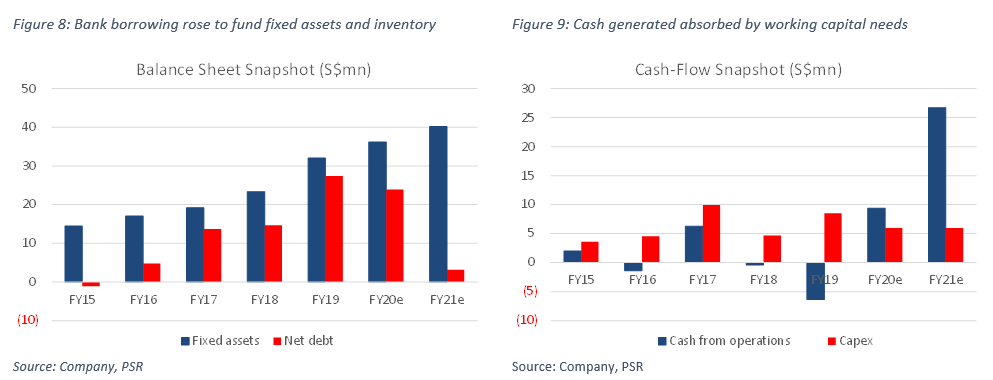

Operating expenses include selling and distribution (3% of sales), administrative expenses (13%) and other operating expenses (2%). The last three years have seen a doubling in operating expense from S$8.1mn in FY16 to 16.8mn in FY19 (Figure 7). Marketing and administrative cost have risen the past two years as the distribution network expanded into new countries such as Brazil. UG had to invest fixed cost such as warehouse and new marketing and sales teams.

MARGINS

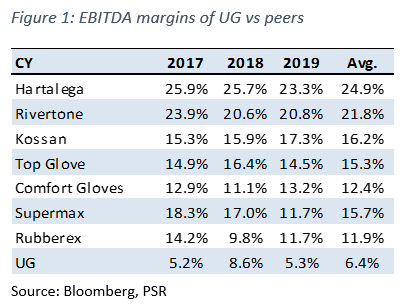

EBITDA margins for UG have 6% for the past three years. This is below larger peers such as Riverstone (22%), Top Glove (15%), Hartalega (25%) and Supermax (16%) – Figure 1 The lower margins is due to UG lower production capacity and economies of scale. Without the higher volume, fixed cost per unit will be higher. Besides, the utilization rate will be lower due to higher downtime and smaller batch production runs. Higher contribution from nitrile sales is another factor to margins. Both Hartalega and Riverstone sell only nitrile gloves.

The two years where margins were weakest was in FY17 and FY18. Margins were negatively impacted by higher material cost, gas tariff hike, foreign worker levy and higher depreciation from new product lines. The supply disruption in global butadiene supply caused nitrile latex prices to spike in early 2017. Whilst, difficult to quantify, the margins are higher than typical OEM manufacturer because of the distribution margins which UG can capture.

OTHER INCOME

There are two categories of other income

BALANCE SHEET

Assets: Fixed assets of the company has doubled over the past four years (FY15-19) to S$32mn (Figure 8). The rise in assets is in tandem with capacity and revenue doubling over a similar period. Conversely, inventory tripled during these four years. Expanding the distribution network into new markets requires warehouse and inventory to become available to customers.

Liabilities: UG swung from net cash of S$1mn to net debt of S$27mn from FY15 to FY19. Debt was required to fund the growth in fixed assets (+S$17mn) and inventory (+$21mn).

CASH-FLOW

Cash-flow from operations has generally been negligible. Any cash generated has been used to fund inventories and receivables. Accumulated operating cash-flow from the past four years has been a negative S$2mn. Meanwhile, capex required was around S$7mn p.a. between FY16 to FY19, as the company doubled its production capacity from 1.4bn to 2.9bn.

INDUSTRY

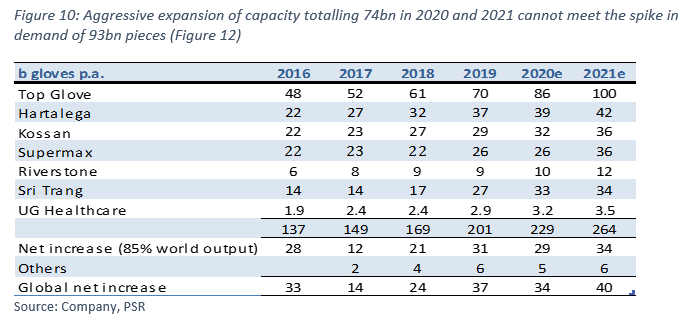

The global rubber gloves industry is dominated by Malaysia exporters. In 2019, Malaysia accounts for 67% of global production followed by Thailand the 2nd largest at 19%, according to MARGMA*. Over the past three years, global demand for gloves has been rising at a CAGR of 12.5% or 29bn pieces a year (Figure 10). Pre-Covid 19, demand for gloves have been driven by increased spending in healthcare, ageing populations, rise in non-communicable diseases, increased regulation and improvement in hygiene, especially in developing countries.

When the Covid-19 pandemic struck, the first wave of demand came China. As the pandemic spread, demand from the healthcare sector soaked up large amounts of the supply. The second wave of demand will now come from non-traditional or healthcare sectors and resumption of economic activity as lockdown eases.

Our expectations are for glove demand to rise by 20% in 2020, or 60bn pieces, followed by a 33bn increase in 2021. Our assumptions around demand are:

UG BUSINESS MODEL

Large glove manufacturers such as Top Glove and Hartalega are largely OEM manufacturers. OEMs manufacture gloves for under the brand of their customers such as large medical distributors (e.g. Medline, OneMed, Marbena, Cardinal Health, Microflex, Ansell, Kimberly Clark), government agencies (Defence or Health Ministries) and non-profit organizations (e.g. WHO, United Nations).

OEMs are not keen to build their own distribution network. Firstly, this is to avoid any conflict of interest. Secondly, managing warehouses and logistics in the destination markets is not their core expertise especially compared to the scale of their production. Another challenge in distribution is the huge variety of products to be stocked and sold, not just a single product – gloves.

The typical logistics or sales cycle is as follows: UG manufactures the gloves from its factory and ship to its warehouses in the UK, China, Brazil and Germany. UG services many end customers that may just order several cartons every week. UG needs to have sufficient stock to meet such consistent orders for next day delivery. For effective sales, UG needs a local sales team to promote the brand, speak to customers, engage in marketing activities and provide after-sales support.

For more than a decade UG has spent building a distribution network for its own branded gloves. It started with Germany and this has now grown to major emerging countries such as Brazil, Nigeria and China (Figure 14, Figure 17). Brazil is a notable country with high barriers to entry due to the need for every glove to be barcoded.

Investment Merits

1. A surge in demand. Covid-19 has resulted in a sharp spike in demand, precipitating severe industry shortages. Industry order lead times have multiplied from one month before Covid to 12 months. Ex-factory spot prices for nitrile gloves have skyrocketed from US$25 to US$120 per 1,000 pieces. The three levers of demand are: a) quantum jumps in the number of hospital patients, frequency of use and typically low inventories, which have led to a scramble for gloves; b) hospitals, governments and NGOs have started to build buffers or strategic stocks to prepare for future spikes in demand; and c) the new normal of hygiene practices has necessitated the use of gloves by consumers and non-healthcare industries such as airlines, airports and restaurants.

2. Capturing the entire supply chain margins. Since listing, UG has been investing aggressively in its brands, logistics, warehouses and end-customer network. Sales from its Unigloves brand have leapt from around 50% of the total in 2015 to 85%. Own-brand products offer higher customer stickiness and selling prices. UG can also capture distribution margins. With a network that reaches out to end-customers directly, UG can benefit from higher end-selling prices of gloves and enjoy both manufacturing and distribution margins for its premium branded gloves.

3. Shortage should persist till 2021. Demand for gloves worldwide was already growing at a CAGR of 10.6% before Covid. We believe the current shortage will persist into 2021. Firstly, glove penetration in emerging markets such as China and Brazil is only 10 and 24 pieces per capita respectively. This compares with 100 and 150 for Europe and the US. UG can benefit from growth in both countries, as it has been entrenching its brand and distribution networks in China and Brazil since 2002 and 2014 respectively. Secondly, industry supply is not expected to meet demand growth even in 2021. Demand was growing by around 30bn a year before Covid. This year, it is expected to grow by 60bn and another 33bn in 2021, as the pandemic has created new growth drivers (Figure 12). This surge of almost 93bn in two years is above expected increases in planned glove capacity of around 74bn (Figure 10). If we assume a 90% utilization rate for the industry, actual supply addition will only be around 67bn pieces.

Risks:

1. A decline in selling price. The largest impact to margins and earnings will be a drop in selling prices for gloves. The current shortfall in supply has triggered a spike in prices. We expect the demand-supply imbalance to continue into 2021. Our assumption for prices is still conservative considering the recent spike (Figure 27).

2. Import restrictions from the U.S. On 16 July 2020, Top Glove announced the U.S. Customs and Border Protection has placed a detention order on disposable gloves manufactured by two of the Company’s subsidiaries. The urgent need for gloves plus a shortage of supply, there will be pressure to ensure sufficient supply for hospitals and medical workers.

3. Additional taxes imposed by Malaysian authorities. In the past, notably palm oil, the Malaysia government has imposed windfall taxes on the palm oil industry due to the surge in palm oil prices. An windfall tax will have dire consequences to the equity markets in Malaysia where the combined market capitalization of rubber glove companies total around RM170bn.

Valuation

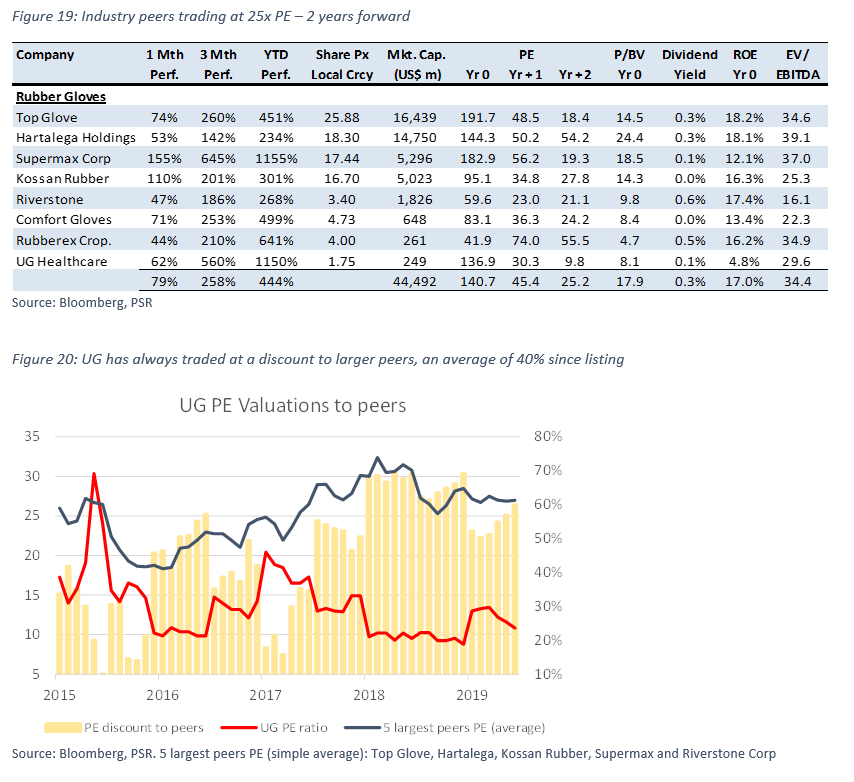

We initiate coverage on UG Healthcare with a BUY recommendation. We peg UG to a PE of 15x FY21e. It is a 40% discount to peer valuations of around 25x PE (Figure 19).

UG has always traded at a discount to its larger peers due to its lower scale, growth and liquidity. The discount has widened recently to 60% due to the weaker financial performance of UG, in our opinion. We believe this discount can shrink to back to at least the historical average since listing of around 40x PE as the financials start to turnaround for UG (Figure 20).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.