Description

Starbucks Corporation (NASDAQ:SBUX) is a roaster, marketer and retailer of coffee. As of October 2016, the Company operated in 75 countries. The Company operates through four segments: Americas, which is inclusive of the United States, Canada, Latin America; China/Asia Pac; Europe, Middle East and Africa, and Channel Development. The Company’s Americas, CAP and EMEA segments include company operated and licensed stores. Its Channel Development segment includes roasted whole bean and ground coffees, Tazo teas, Starbucks and Tazo branded single serve products, a range of ready-to-drink beverages, such as Frappuccino, Starbucks Doubleshot and Starbucks Refreshers beverages and other branded products sold across the world through channels, such as grocery stores, warehouse clubs, specialty retailers, convenience stores and the United States foodservice accounts.

Source: Thomson Reuters

Investment Rationale

SBUX reported their Q1 earnings on Thursday, 25th January, with non-GAAP EPS of USD0.65, up 25% YoY, beating consensus estimates of USD0.57. However, revenue came in at USD6.07bn, which missed consensus estimates by USD110.00mn. As such, SBUX share price tumbled by 4.2% to USD57.99. While SBUX disappointed with its weak holiday sales in the USA, its China segment grew same store sales by 6% YoY. We believe that the dip has caused SBUX to be undervalued and represents a buying opportunity for the coffee giant.

Recent Price Action: SBUX has been range bound between USD54.00 to USD64.00 since end 2015. Slowing domestic growth has caused the stock to underperform the major indexes. SBUX had been climbing towards the end of 2016 on the back of the tax reform; however, its recent earnings report caused it to dip more than 4%.

Strong momentum in China: SBUX has shown very strong momentum since it started rolling out stores in China. In the latest earnings, the Company reported a 6% growth in same-store sales for China and 30% revenue growth. They also reported entry into seven new cities and over 3,100 stores in China.

Enthusiasm for SBUX seems to remain strong in China. Its new Starbucks Reserve Roastery opened in Shanghai on the 6th December 2017 and has been performing incredibly well since. SBUX mentioned that the Shanghai Roastery is doing double the average weekly US Starbucks store sales per day after eight weeks of operations.

With China still a distant second when it comes to total revenue; China/Asia Pacific total net revenue came in at USD3.24bn for FY17, while Americas came in at USD15.65bn, we believe that China continues to hold great potential for growth for SBUX.

Rewards Program: SBUX has also been prioritizing their digital footprint by way of their Starbucks Rewards program. We believe that the Rewards program is helps encourage repeat spending by members as well as allow direct marketing through personalized offerings. As such, we find it encouraging that SBUX has been able to add over 1.4mn new members in USA, an increase of 11% YoY, with member spending accounting for over 30% of US company operated sales and Mobile pay representing 11% of US company operated transactions.

Along with the increase in cashless payments, SBUX has also entered into partnerships with different companies like Chase, Tencent, and Alibaba to explore digital payments. Its Shanghai Roastery collaborated with Alibaba’s Taobao app and online marketplace, Tmall, to allow customers to purchase merchandise as well as whole bean coffee to be delivered to their homes. SBUX also partnered with Chase and Visa to launch a Co-branded credit card later in February as well as a stored value card later in April. SBUX mentioned that with only 14mn of their 75mn unique customers signed up, there is great potential to leverage digital technologies to market and establish a more direct relationship.

Valuations: SBUX closed at USD57.99 and trades at a forward PER of 22.88, with a dividend yield of 2.07%. SBUX 4 year average PER is 28.8 and its 10 year low PER is 17.82. SBUX has total debt of USD3.93bn, with USD2.69bn in Cash and equivalents. SBUX’s annual net income has also been growing consistently. However, it has been slowing in recent years, with revenue only growing 5% and profit decreasing 1% in its recent FY results. However, SBUX pays over 30% effective tax rate, and as such, it should greatly benefit from the tax reform when it reports in FY18. SBUX also recently increased their dividends in the end 2017. It now pays an annual dividend of USD1.20 per share, yielding 2.07% at current prices. This amounts to an annual payout of about USD1.45bn. SBUX was able to generate USD 2.66bn in Free Cash Flow in FY17. As such, we believe that SBUX is undervalued at this price despite the headwinds they are facing.

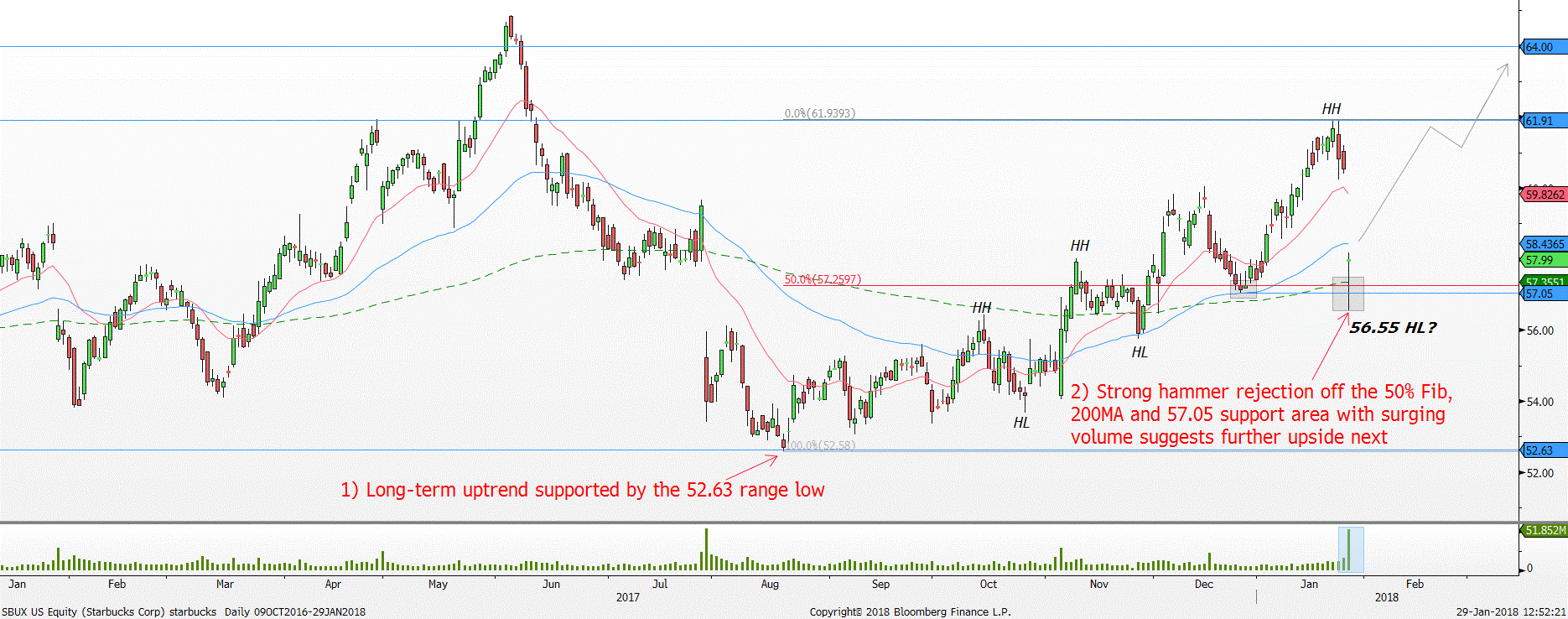

Technicals: Since August 2017, SBUX has reversed back into the long-term uptrend after finding some strong support at the 52.63 range low. The general uptrend structure of Higher Highs (HH) and Higher lows (HL) followed as the 20 and 60 day moving average propelled price higher. Even after the recent selloff, the general uptrend remains intact.

SBUX Daily chart – Strong hammer rejection off the 57.05 support area

Source: Bloomberg, PSR

Support 1: 57.05 Resistance 1: 61.91

Support 2: 55.63 Resistance 2: 64.00

Red line = 20 period moving average, blue line = 60 period moving average, Green line = 200 period moving average

The most recent price action saw SBUX plunging on 26 January 2018 where it broke below the 20 and 60 day moving average. At one point, SBUX was down -6.6% on 26 January 2018, but buyers were ready to defend the confluence of support area at the 200-day moving average, 50% Fibonacci retracement level and 57.05 support area showing sign of strength. As a result, a bullish reversal bar (hammer) with surging volume was formed signalling a reversal higher next.

Expect the uptrend to resume next for price to continue forming the series of Higher Highs (HH) and Higher Lows (HL). For this up-leg, buyers should be targeting the 61.91 resistance area followed by 64.00.

The 26 January 2018 hammer’s low of 56.55 could very well be the next higher low point within this uptrend.

Conclusion: We are bullish on SBUX due to 1) China growth, 2) Membership Rewards plan and 3) Historically low valuations. As such, we believe that stock is undervalued and the recent dip represents a buying opportunity.

![]()

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: