Company Background

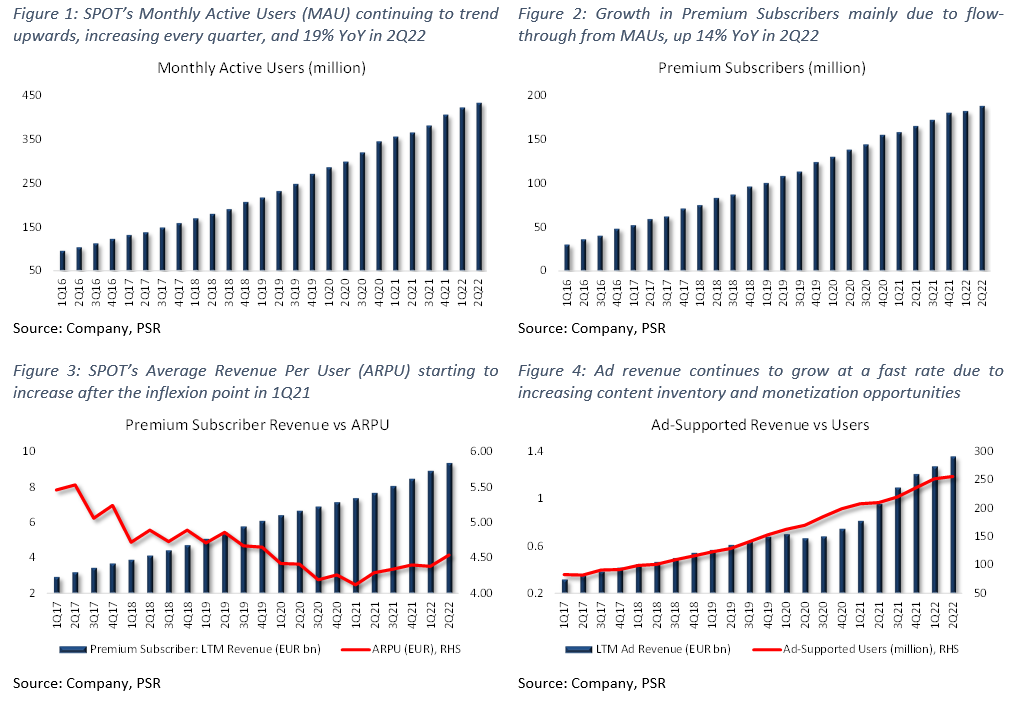

Spotify Technology S.A. operates the world’s most popular audio streaming subscription service with >430 million monthly active users across 180+ countries and territories. The bulk of its total revenue comes from premium service subscriptions (87.5%), and the remaining 12.5% comes from advertising revenue in its ad-supported segment. Spotify currently has the largest market share (31%) in the global audio streaming industry, with more users than the next 2 closest competitors combined.

Investment Highlights

We Initiate coverage with a BUY rating and a target price of US$117.00 based on DCF valuation, with a WACC of 7.5% and terminal growth of 3%.

REVENUE

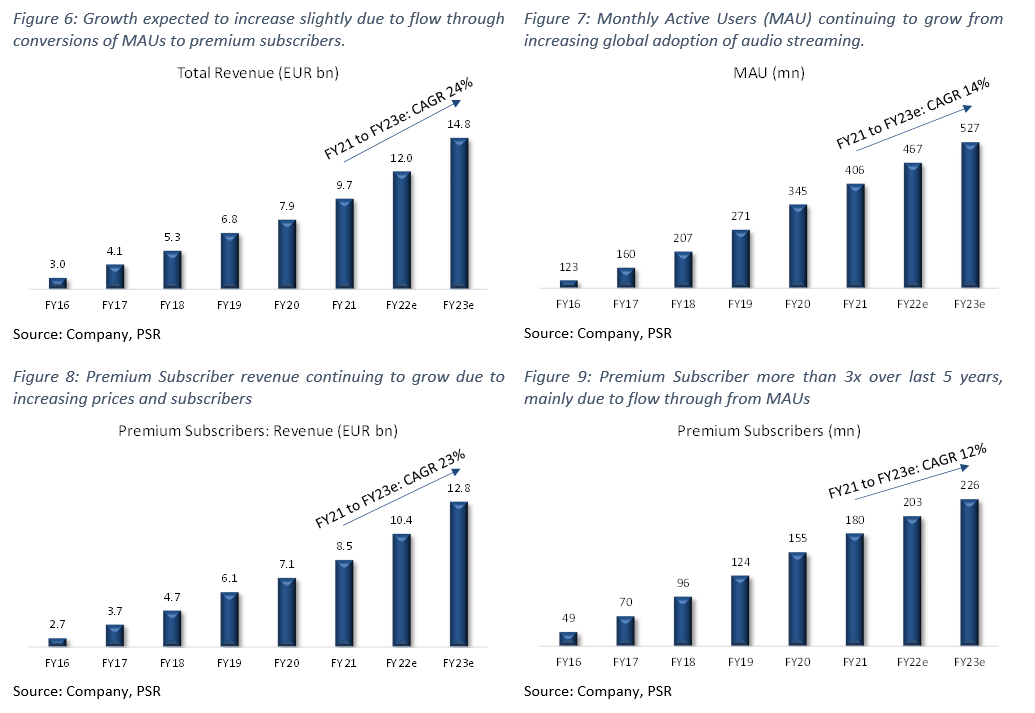

SPOT posted EUR9.7bn in revenue for FY21, increasing 23% YoY (Figure 6), with the majority (87.5%) of its total revenue coming from its premium service subscriptions, and the remaining 12.5% coming from advertising revenue in its ad-supported segment.

Premium Subscription: SPOT generated about EUR8.5bn in revenue for this segment last year, growing 19% YoY (Figure 8), with a 5-Yr CAGR of 26%. From the company’s latest 2Q22 filings, revenue from premium subscriptions came in at EUR2.5bn, up 22% YoY (14% YoY in constant currency), primarily due to a follow-through effect on subscriber gains. Revenue in this segment is earned mainly through the sale of its premium services – on-demand and offline listening. This service is sold both directly to end-users, and also through distribution partners such as telecommunications companies. The premium service is typically paid for on a monthly recurring basis, with average revenue per user (ARPU) the main metric used to monitor pricing trends. ARPU had been declining due to expansion into lower-priced regions but has since reached an inflexion point as a result of strong pricing power, increasing QoQ since 1Q21.

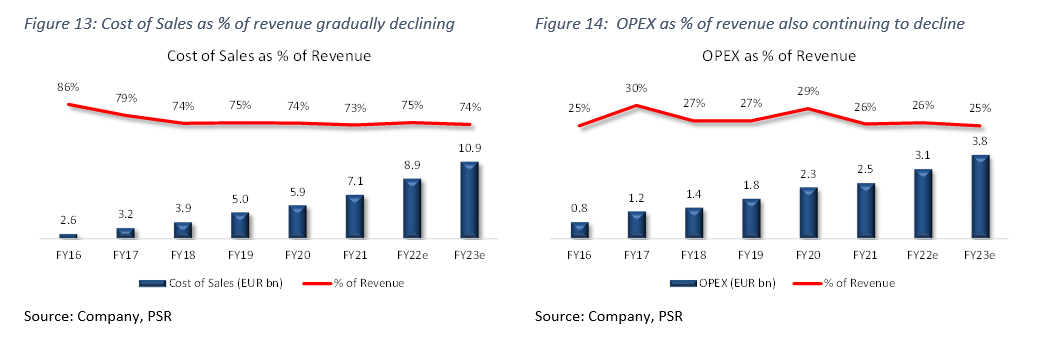

Ad-Supported: SPOT generated about EUR1.2bn in ad-supported revenue for FY21, with a growth rate of about 62% YoY (Figure 10), and a 5-Yr CAGR of 33%. Ad-Supported revenue for 2Q22 grew 31% YoY (17% in constant currency), led by growth in ad impressions and cost per 1000 impressions (CPM). Revenue from this segment is generated primarily from the sale of display, audio, and video advertising through ad impressions across the company’s music, podcast, and audiobook content. Advertising arrangements are usually sold on a cost-per-thousand basis and recognized when impressions are delivered on the platform

Revenue Growth: We forecast total revenue for FY22e to hit EUR12bn, which would represent a 24% YoY growth, supported by a combination of FX tailwinds, increasing premium subscribers, and increasing ad revenue. Revenue from premium subscribers in FY22e is expected to hit EUR10.4bn (23% YoY), primarily from subscriber growth and slight increases in the subscription price. Ad-supported revenue is expected to grow 30% YoY to EUR1.6bn, on the back of increasing ad impressions.

RULE OF 40

The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared with just a single period growth rate. Adding together SPOT’s 3-year average revenue growth of 23% and its EBITDA margin of 2%, the total of 25% is less than our required threshold of 40% (Figure 12). However, we do expect EBITDA margins to continue rising due to SPOT’s growth in operating leverage.

EXPENSES

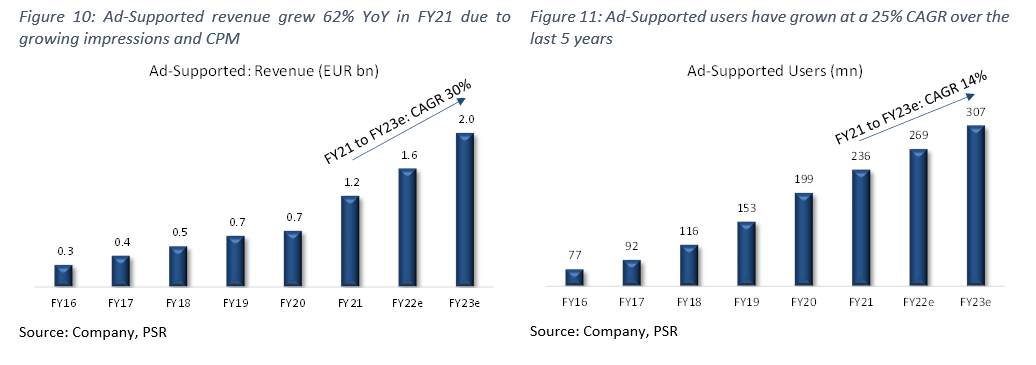

SPOT’s cost of sales grew 21% in FY21 to EUR7.1bn (Figure 13), slightly below the total revenue growth of 23%. Cost of sales (73% of total revenue) encompasses mainly royalties and distribution costs related to content streaming paid to third parties – record labels, music publishers, etc. Through FY21, the company had paid more than EUR26bn in royalties, making them one of the largest engines for revenue growth to artists and labels in the music industry.

Premium subscriber cost of sales grew 17% YoY, but decreased slightly as a percentage of premium subscriber revenue from 72% in FY20, to 71% in FY21. The YoY increase was mainly driven by growth in premium subscribers and increases in publishing licensing rates. Ad-supported cost of sales grew 48% YoY, but decreased as a percentage of ad-supported revenue from 99% in FY20 to 90% in FY21. The YoY increase was mainly due to higher royalty and revenue-sharing costs due to growth in advertising revenue and increases in publishing rates.

Operating expenses include research and development (9% of revenue); sales and marketing (12%); and general and administrative (5%). R&D expenses grew 9% YoY, primarily due to personnel-related costs as a result of increased headcount to support growth. Sales and marketing expense grew 10% YoY, primarily due to a EUR128mn increase in advertising costs for marketing campaigns. General and administrative expenses increased only 2% YoY. Total Operating Expense for FY21 was EUR2.5bn (Figure 14) – 26% of revenue.

MARGINS

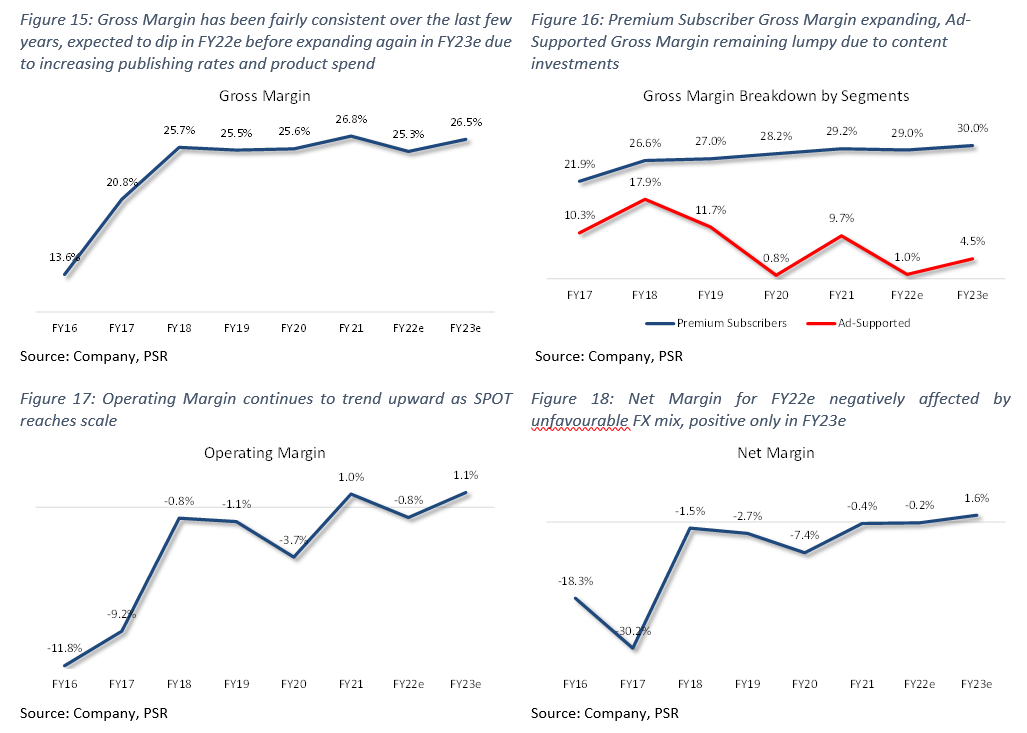

SPOT’s gross margin was 27% in FY21, and has been gradually improving over the last 5 years (Figure 15). Premium subscriber gross margin was 29.2% in FY21, up 1% YoY, and an increase of 7.3% from FY17 – 21.9% (Figure 16). The increase was primarily due to certain benefits from marketplace programs and beneficial changes in rights holder liabilities estimates. Ad-supported gross margin was 9.7% in FY21, compared with 1% in FY20 (Figure 16). The sharp increase was primarily due to a decrease in streaming delivery, ad servicing, and production costs as a percentage of revenue.

Typically, gross margins have been relatively low due to high royalties paid out to record labels and music rights holders, and continued investments in building up its Podcast and Audiobook content. However, we do expect gross margins to start climbing as the company begins slowing its product investments as a % of revenue over time. Management has also reiterated its goal for gross margins to be in the 35-40% range moving forward.

Operating margin was 1.0% in FY21, and has been steadily increasing over the years – up from -12% in FY16 (Figure 17). We forecast operating margins to dip slightly in FY22e due to unfavourable FX headwinds – SPOT has a larger percentage of US Dollar denominated expenses, but to resume its path upwards in FY23e and beyond, mainly due to increasing operating leverage.

Net margin in FY21 was -0.4%, and has been improving YoY, with positive net margins expected for the first time in FY23e as the company leverages on its growing user base and increasing pricing power (Figure 18).

BALANCE SHEET

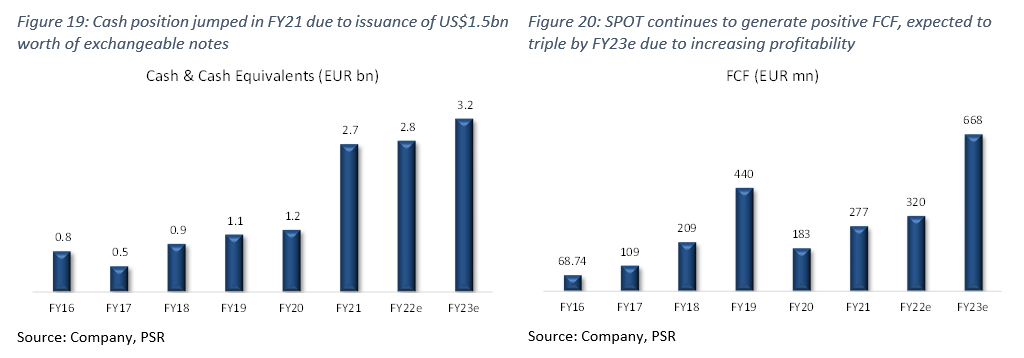

Assets: Cash and cash equivalents increased by about EUR1.6bn YoY in FY21 to EUR2.7bn (Figure 19), largely due to a EUR1.2bn issuance of exchangeable notes, and improving cash generated from operations. Short-term investments were at EUR756mn, and generally consist of commercial paper, corporate debt securities, collateralized reverse purchase agreements, and government and agency debt securities, with an average duration of less than 2 years.

Liabilities: SPOT’s largest current liability was its accrued fees payable to rights holders of its streaming content, and was EUR1.4bn in FY21 – falling within accrued expenses and other liabilities category.

US$1.5bn Exchangeable Notes

SPOT issued US$1.5bn worth of 5-year 0% exchangeable notes in FY21, and it was the company’s largest non-current liability. These notes mature in March 2026 with a strike price of ~US$515 per ordinary share (around 5x its current price). Net proceeds for this issuance was EUR1.2bn after transaction costs. The company will be able to repay the notes with its net cash hoard of EUR2.1bn by 2023e.

CASH-FLOW

Free Cash Flow (FCF) grew 51% YoY in FY21 to EUR277mn (Figure 20) and has been increasing at a 5-Yr CAGR of 32%. We expect FCF to triple by FY23e on the back of increasing profitability and operating leverage.

BUSINESS MODEL

Similar to how Netflix has transformed the way people consume on-demand visual entertainment, SPOT has also provided consumers the ability to stream music on demand, transforming the music industry through its >80 million tracks – including >4.4 million podcast titles. The company has also reiterated its decision to actively invest in other forms of alternative and spoken word content like audiobooks and podcasts to complement its existing music library – through direct ownership or licensing arrangements. SPOT also leverages on relationships in the music industry, data analytics, and software, to build and enhance a two-sided marketplace for both users and creators, empowering creators by unlocking new monetization opportunities, and reshaping the way users enjoy, discover, and share audio content. SPOT’s two distinguished services – premium and ad-supported, live independently of each other, with ad-supported services acting as a funnel that drives a significant portion of premium subscriber additions.

Premium Subscription: SPOT provides its premium subscribers unlimited online and offline high-quality streaming access (via PC, mobile, and tablets), to its library of music, podcasts, audiobooks. Subscribers also have the option of choosing from a variety of price plans – Standard, Family, Duo, Student. Prices vary between plans, and are adapted to local markets to align with consumer purchasing power. Subscriptions are usually recurring on a monthly basis, but SPOT has also expanded to include prepaid options and durations other than monthly (longer or shorter durations) to cater to local markets. Most of the new premium subscribers are generally sourced from converting ad-supported users through online platform and marketing engagements.

Ad-Supported: No subscription or platform fees, provide users with limited on-demand online access to music catalogue, but unlimited access to podcasts via PC, mobile, tablets. It also serves as both an acquisition channel for premium subscribers, and a free option for users who are unable or unwilling to pay a monthly subscription fee. Revenue is generated via the sale of video, display, and audio advertisement placements. Advertising arrangements are usually sold on a cost-per-thousand basis. SPOT is also constantly looking to introduce new advertising products across all catalogues. An example of this would be the introduction of an audio advertising marketplace, Spotify Audience Network (SPAN), with SPOT acting as an enabler helping publishers sell targeted advertisements to brand partners. The prospect of monetization has been successful in incentivizing content creators into publishing more content into SPAN, which has in turn made it more attractive for advertisers to be a part of this ecosystem, creating sort of a flywheel effect which will benefit the growth in Ad-supported revenue. Revenue from this segment is reliant on the number of users, total hours of content consumed, and SPOT’s ability to provide relevant innovative advertising products.

INDUSTRY

SPOT is the leader in audio streaming services globally, with almost the same number of subscribers as the next 3 platforms combined (Figure 23). As of FY21, SPOT had an estimated 31% market share in the global audio streaming market, based on subscriber base – almost twice that of its nearest competitor Apple Music. Other competitors include YouTube Music, Amazon Music, SiriusXM, and Pandora. The company’s highest penetrated countries are developed regions like North America and Europe, with other regions such as Asia still in its early stages of adoption (Figure 24).

The global audio streaming industry has continued to grow at a 3-YR CAGR of 19% since FY18, with users also growing at a similar CAGR of 18%. Several factors have contributed to this: 1) increasing smartphone penetration globally has allowed more users to consume on-demand audio wherever they go; 2) traditional radio usage has been declining, with digital consumption taking its share, particularly with car usage being a huge use case in North America. We do expect growth rates to come down slightly, to about 9% CAGR over the next 4 years, mainly due to a huge adoption wave over the last 2 years that was driven by COVID-19 (Figure 25). Similarly, we expect the growth in users to slow to about 7% CAGR over the same period moving forward (Figure 26).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.