SECTOR SNAPSHOT

S-REIT yield and yield spread expanded 73bps and 177bps to 514bps and 442bps (+1.4 SD level) respectively as at 15 April 2020.

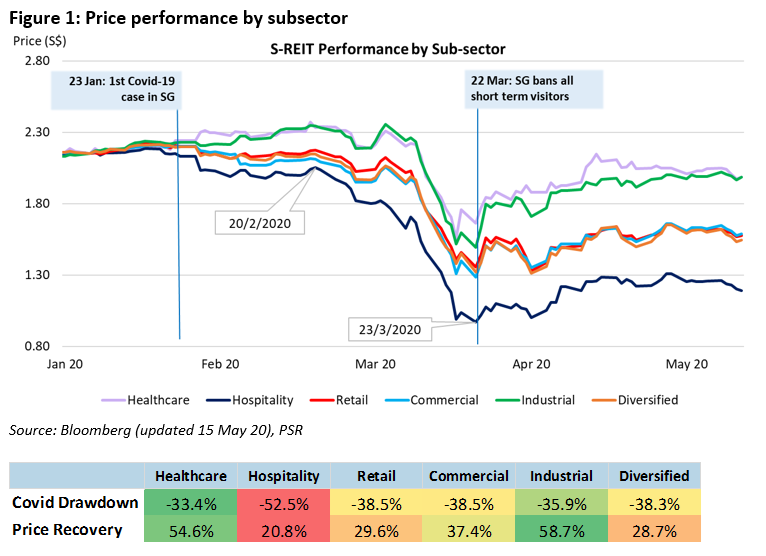

COVID-19 has impacted the subsectors differently. At the peak of the market sell-off, S-REITs experienced an average decline of 40% in prices. The smallest decline of 33% was registered by the healthcare sector, while the largest drop of 53% was seen in the hospitality sector. The retail, commercial and industrial REITs declined within the range of 36% to 39%.

The recovery since has been varied as well – the seemingly more resilient healthcare and industrial sectors have recovered roughly 55% to 59% of their fall in share prices, while the commercial sector has recovered by 37% and retail by 30%, with hospitality recovering only 21% of their value (figure 1).

Impact across subsectors

The impact to the REITs will vary according to the underlying tenants’ reliance on premises to generate income. This will determine the degree of disruption to businesses, the amount of rental assistance required, as well as the future demand for spaces, which will be altered by both occupiers’ and consumers’ behavioural shifts such as increased telecommuting and adoption of e-commerce platforms.

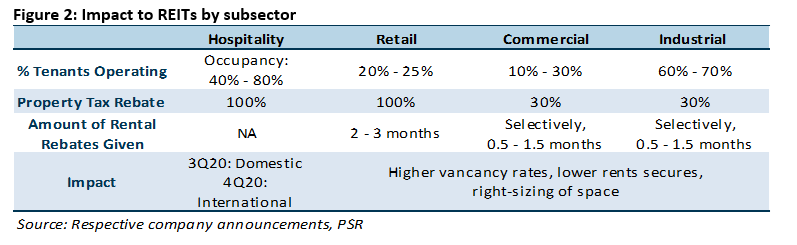

The immediate impact on FY20 earnings will be offering of rental rebates and higher vacancy rates. More rental rebates were given to tenants whose revenue generation is highly dependent on their premises and who were unable to operate due to the lockdown – such as the retail and F&B sectors. While the commercial and industrial sectors’ tenants have a moderate to low dependency on their premise, REITs are prepared to/have offered targeted relief to tenants who are more in need of help, such as the retail and small medium enterprises (SMEs) with their portfolios. As such we expect the rental relief given to commercial and industrial tenants to have minimal impact to distributable income.

Rental rebates offered will lower FY20 revenues and DPUs for the REITs. Among the subsectors, retail REITs have given the most rental relief to their tenants (2 to 3 months) as only 20% to 25% of their tenant were operating during the circuit breaker. These rental rebates from landlords come on top of relief packages from various governments to help cushion the COVID-impact on businesses, such as wage support and property tax rebates/deferments to be passed onto underlying tenants.

Weaker leasing due to lower business formations and expansions, as well as rightsizing. Landlords have some reprieve given that tenants are locked in by their existing leases. Signing of new leases were challenging, which was exacerbated by lockdowns, making physical inspections less possible. Moving forward, expansions and new demand are expected to be muted in the short term, due to lower business formations and deferment of business expansions. We will likely see more lease renewals, along with some right-sizing of space which will lead to higher vacancy rates.

Most REITs have tapered their reversion expectations downwards and are prepared to adopt more flexible leasing strategies, such as trading rental fees for occupancies. Hence, we are expecting lower rents and negative rental reversions in the near-term. Demand for retail and office space may be weaker due to the familiarisation and convenience of e-commerce and viability of telecommuting, however, logistics and data centres assets which support future trends of e-commerce and cloud adoption may see receive greater interest.

Cashflows remain the priority for REITs. Some REITs have retained distributions in the most recent quarter to meet any cashflow requirements that may arise from cashflow mismatch should tenants request for rental deferments. Most REITs concur that cash conservation and a robust balance sheet is key to tide through this challenging period. While some REITS have chosen to postpone or cancel asset enhancement initiatives (AEIs), and non-essential CAPEX, some REITs have decided to push ahead with their AEIs, utilizing this period where leasing activity is softer to update and improve assets.

The raising of leverage limits from 45% to 50% will give REITs more breathing room should asset values deteriorate and added flexibility to draw on debt facilities to meet any short-term cashflow needs. While acquisition ambitions have taken a backseat due to the lower share prices, making acquisitions less accretive, most REITs are willing to dip into their pockets should a good opportunity surface. Having a strong cash position will allow the REITs to remain both offensive and defensive during the crisis.

Revaluations largely unchanged, still a waiting game. Valuation is a trifactor methodology, incorporating i) present value of cashflows from the asset (which are affected by rental growth assumptions), ii) comparable transaction and iii) capitalisation rates. Capitalisation rates have remained largely unchanged given the absence of transactions during this COVID-19 period. Most asset owners (including SREITs) are well capitalised and under no pressure to liquidate assets. Conversely, many SREITs are on the lookout for potential acquisition opportunities. Valuers are reluctant to make any large adjustments to valuations without transactional evidence and will likely omit fire-sales which are inaccurate representations of market conditions.

According to CBRE’s April 2020 cap rate flash survey, investors are expecting capitalisation rates for shopping malls to expand up to 30bps while capitalisation rates for logistics and Grade A office are expected to hold steady. Valuers may marginally adjust valuations downwards by incorporating a lower/more conservative rental growth assumption due to the weaker economic outlook and demand moving forward.

Hospitality:

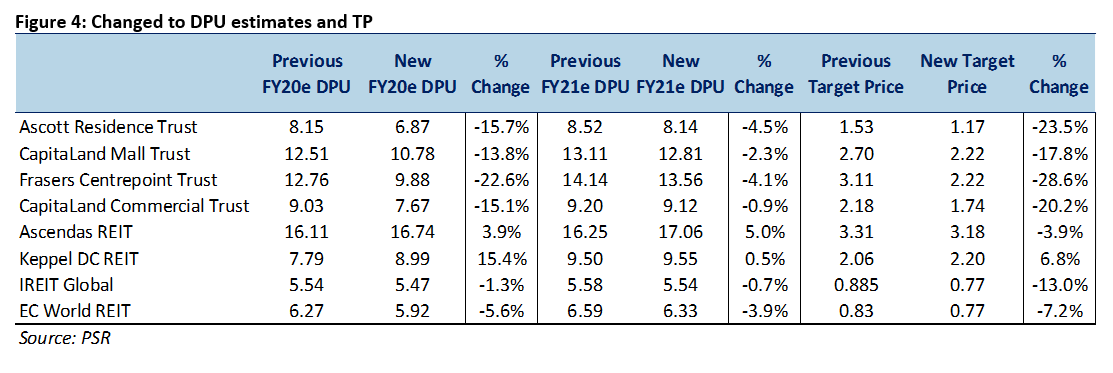

The extension of lockdowns and restrictions on international travel in many countries has resulted in occupancy levels for hotels to nosedive by approximately 30%. Alternative sources of income such a block-bookings by the government for isolation purposes lifted occupancies to the 40% – 80% range. Recovery for the hospitality sector is expected to be slow in 2020 as lingering fear and caution after international travel bans are lifted may keep visitors away. However, MICE events, which have been pushed back to the second half of the year, should help in the recovery of the sector once event-hosting restrictions are lifted. Hospitality REITs are expecting domestic demand to fill occupancies until international travel resumes. Pent-up demand for travel will lead to a strong recovery for the hospitality sector in 2021. FY20 DPU was cut by 15.7% for ART (figure 4).

Retail:

The mandated closure of non-essential trade has impacted the retail sector the most. The COVID-19 situation has highlighted the vulnerable positions retail tenants are in, with their thin margins, as well as the market’s expectation for landlords to have “more skin in the game”. During the circuit breaker, approximately 25% of mall tenants were operational. Landlords offered 2 to 3 months’ worth of rental rebate to help tenants through this period of non-trading.

In the near-term, landlords will exercise flexibility in their leasing strategy. This equates to lower fixed rent component and a higher turnover-based variable rent. In the long run, higher risk-sharing may increase the demand for retail space as the lower fixed rents makes it more economically viable for new-to-market brands to give the brick-and-mortar model a go, helping to combat the shift towards e-commerce, which is more pronounced due to the familiarisation of e-commerce platforms and convenience experienced during the lockdown. FY20 DPU was cut by 22.6% and 13.8% for FCT and CMT respectively (figure 4).

Office:

We expect a slight increase in vacancy rates for the commercial sector as tenants rationalise their space requirements during this period. It is still too early to predict how future demand for office space will look like as there are counteracting leasing strategies being rolled out. On one hand, the successful implementation of telecommuting is likely to have a long-term impact on occupier strategy and poses risks to office demand. On the other hand, we may see companies choosing to reduce over-concentration risk by adopting lower desk-density and splitting of offices, hence increasing the demand for space. Flex-space providers may receive more demand as alternative/secondary office space.

Industrial:

While the industrial sector has a greater exposure to small-medium enterprises, the relatively high percentage of operational tenants, especially in assets where telecommuting is not possible (such as the light industrial and logistics assets), provides comfort to the degree of business disruption and the number of tenants that may require rental deferments/waivers. Future trends of e-commerce prevalence and increased adoption of cloud computing will likely see an uptick in demand for logistics and data centres assets.

INVESTMENT ACTIONS

Maintain OVERWEIGHT on the S-REITs sector

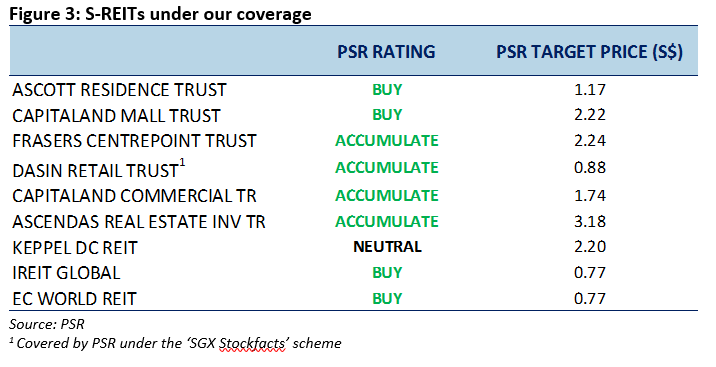

After adjusting our estimates to account for lower earnings and DPU forecasts due to the rental rebates given and the lower revenues for hospitality assets under management contract, as well as the softer demand for space in the coming years, SREITs under our coverage still present attractive upside from current prices. Figure 4 summarises the changes in our DPU estimates and TPs over the previous estimates.

Top-down view (unchanged)

We like the Commercial and Industrial sub-sectors due to tapering office supply after the surge in supply in the prior two to three years, and the AEI and redevelopment opportunities for the Industrial sector. The tenants in these two sectors are also less affected by the COVID-19 outbreak. We are cautious on the Hospitality and Retail sub-sector due softer tourism sentiment and retail outlook, exacerbated by lingering fears of another wave of COVID-19 outbreak.

Tactical bottom-up view (unchanged)

REITs that can better weather through the rising interest rate environment would be those with:

1) Low gearing; 2) High-interest coverage; 3) Long weighted average debt to maturity; and

4) A high proportion of debt on fixed interest rates; 5) Higher percentage of guaranteed revenue through “fixed” or “stable” leases.

MACROECONOMIC ENVIRONMENT

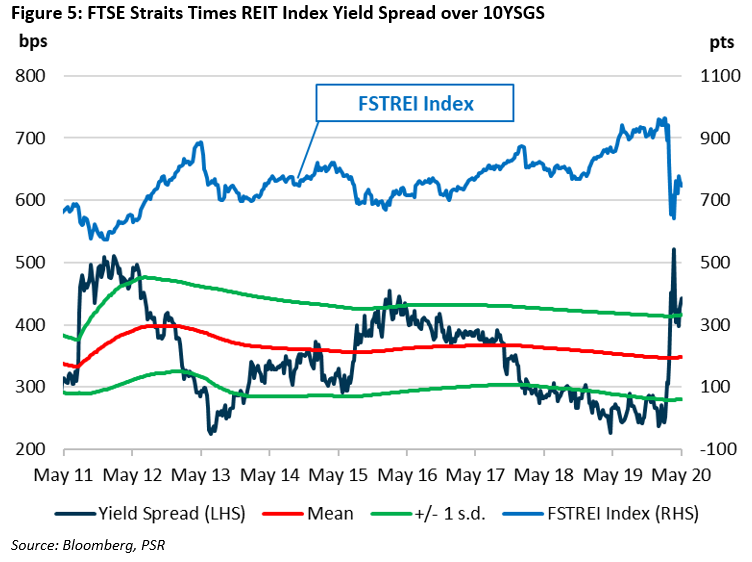

The S-REIT yield spread as at 15 May 2020 was 442bps, at the +1.4SD level. This compares to the average dividend yield spread of 260bps in 2019 which was in the -1.0 to -1.5SD range.

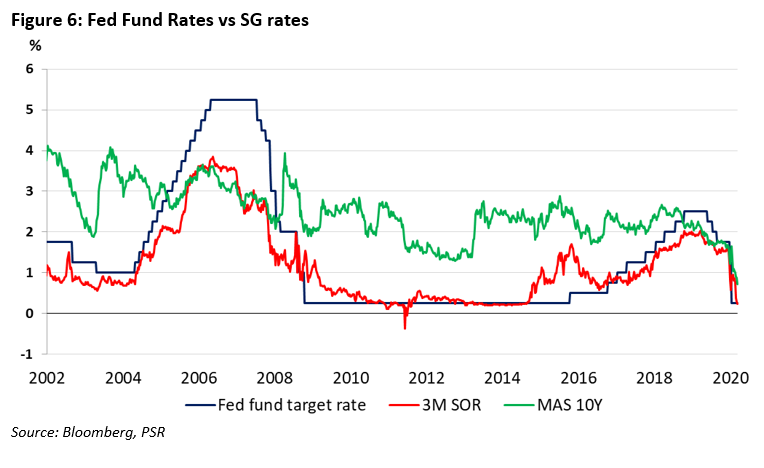

3M SOR at 0.23% is a 5-year low. Such levels of SOR were last seen in September 2014. The 10YSGS at 0.72% is also a decade-low.

OFFICE

Occupancy dipped 0.5ppts in 1Q20 to 89.0%, albeit being 0.8ppts higher YoY. The rental index which has experienced 3 consecutive quarters of decline, falling 1.3pts QoQ to 168.7pts. Office prices also showed some weakness, falling 4.0% QoQ. However, positive rental reversions are expected for the office sector which typically follows a 3-year leasing cycle (figure 7), as expiring rents are still 5% to 25% below current market rents.

We expect a slight increase in vacancy rates for the commercial sector as tenants rationalise their space requirements. While the successful implementation of telecommuting is likely to have a long-term impact on occupier strategy and poses risk to office demand, we may also see companies choosing to reduce over-concentration risk by adopt lower desk-density and split office, hence increasing the demand for space. Flex-space providers may receive more demand as well.

59% of the 872K sqft coming online in the central area in 2020 is from CapitaLand owned 79 Robinson Road, which received TOP on 5 May 2020. The CapitaLand Group announced that 79 Robinson Road has secured >70% leasing pre-committed from MNCs from various industries. The lower vacant supply should take some pressure off rents. CapitaSpring which will come online in 2021 has secured pre-commitments for 34.8% of the space.

INDUSTRIAL

Industrial rents have been bottoming out over the past 18 quarters. Industrial occupancy held steady QoQ at 98.2%. Rental index for business parks were unchanged while the multiple and single-user factory and warehouse index fell by 0.2 to 0.4pts.

New supply of industrial space coming on to the market in FY20/21 represents 4.4%/1.5% of existing supply. However, a deeper look at the oncoming supply reveals that c.70% of FY20/21 supply will be from light industrial flatted factories, of which 50%/68% of light industrial supply will be leased to single tenants (i.e.: build to suit with a committed occupancy of 100%).

RETAIL

Occupancy dipped marginally by 0.5ppts while the rental index fell by 2.3pts QoQ.

70,000sqm of supply coming onto the market in 2020 and 2021 represents a 1.2% increase in retail stock. Most of the retail supply hitting the market are part of mixed-use developments with <10,000sqft of retail space, hence indirectly competing with suburban malls in those locations.

REITS under our coverage, Frasers Centrepoint Trust (FCT) (Accumulate; TP: S$2.24) and CapitaLand Mall Trust (CMT) (Buy; TP: S$2.22) managed to achieve positive rental reversions on expiring leases in the quarter ended 31 March 2020, although the reversions for the rest of the year are expected to be weak.

HOSPITALITY

Low supply of rooms hitting the market over the next 3 years bodes positively for the SG hospitality sector. Room supply is expected to grow by 1.1%/1.0% in FY20/FY21.

The ugly collapse of IVA and RevPARs comes as no surprise as Singapore’s closed its borders from international travelers. Alternative sources of income such a block-bookings by the government for isolation purposes lifted occupancies to the 40% – 80% range. Recovery for the hospitality sector is expected to be slow in 2020. Fear and caution after international travel bans are lifted may keep visitors away, although MICE events, which have been pushed back to the second half of the year, should help in the recovery once event-hosting restrictions are lifted. Hospitality REITs are expecting domestic demand to fill occupancies until international travel resumes. Pent-up demand for travel will lead to a strong recovery for the hospitality sector in 2021.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: