SECTOR SNAPSHOT

Acquisition momentum continued, with Ascendas REIT, CapitaLand Retail China Trust, Mapletree Logistics Trust, Suntec REIT and ARA LOGOS Logistics Trust announcing acquisitions in the last one month.

Leasing remained challenging across the sectors as companies held off expansion and relocation. Renewals are expected to form the bulk of leases as businesses try to preserve capital and save on relocation.

Office:

Several banks have allowed their staff to telecommute 40-60% of the time. DBS’ 29,000-strong workforce has the option to work remotely up to 40% of the time while 65% of UOB’s 26,000-strong workforce has the option to work remotely two days a week. As financial institutions are the top three occupiers of office space, we think this move towards flexible work arrangements will set in motion more aggressive rightsizing of space in the mid-term.

REITS have reported a handful of pre-terminations, with tenants giving back 10-20% of their space. Encouragingly, part of the space vacated has been backfilled. QBE Insurance is relocating to Guoco Tower and taking up 31,000 sq ft of space vacated by Grab, which is moving to one-north. Amazon will lease 90,000 sq ft across three floors at Asia Square Tower 1 given up by Citigroup.

Industrial:

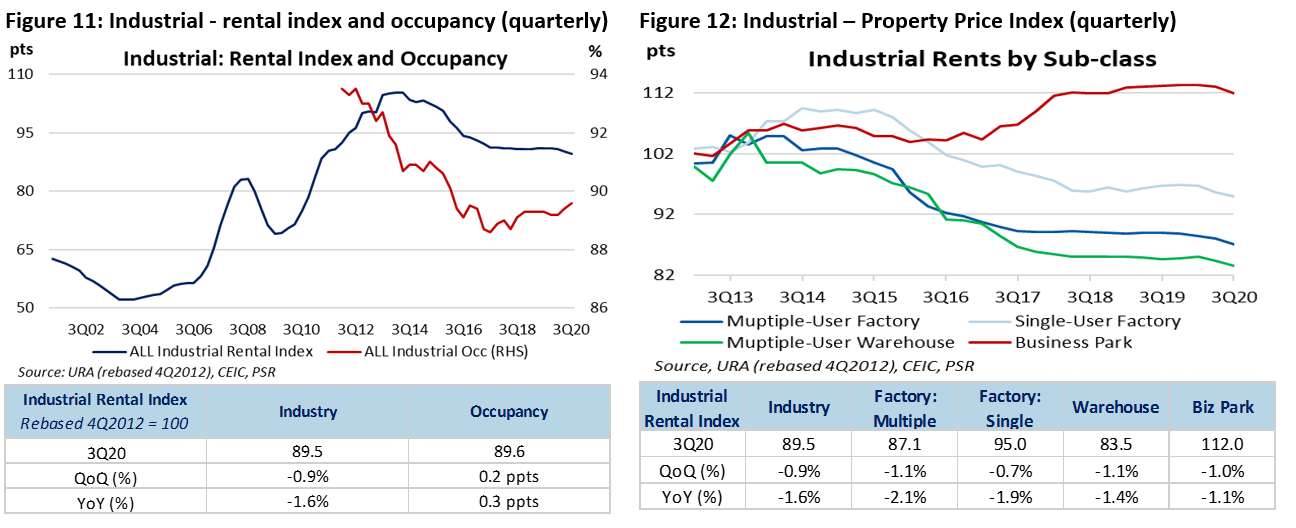

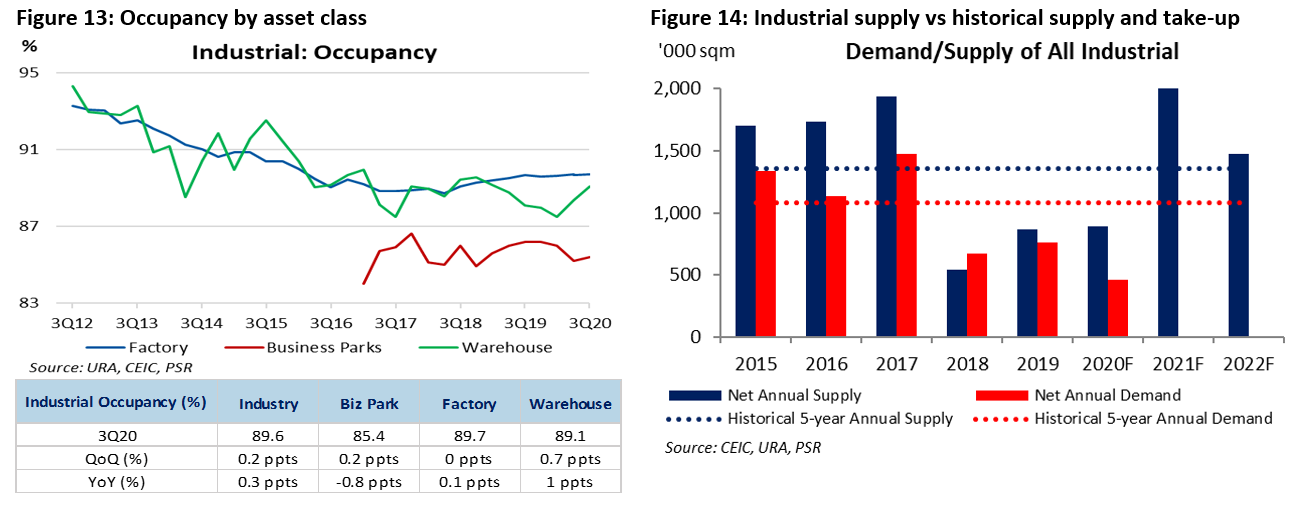

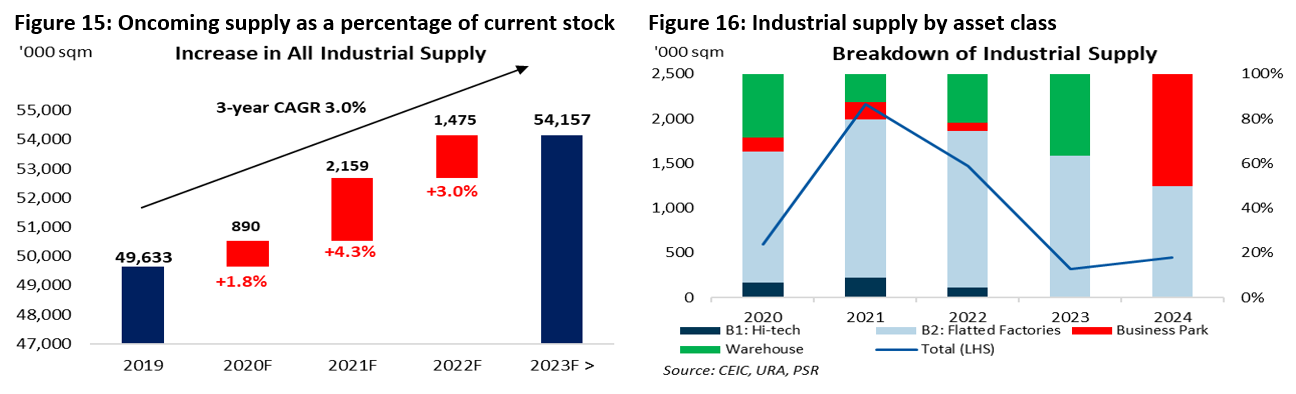

Industrial rents dipped 0.7-1.1% QoQ across the asset classes while occupancy inched up 0.2ppt, lifted by factories (+0.2ppt) and business parks (+0.7ppt).

Mixed outlook. Logistics assets have benefited from expansion by e-commerce and third-party logistics players while demand for business parks has come from firms relocating to business parks with similar specifications as Grade A offices to save costs. A continued moratorium on data centres is expected to lead to higher rents in the coming years. Leasing of factory space may not fare as well as the global demand recovery is nascent while demand for hi-tech space remains supported by growth in electronics demand.

Retail:

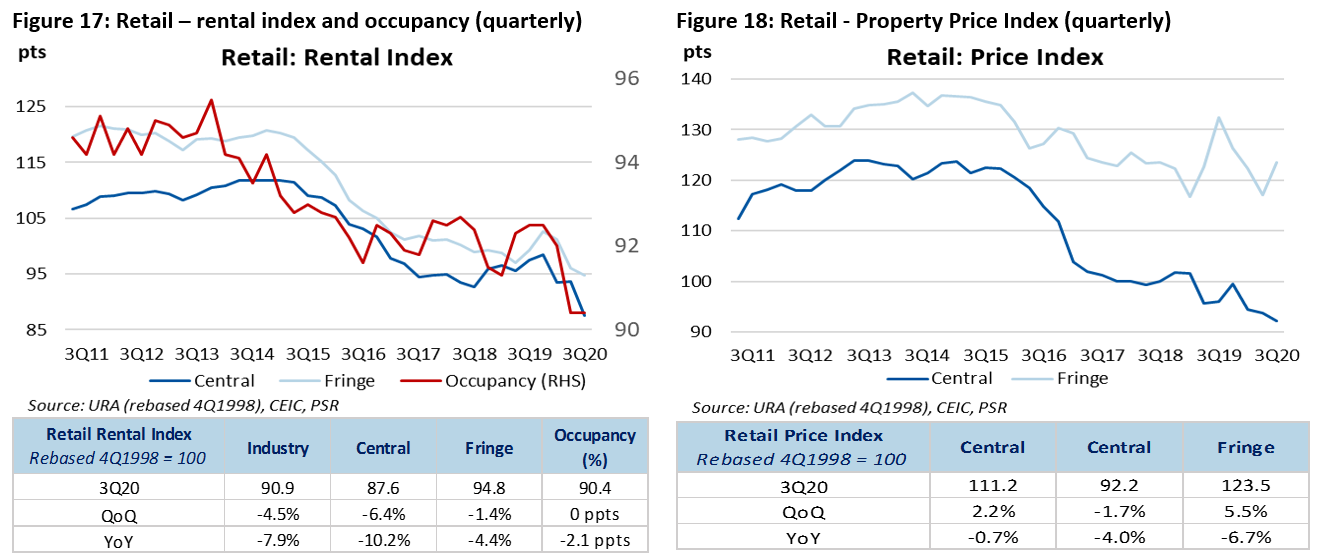

Retail occupancy was steady QoQ at 90.4%, although rent weakness was detectable. Central rents tumbled by 6.4% QoQ and 10.2% YoY while fringe rents dipped 1.4% QoQ and 4.4% YoY. This is likely to continue as retail landlords prioritise occupancy over rents and exercise flexibility in lease negotiations.

The pandemic was the final nail in the coffin for ailing concepts such as department stores. In October, Robinsons announced the closure of its Singapore stores for good. It followed Top Shop’s decision to pull out of Singapore in September. News of multinational fast-fashion chains such as H&M, Gap and Forever 21 slashing their global store counts is worrying and will likely impinge on demand for retail space.

Hospitality:

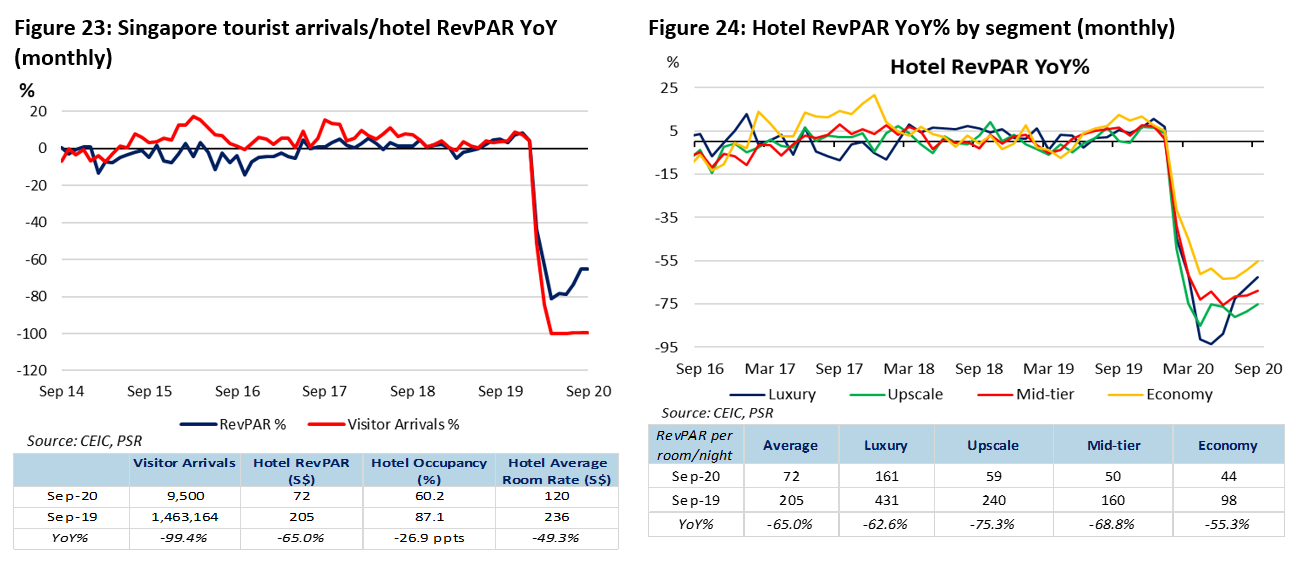

RevPARs have been climbing since hoteliers were able to accept staycation bookings in July. Industry occupancy remained above 60% in 3Q20, recovering from its low of 40% in March and April. Hotels that are expected to draw staycation demand are luxury/upscale or resort-styled accommodations. With bans on leisure travel likely to remain in place towards the festive season, hoteliers are anticipating a spike in staycation demand. They have raised room rates by S$100-200.

Meanwhile, hospitality players have achieved leaner cost and operating structures through the adoption of digital technology. They have lowered manpower costs by enabling self-check-in using mobile devises and turning to service robots and mobile applications for reservation systems.

INVESTMENT ACTIONS

Maintain OVERWEIGHT on sector

Broadening economic recovery

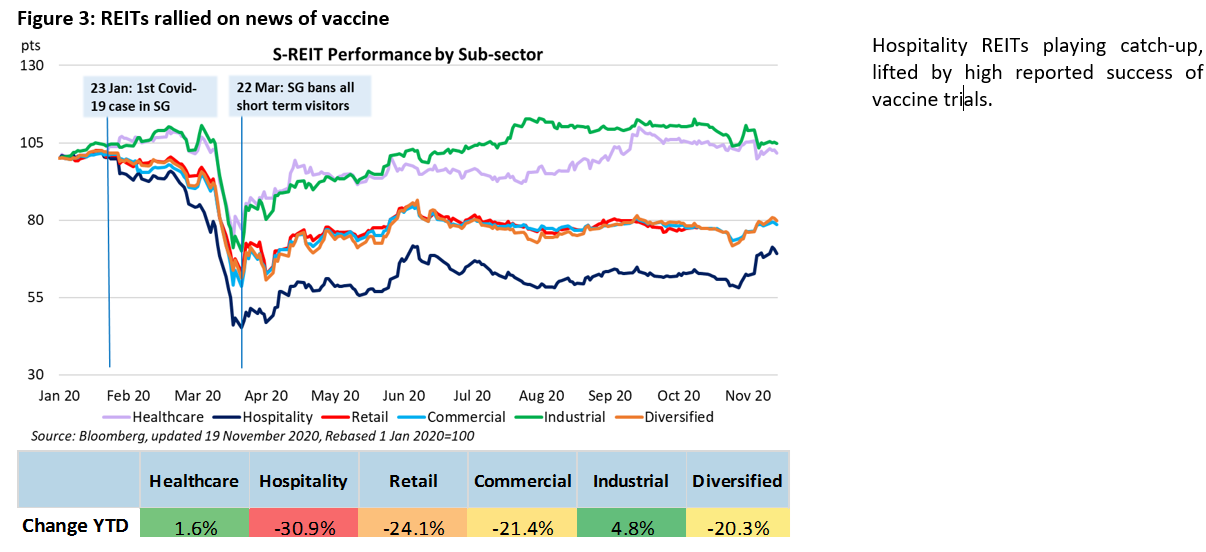

Since June, economic indicators have been improving. These include manufacturing output, NODX and retail sales. SREITs share that most of their tenants remain current with their rents, although a handful are still in need of rental assistance. News of high success rates of the Pfizer and Moderna vaccines has lifted sentiment, potentially benefitting hospitality REITs the most.

Sub-sector preferences: hospitality, office and industrial

almost a year of living under travel and mobility restrictions, demand for travel is expected to pent up. With many countries rushing to secure more than one vaccine, high participation in the COVAX* programme and months of calibrating the manufacturing and distribution of vaccines, we think this last leg of the vaccine timeline will be swifter. As we believe it pays to be early in our call, we have upgraded the hospitality sub-sector to overweight.

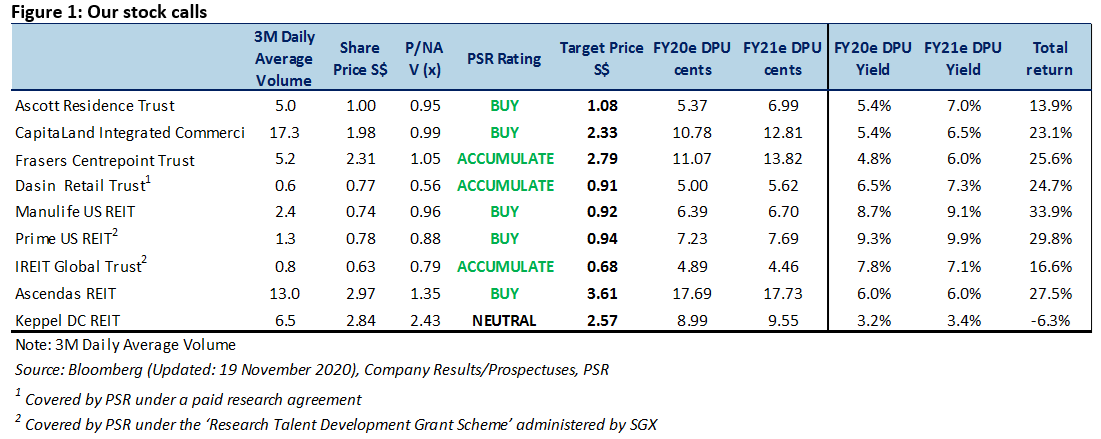

We like US office REITs for their long WALEs and downside protection from remote-working adoption. Our stock picks are Manulife US REIT (MUST SP, Buy, TP: US$0.92) and Prime US REIT (PRIME SP, Buy, TP: US$0.94).

Our pick for retail exposure is Frasers Centrepoint Trust (FCT SP, BUY, TP: S$2.79). Tenant sales at its suburban malls have recovered to pre-COVID levels. We believe that suburban malls will remain an important infrastructure, catering to necessity spending.

MACROECONOMIC ENVIRONMENT

OFFICE

As more workers return to the office, companies are able to evaluate their space needs. Several banks have announced flexible working arrangements, allowing their workforce to telecommute 40-60% of the time. DBS’ 29,000-strong workforce has the option to work remotely up to 40% of the time. About 65% of UOB’s 26,000-strong workforce has the option to work remotely two days a week. Financial institutions are the top three occupiers of office space and we think their move towards flexible work arrangements will set in motion more aggressive rightsizing of space in the mid-term.

REITS have reported a handful of pre-terminations, with tenants giving back 10-20% of their space. Encouragingly, part of the space vacated has been backfilled. QBE Insurance is relocating to Guoco Tower and taking up 31,000 sq ft of space vacated by Grab, which is moving to one-north. Amazon will lease 90,000 sq ft across three floors at Asia Square Tower 1 given up by Citigroup.

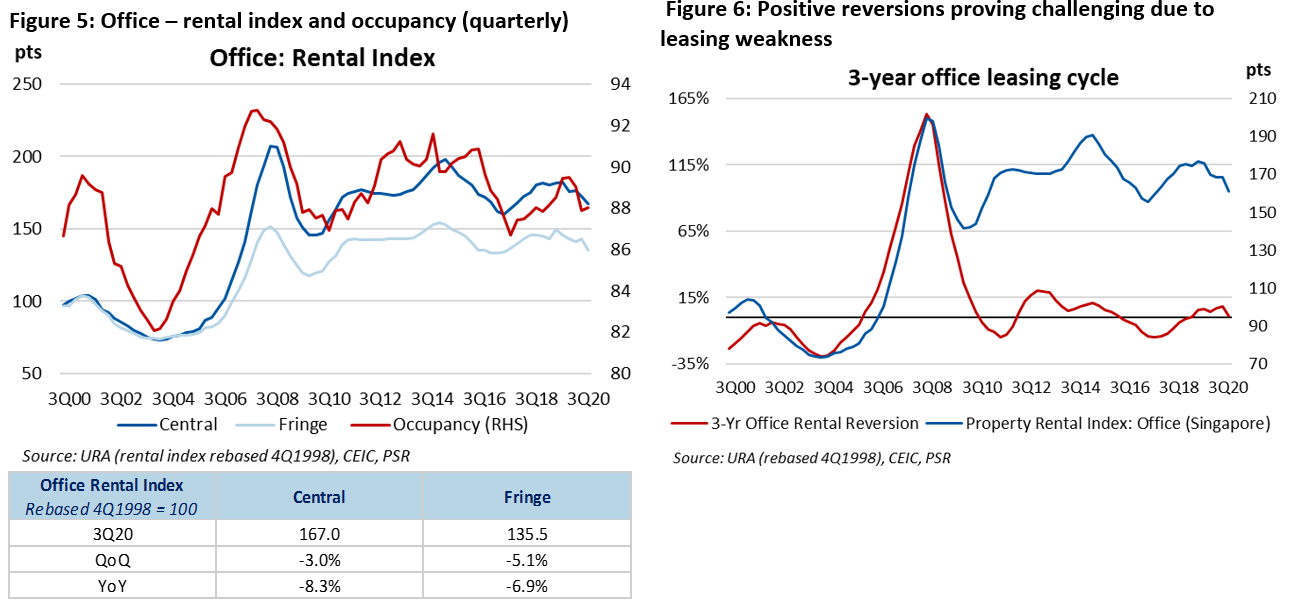

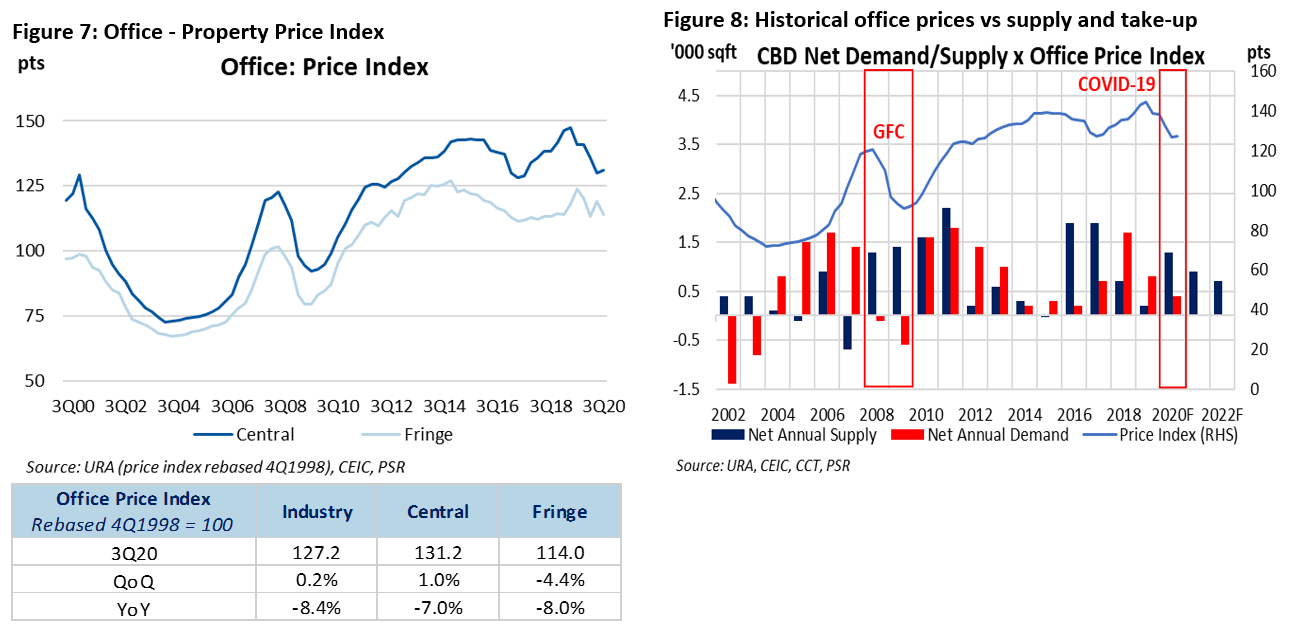

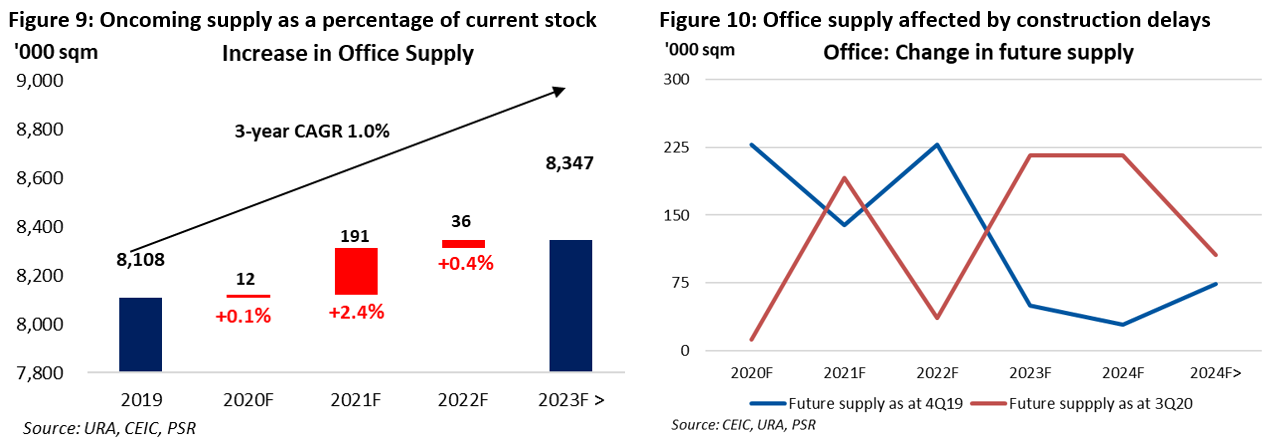

Construction slippages (Figure 10), as well as muted supply in the market, are expected to provide near-term support for the office sector. Supply in the core CBD is at its 5-year historical average of 0.9mn sq ft in comparison to 1.2mn sq ft during the GFC (Figure 8). So far, two CBD commercial owners are revaluating redevelopments to unlock additional GFA from the CDB and Strategic Development Incentive Schemes. About 700,000 sq ft from AXA Tower (50:50 JV between Perennial and Alibaba) and CDL’s 353,575 sq ft Fuji Xerox Tower and 131K sq ft Central Mall will potentially be displaced in 2021/22, if plans for redevelopment proceed.

INDUSTRIAL

Industrial rents dipped 0.7-1.1% QoQ across the asset classes while occupancy inched up 0.2ppt, lifted by factories (+0.2ppt) and business parks (+0.7ppt).

Mixed outlook. Logistics assets have benefited from expansion by e-commerce and third-party logistics players while demand for business parks has come from firms relocating to business parks with similar specs as Grade A offices to save costs. The moratorium on data centres remains firmly in place. This is expected to lead to higher rents in the coming years. Leasing of factory space may still be muted as global demand is only starting to recover. Demand for hi-tech space remains supported by growth in electronics demand.

RETAIL

Retail occupancy was steady QoQ at 90.4% although rents showed weakness. Central rents tumbled by 6.4% QoQ and 10.2% YoY while fringe rents dipped 1.4% QoQ and 4.4% YoY. This is expected to continue as retail landlords prioritise occupancy over rents and exercise flexibility in lease negotiations. Landlords have offered shorter leases of six months to tenants who are still struggling. They are also offering 3-year leases with lower base rents and higher turnover rents in the first year, with the base rents escalating over the years. Such leases are expected to lower occupancy costs for tenants in the short term as the economy recovers.

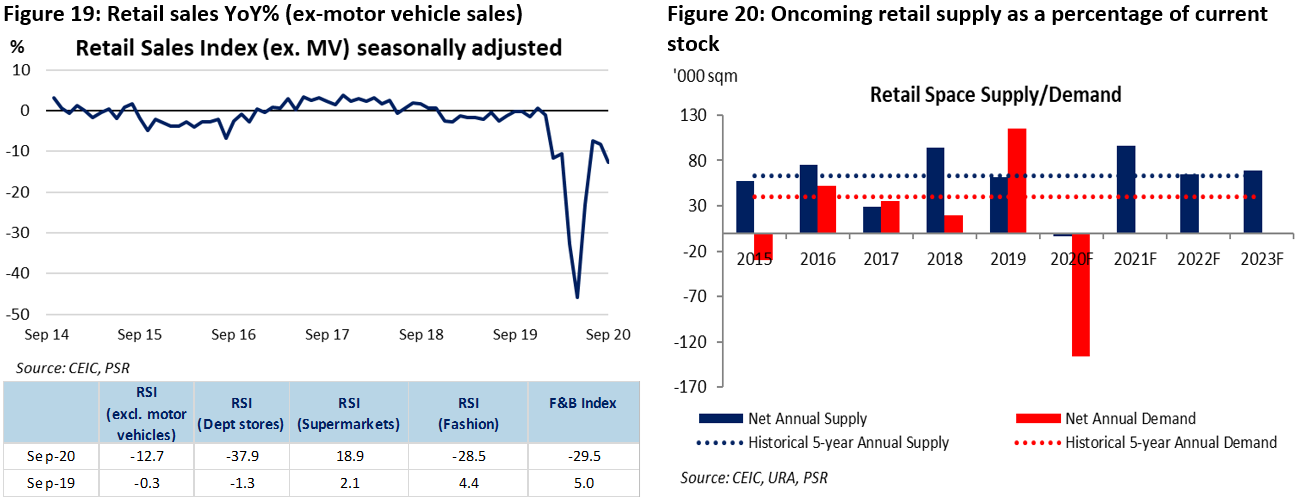

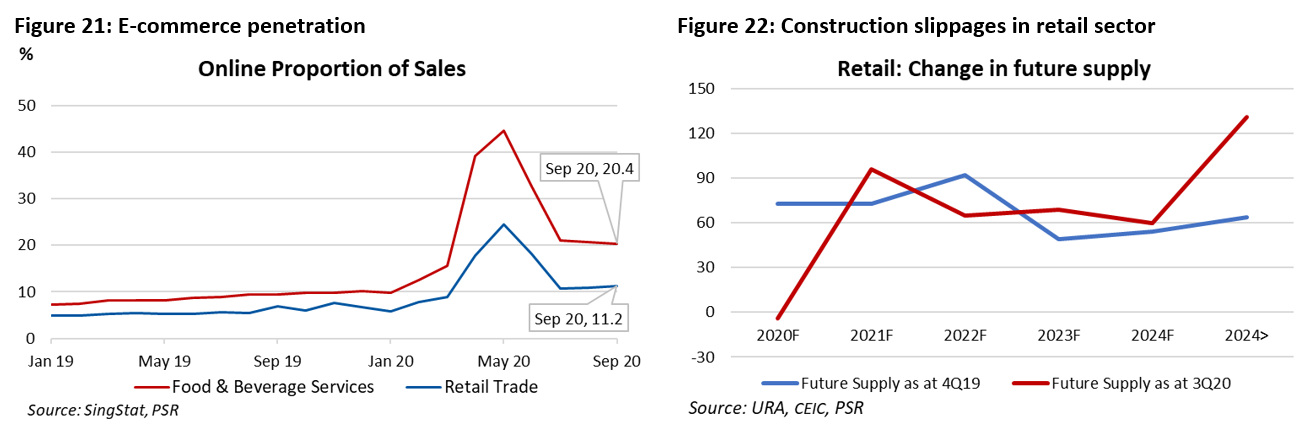

The retail sales index (ex-motor vehicles) dipped 4.4ppts MoM from -8.3% to -12.7% in September. Online retail sales made up 11% of the sales. Supermarkets (+18.9%), Furniture & Household Equipment (+11.0%) and Recreational Goods (+6.1%) continued to grow YoY while other fashion-related discretionary trades contracted 15.9-37.9%.

The pandemic was the final nail in the coffin for ailing concepts such as department stores. In October, Robinsons announced its total exit from Singapore for good. It followed Top Shop’s decision to pull out of Singapore in September. In light of the weaker leasing demand, REITs are evaluating their asset-enhancement initiatives and repositioning of their malls.

Singapore may enter Phase 3 of reopening before the end of the year. Phase 3 will entail a further relaxation of control measures. The cap on group gatherings may be increased from five to eight people. Restrictions on nightlife hotspots, which are deemed higher-risk, such as bars, karaoke lounges and nightclubs are likely to remain. Retail landlords will likely provide some rental support for tenants which continue to operate under restrictions.

HOSPITALITY

RevPARs have been climbing since hoteliers started to accept staycation bookings in July. Industry occupancy remained above 60% in 3Q20, recovering from its low of 40% in March and April. Hotels that are expected to draw staycation demand are luxury/upscale or resort-styled accommodations. With bans on leisure travel likely to remain in place as we enter the festive season, hoteliers are anticipating a spike in staycation demand. They have raised room rates by S$100-200.

China’s domestic air travel has recovered to pre-pandemic levels although international travel remains curtailed. Given that China is ahead in the COVID-19 timeline, we look at its recovery as a gauge for the other countries. Countries with sizeable domestic travel markets such as France, Japan, the US, Spain, India and Brazil could potentially see a similar recovery in domestic travel. Several vaccines have achieved success rates of over 90%. But for travel confidence to return, the vaccines must be available to all.

Meanwhile, cost initiatives by hoteliers have borne fruit. Cost and operating structures have become leaner through the adoption of digital technology. Hotels have lowered their manpower costs by enabling self-check-in using mobile devises and deploying service robots and mobile applications for reservations.

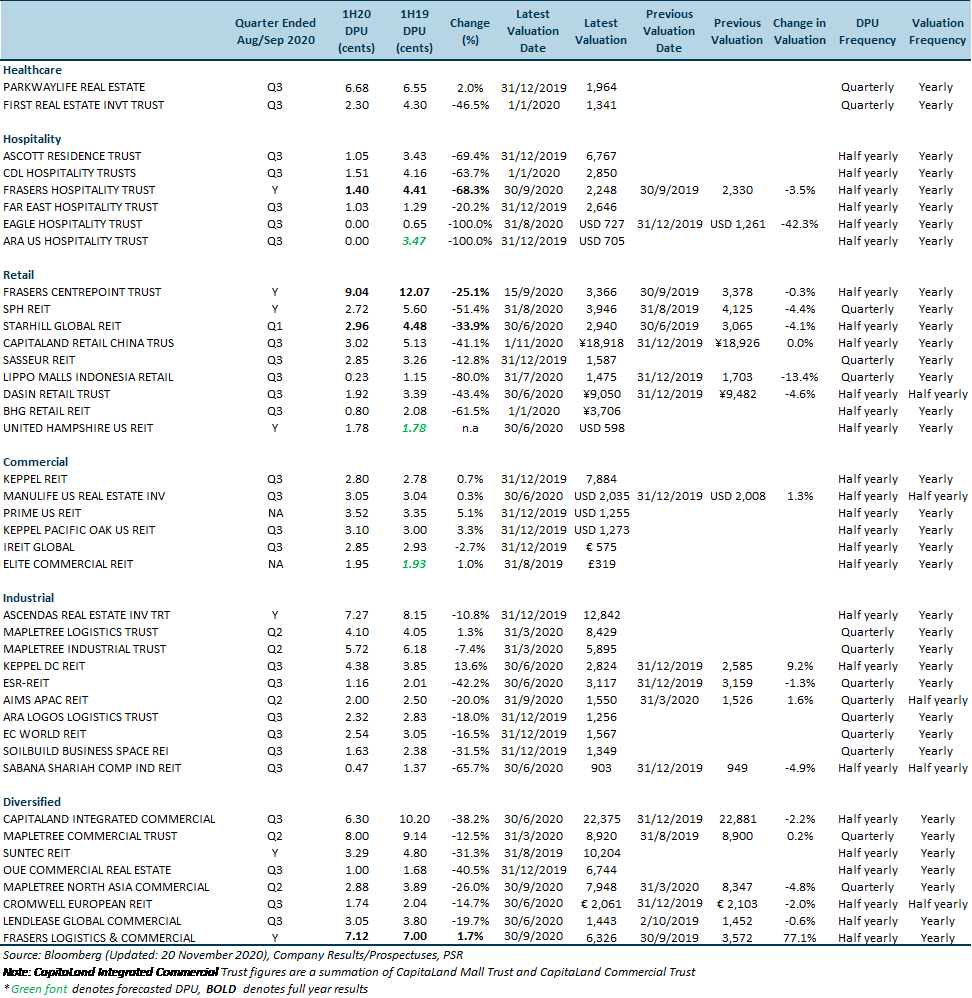

Figure 25: COVID-19’s impact on DPUs and asset valuations

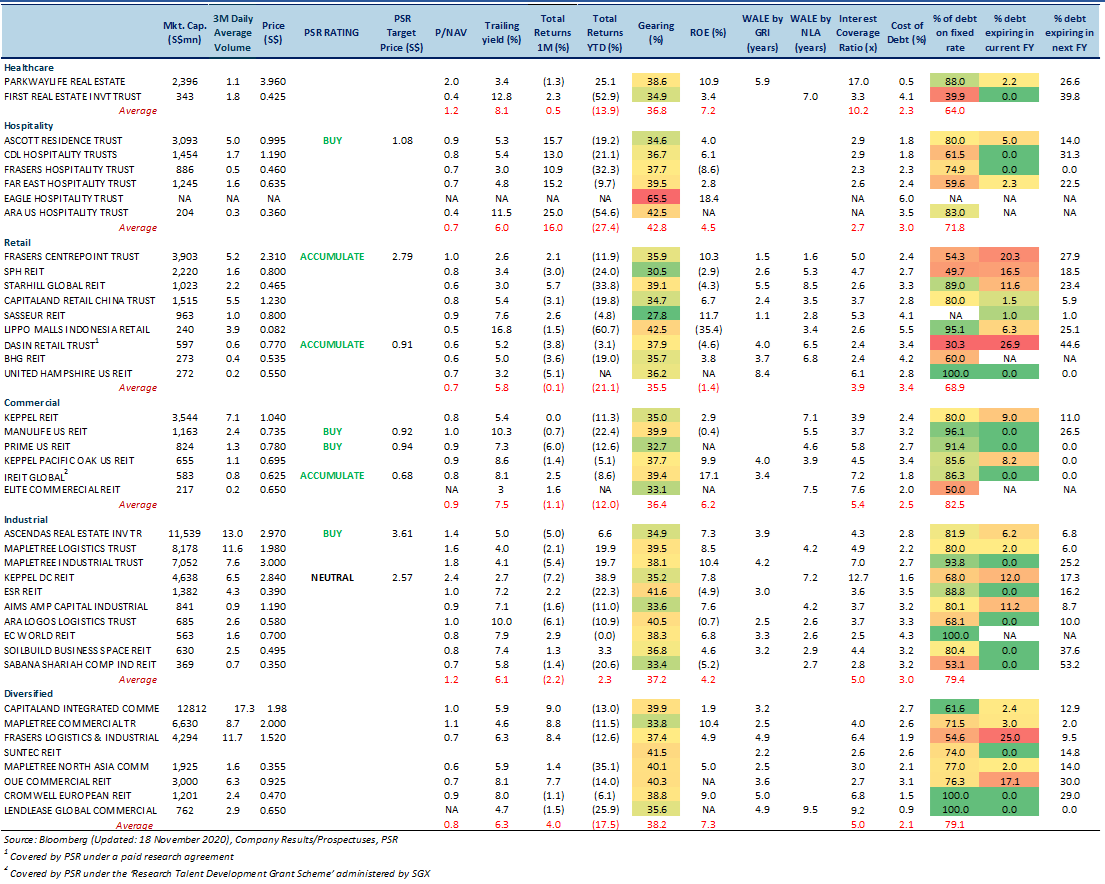

Figure 26: S-REIT Universe

*Note: Coloured columns indicate the critical attributes of REITs that should be looked at from a capital management perspective. Our colour coding represents the scale of the figure for each column, green representing better than average and red representing worse than average.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: