SECTOR SNAPSHOT

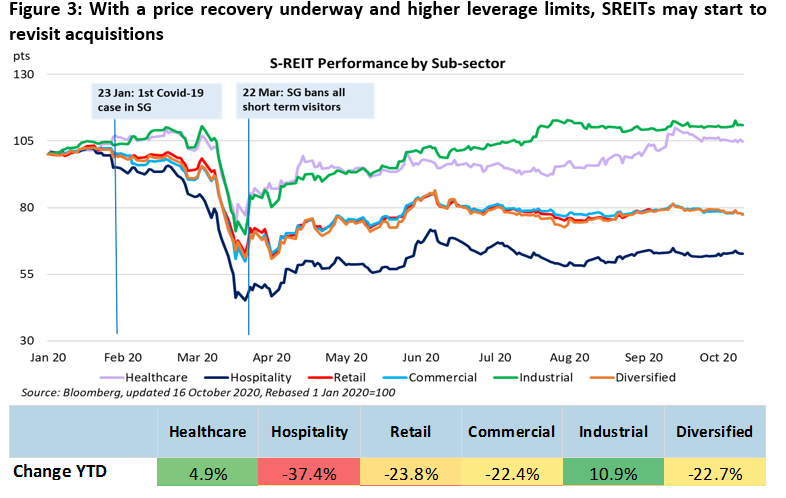

SREITs had a turbulent first half, with many slashing their DPUs to conserve cash amid economic uncertainties (Figure 8). With a broad economic recovery underway, they are likely to pay out retained distributions in 2H20, in our view. Some recently revalued their assets, capturing the COVID-19 impact on their portfolios (Figure 8). Most valuations did not fall by more than 5%, except for Lippo Malls Indonesia Retail Trust (LMRT SP, Not Rated) (-13.4%). There were some revaluation gains for Industrial REITs such as Keppel DC REIT (KDC SP, Neutral, TP: S$2.57) and Aims Apac REIT (AAREIT, Not Rated), of 9.2% and 2.5% respectively.

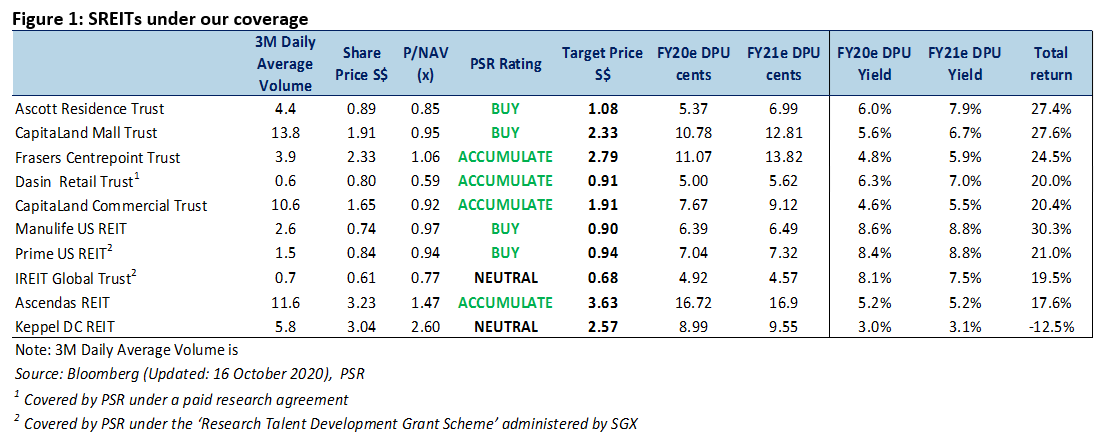

The merger between CapitaLand Mall Trust (CT SP, BUY, TP: S$2.33) and CapitaLand Commercial Trust (CCT SP, Accumulate, TP: S$1.91) is ongoing. Expected date of CCT’s delisting is 30 October 2020. Keppel DC REIT (KDC SP, Neutral, TP: S$2.57) is currently at the top of the FTSTI reserve list and could be added to the index at the next quarterly review in December. Index inclusions typically elevate the profile and trading volume of the constituent stocks and an inclusion could potentially result in a re-rating for KDC. Of the remaining four stocks on the reserve list, three are REITs: Frasers Logistics & Commercial Trust (FLCT SP, Not Rated), Suntec REIT (SUN SP, Not Rated) and Keppel REIT (KREIT SP, Not Rated).

Office:

Despite some attrition in demand from downsizing and remote working, demand for space continues to stem from:

A “flight to quality” usually occurs in times of economic uncertainty, as tenants take the opportunity to lease prime space at more attractive rates. Leasing picked up in 3Q20, although CBD rents have dipped. Encouragingly, part of the space vacated from relocations and downsizing has been backfilled. QBE Insurance is relocating to Guoco Tower and taking up 31,000 sq ft of space vacated by Grab, which is moving to one-north. Amazon will lease 90,000 sq ft across three floors at Asia Square Tower 1 given up by Citigroup.

Supply conditions are supportive, with an average 0.9mn sq ft expected per year. This is below the 10-year average of 1 mn sq ft. And it is before accounting for the redevelopment of AXA Towers, Fuji Xerox and Central Mall in 2020/2021, which will take off almost 1.2mn sq ft of supply. We expect this to provide further support for rents.

We reiterate that office workspace should remain relevant due to the value-add from collaboration, mentorship and corporate culture, which are best effected through physical interactions.

Retail

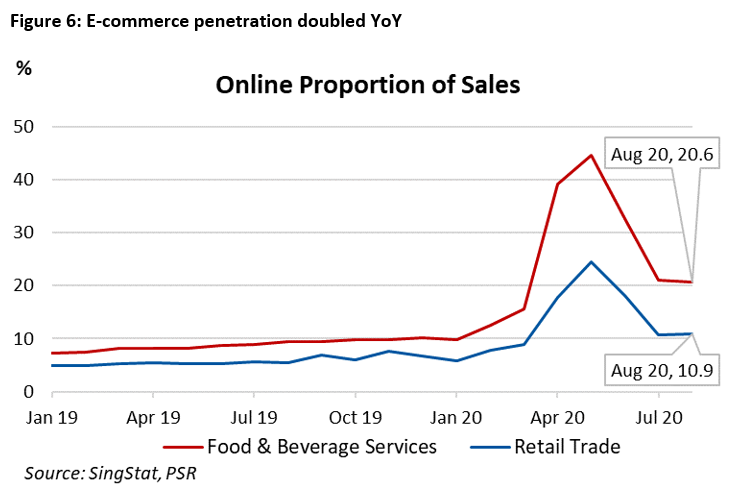

Retail e-commerce penetration settled at 11.0% in Phase 2 of the economic reopening in July and August. This was almost double the average of 5.8% in 2019. The trend was seen across the three disclosed subsectors: Supermarkets (11.7%), Computers & Telecommunication Equipment (46.7%) and Furniture & Household Equipment (23.5%).

Still, we remain convinced that having physical stores or an omnichannel presence will be a crucial differentiating factor in ensuring longevity in the retail business. We believe that e-commerce is best suited for price comparisons, non-urgent, discretionary and “good-to-have” purchases.

While it is easy to list anything online via platforms like Lazada, Amazon and Shopee, in the long run, as e-commerce competition stiffens, we think that omnichannel marketing will give retailers an edge over the pure e-commerce players. Brick-and-mortar stores allow for better branding through:

We believe these factors will help drive brand loyalty and business sustainability – regardless of whether the transactions are concluded in-store or online. This should ultimately confirm the relevance of retail malls.

We think the recovery in sales could return confidence to tenants. Capacity constraints in malls, particularly in dine-in establishments, are partially alleviated by more balanced customer flows throughout the day.

Tenants are also likely to benefit from the scale of e-commerce and membership initiatives launched by landlords. These are likely to spur sales and customer stickiness, allowing retailers to compete with e-commerce merchants. We think mall operators like CMT and FCT will have greater success with their initiatives given their higher number of malls and the 1mn and 800k members on their membership programmes.

Hospitality

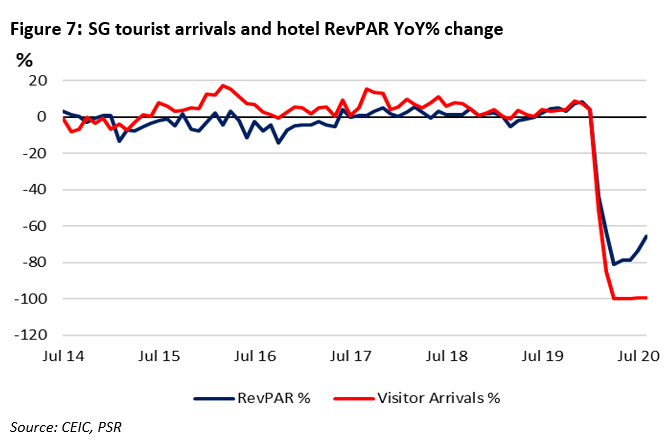

Hospitality remains under the weather as containment measures are being eased at a snail’s pace. Indonesia is the newest and ninth country with whom Singapore has established special travel arrangements. It joins Brunei, China, Malaysia, New Zealand, Korea, Japan, Australia and Vietnam.

From 3 October, the number of unique attendees at wedding receptions has been doubled from 50 to 100. Guests must be split up into physical zones of up to 50 people each. The larger group size would allow more wedding receptions to take place and hoteliers to recognise event-related revenue and clear their backlog of wedding bookings.

Recovery in the sub-sector is expected to be slow in 2020/2021, hinging on the vaccine timeline. We expect business travel to remain muted. Transaction-driven or top-management meetings will likely be among the first to resume. Staycation demand could help fill occupancies in the near term, with the S$300mn SingapoRediscovers vouchers expected to stimulate staycation take-up.

Industrial

Of the asset classes, warehouses and data centres are the brightest spots. Occupancy growth to the 90% region and better rents in the warehouse segment have lifted the industrial sector. We understand from the REITs that there has been tenant expansion as well as new demand from e-commerce and third-party logistics players. With increased e-commerce penetration, we expect demand for warehouse space to heighten further.

Leasing at business parks and high-spec industrial parks remains subdued, consisting mainly of renewals. However, low supply coupled with construction delays due to COVID-19 should provide some near-term support for rents.

Containment measures due to COVID-19 has forced businesses to rely on the internet, software and programmes to work interact with colleagues remotely. Business have accelerated digitalisation efforts and marketing to reaching out to customers. This has resulted in an increased need for data storage and hence, data centres. Competition for this future ready, critical and stable asset class has pushed asset values up, as seen in KDC’s 9.2% increase in portfolio valuation post-COVID.

Much of the future supply for the industrial segment is expected to come in the form of light industrial assets, traditionally leased by manufacturers. Economic data turned more positive in 3Q20. Manufacturing output grew 2.0% YoY, a reversal from its 0.8% contraction in the previous quarter. There was expansion in the electronics and precision engineering clusters, which benefited from global demand for semiconductors and semiconductor manufacturing equipment. With persisting trade tensions between the US and China, many companies are exploring a China+1 strategy. Singapore, with its neutrality, free trade agreements with 22 countries and skilled labour, is generally considered a strong contender as an alternative manufacturing location.

INVESTMENT RECOMMENDATIONS

Maintain OVERWEIGHT on S-REITs

Broadening economic recovery

Since June, economic indicators have been improving, including manufacturing output, NODX and retail sales. SREITs share that the majority of their tenants remain current with their rents, abating concerns that they may have to provide additional rental support. We think the worst could be over except for Hospitality, barring a second pandemic wave.

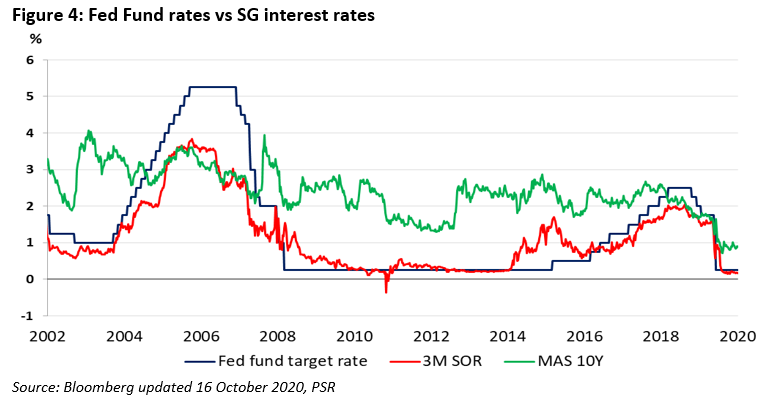

Interest rates supportive of M&A growth

REITs have resumed their quest for acquisitions. The establishment of travel channels with more countries will allow the resumption of more overseas negotiations. With interest rates expected to remain low, share prices recovering and confidence returning to capital markets, there could be more M&A opportunities for the REITs.

Sub-sector preferences: Commercial and Industrial

We prefer the Commercial and Industrial sub-sectors due to tapering office supply, AEI and redevelopment opportunities. These two remain relevant and stable despite the pandemic.

We like the US Office REITs due to their long WALEs and downside protection from remote-working adoption. Our stock picks are Manulife US REIT (MUST SP, Buy, TP: US$0.90) and Prime US REIT (PRIME SP, Buy, TP: US$0.94).

Retail does look more optimistic, as suggested by the V-shaped recovery in the RSI. However, we would hold off upgrading this segment pending signs of sustained leasing demand to compensate for their shorter WALEs. Our pick for exposure is Frasers Centrepoint Trust (FCT SP, Accumulate, TP: $2.79). Tenant sales at its suburban malls have recovered to pre-COVID levels while central malls struggle to catch up with a lack of tourist spending.

We remain cautious on Hospitality due to continued restrictions on international travel. Our call for this segment is Ascott Residence Trust (ART SP, BUY, TP: S$1.08), on the back of ART’s strong balance sheet and ability to weather near-term headwinds facing the hospitality sector.

MACROECONOMIC ENVIRONMENT

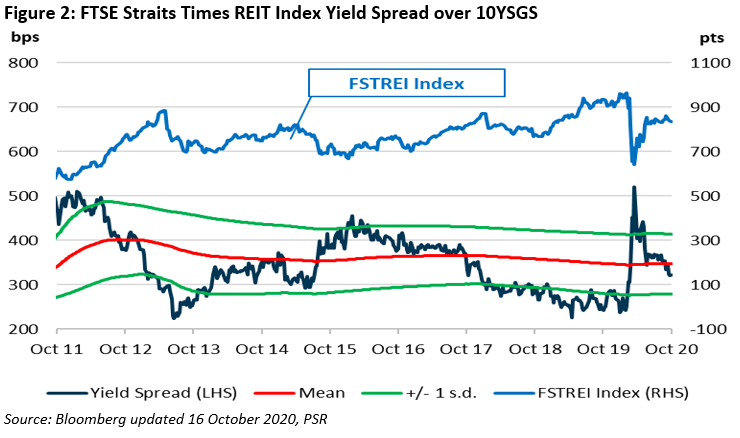

FTSE S-REIT index has been trading sideways for the past five months.

Dividend yield dipped from 4.23% to 4.11% due to lower DPUs reported in the last 12 months. As a result, dividend yield spread fell from 3.35% to 3.22%, which is -0.36 SD.

SUBSECTOR MONTHLY INDICATORS

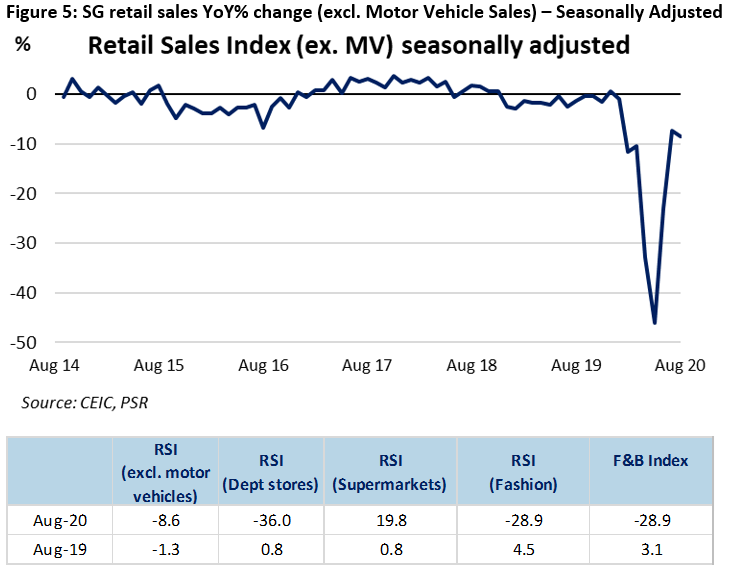

The RSI (ex-motor vehicles) dipped 1.4ppts to -8.6% YoY

Trade categories that posted growth included Supermarkets (+19.8%), Furniture & Household (+18.6%), Computer & Telecomm. Equipment (+16.1%).

Discretionary trade sales remained depressed, down c.30% YoY in August.

Despite marked improvements in F&B services since Phase 2, the F&B Services Index was down 28.9%.

E-commerce penetration settled at around 11% for retail trade during Phase 2. This was double its 2019 average of 5.8%. We expect such penetration rates to be the new normal.

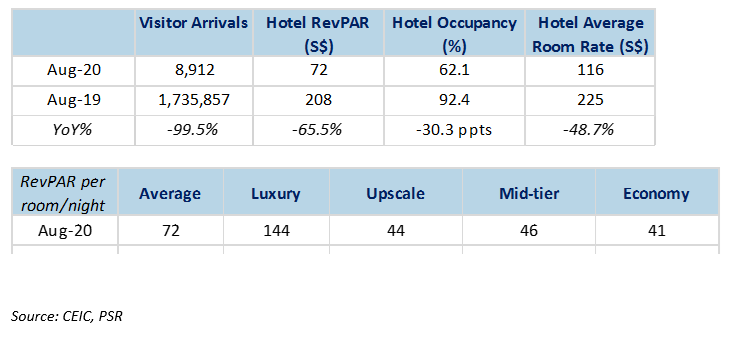

Average RevPAR climbed 33.8% MoM, led by a 26.5% increase in the luxury segment. Room rates were likely bumped up by staycation demand.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: