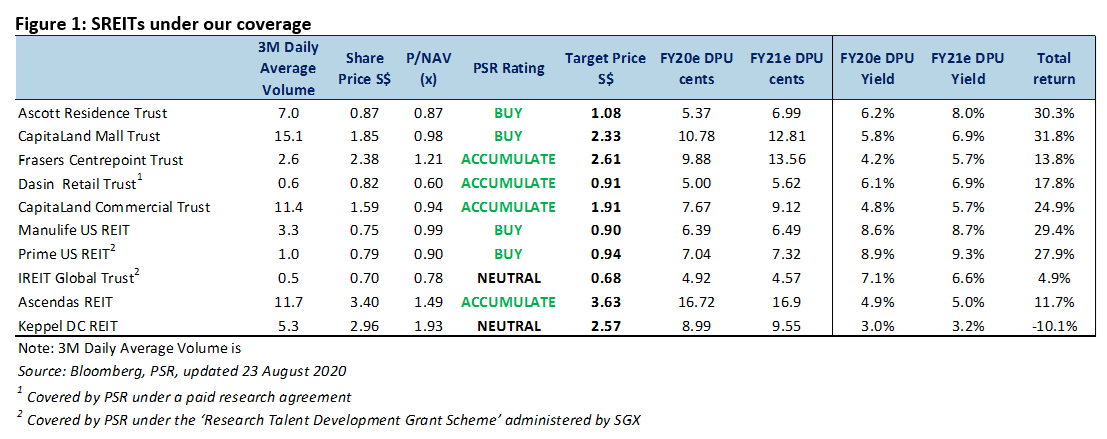

SECTOR SNAPSHOT

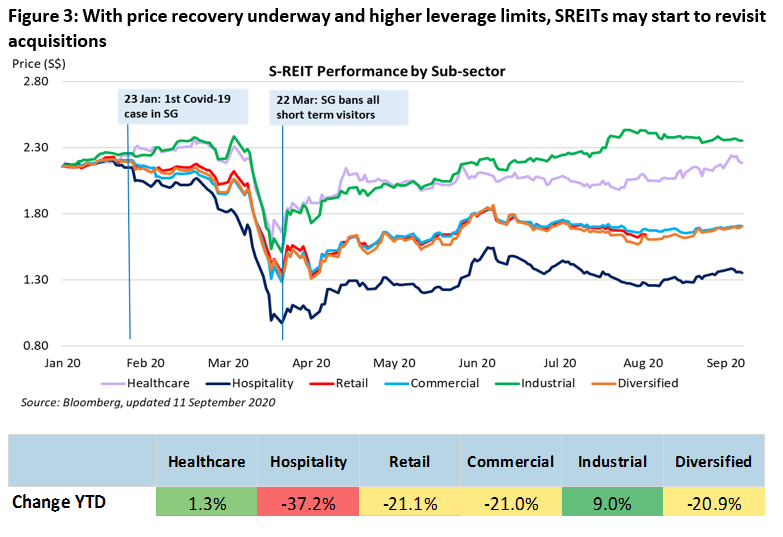

Acquisition momentum for REITs continued, spurred by low interest rates and the recovery in share prices. On September 3, Frasers Centrepoint Trust (FCT) announced the $1,057mn acquisition for the remaining 63.1% stake in AsiaRetail Fund Limited, gaining full control of 5 suburban malls and 1 office asset located in Singapore. On 13 September 2020, Keppel REIT announced the acquisition of Pinnacle Office Park on New South Wales, Australia for S$303mn.

Office:

We reiterate our view that offices will remain relevant due to the value-added by mentorship, collaboration, corporate culture and creativity, which are best effected through physical interaction. We expect some attrition in office demand from downsizing or experimenting with remoting working, however the maintenance of an office address will remain the dominant trend.

Retail

In suburban malls, tenant sales have recovered to normalised levels despite shopper footfall being c.40% below normalised levels due to capacity control measures, implying that shoppers are becoming more efficient with their trips to the malls and higher conversion rates. Meanwhile, shopper traffic at central malls has also recovered to c.-40% pre-COVID levels owing to the single-digit local infection cases throughout Phase 2 and gradual return-to-office.

We think that the recovery in tenant sales would return confidence to tenants, and right concern of the sustainability of traditional retail. Capacity constraint in malls and particularly in dine-in establishments are partially alleviated by more balanced customer-flow throughout the day. Tenants will benefit from the scale of e-commerce and membership initiatives by landlords, which will help to drive sales and customer stickiness, allowing retailers to compete with merchants selling on e-commerce platforms. We think retail operators like CMT and FCT will have greater success with their e-commerce/omni-channel strategy given the higher number of malls in their portfolios and the 1mn and 800k members on their membership programs.

Hospitality

As of 11 September 2020, Singapore has established Green Lane arrangements with 6 countries (Brunei, China, Malaysia, New Zealand, Korea and Japan). As international travel restrictions are progressively lifted, the need for dedicated isolation facilities for arriving and returning travelers will continue to provide marginal block-booking demand.

Recovery for the hospitality sector is expected to be slow in 2020, hinging on the vaccine timeline. We expect business travels to remain muted, spurred by reason for travel. Transaction-driven or top-management meetings will likely be among the first to resume. Staycation demand to help fill occupancies in the near-term.

INVESTMENT ACTIONS

Maintain OVERWEIGHT on the S-REITs sector

We continue to view REITs as a stable yield investment. We believe that SREITs may emerge stronger will more future-ready portfolios, resulting in a re-rating of the SREITs sector due to:

Top-down view (unchanged)

We continue to prefer the Commercial and Industrial sub-sectors due to tapering office supply, and AEI and redevelopment opportunities. These two sectors remain more resilient, relevant and stable despite the pandemic.

The outlook for the Retail sector does look more optimistic as indicated by the V-shaped recovery in the RSI. However, we hold off on upgrading our sector view as we would like to see sustained leasing demand to compensate for the shorter WALEs of the sector.

We remain cautious on the Hospitality sector due to the continued restrictions on international travel.

Tactical bottom-up view (unchanged)

We continue to favour REITs with stability, diversification as well as near-term growth catalyst. REITs that can better weather through the weaker leasing environment and structural shifts are those with:

1) Well-distributed lease expiries 2) High-interest coverage; 3) Long weighted average debt to maturity; and 4) percentage of guaranteed revenue through “fixed” or “stable” leases.

MACROECONOMIC ENVIRONMENT

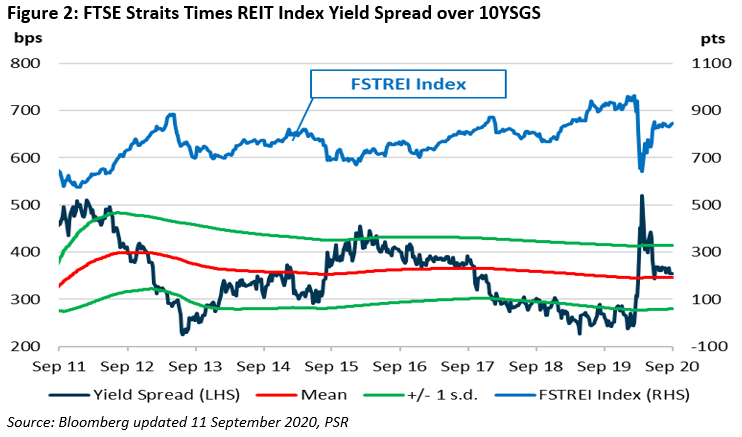

The FTSE S-REIT index has been trading sideways for the past 4 months, with dividend yield hovering around 4.4% to 4.6%. Current dividend yield stands at 4.5%.

Similarly, dividend yield spread has been in the 3.6% to 3.8% range over the corresponding period. Current dividend yield spread of 3.5% is at the +0.11 SD level.

3MSOR at 0.2% is at 9-year lows, 155bps lower YoY, while the 10YSGS at 0.9%, was 84bps lower YoY.

SUBSECTOR MONTHLY INDICATORS

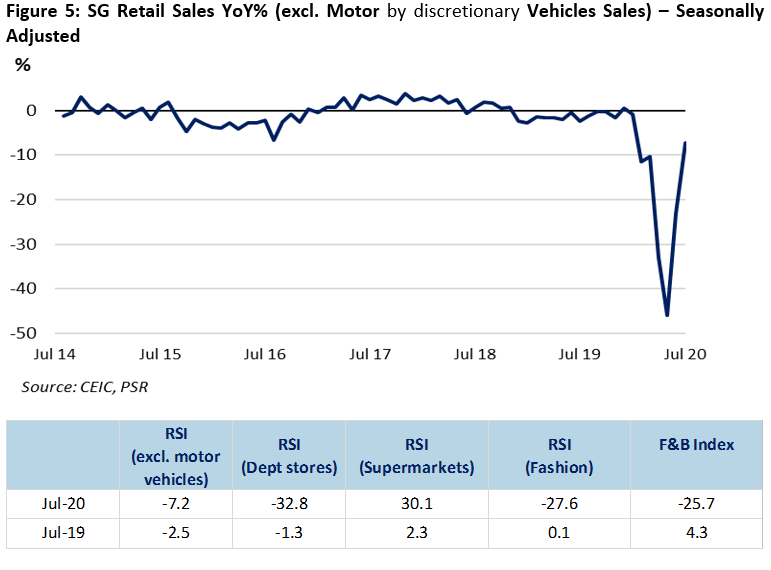

The RSI (Ex MV) made a “V-shaped” recovery with July’s figures down only 7.2% YoY. Discretionary trade categories such as recreational goods, watches & jewellery, departmental stores, furniture & household and fashion drove the recovery.

Computer and telecommunication equipment category maintained its second consecutive month of c.20% growth.

The FMCG segments, supermarkets (+30.8%) and mini-marts and convenience stores (+3.8%) remained in the green, albeit growth has slowed.

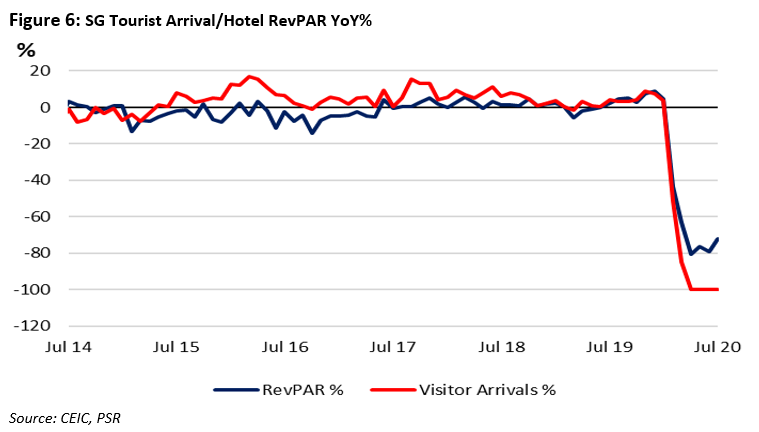

RevPAR improved 7.2ppts MoM, lifted by the Luxury, Upscale and Midscale segments, on the back of higher room rates and occupancy. We opine that this was due to the staycation take-up, as international borders remain closed. Staycation demand will likely be more pronounced in the following months.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: