SECTOR SNAPSHOT

Extension of the Job Support Scheme (JSS) by up to 7 months

Previously, the JSS provided 25% to 75% in wage subsidies for a 10-month period till August 2020. Under the extension, firms will receive between 10% to 50% of monthly wages for each local employee, depending on the project recovery of their different sectors. The Hospitality and Retail sectors, which are the harder hit sectors, will benefit from an additional 7 months of wage support for local employees at 50% (prev. 75%) and 30% (prev. 50%) respectively. This will help accommodation operators/owners and retail tenants offset some operating cost and ride out the period of lower earnings.

Initiatives to boost domestic tourism

The government has earmarked $320mn in tourism credits (SingapoRediscovers Voucher) to drive local spending to Singapore’s eateries, shops, hotels and leisure attractions. While more details will only be released by the Ministry of Trade and Industry (MTI) in September 2020, we think that some of the tourism credits will be channeled to offset staycation packages.

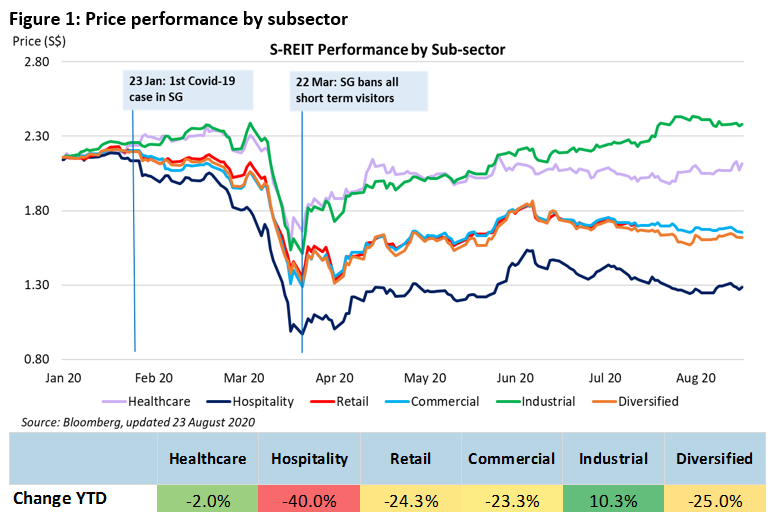

The recovery since has been varied as well – the seemingly more resilient healthcare and industrial sectors have recovered roughly 55% to 59% of their fall in share prices, while the commercial sector has recovered by 37% and retail by 30%, with hospitality recovering only 21% of their value (figure 1).

Office:

As the telecommuting “experiment” wears on and the novelty of remote working wears off, the value added by offices becomes clearer and is synonymous with mentoring, collaboration, corporate culture and creativity. We think flex space will play a more prominent role as an intermediate solution, as businesses revaluate their leasing strategies, and as scalable solution for space (core+flex model). That said, there is no one-size-fits-all occupier strategy, and we expect some attrition in office demand as from adoption of flexible work arrangement.

The pausing of densification trends due to social distancing, construction slippage (figure 10), as well as muted supply coming onto the market will provide near-term support for the office sector. Supply coming onto the market in the core CBD area is at the 5-year historical average of 0.9mn sqft, in comparison to supply of 1.2mn sqft during the GFC (figure 8). So far, two CBD commercial owners are revaluating redevelopments to unlock additional GFA from the CDB and Strategic Development Incentive Schemes. c.700,000sqft from AXA Tower (50:50 JV between Perennial and Alibaba) and CDL’s 353,575 sqft Fuji Xerox Tower and 131K sqft Central Mall will potentially be displaced in 2021/22, if plans for redevelopment proceed as planned. AXA Tower, Fuji Xerox Towers, reduction in supply when assets are taken offline for redevelopment, which is likely to take place in 2021.

Industrial:

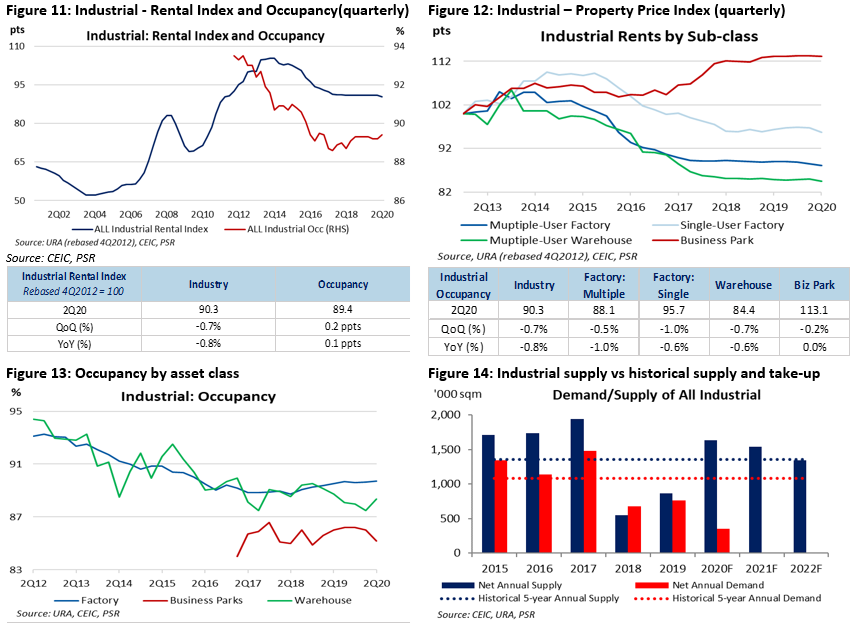

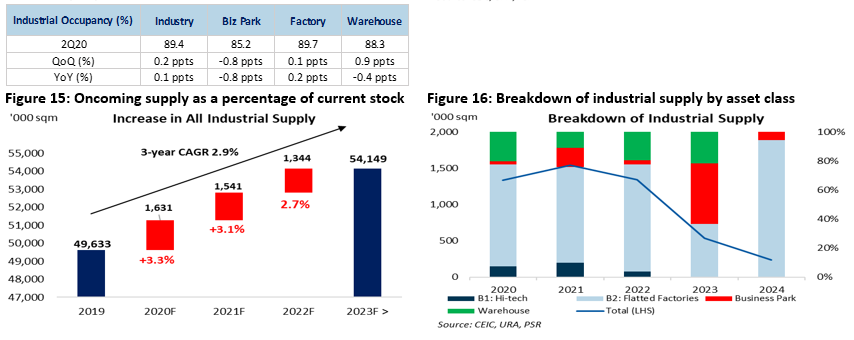

Industrial rents were resilient, dipping -0.2% to -1.0% QoQ across asset classes. Industry occupancy inched up 0.2ppts due to short-term stock piling demand in the warehouse subsector (+0.9ppts). Future trends of e-commerce prevalence and increased adoption of cloud computing will likely see an uptick in demand for logistics and data centres assets.

New supply of industrial space coming on to the market in FY20/21 represents 3.3%/3.1% of existing supply. However, a closer look at the oncoming supply reveals that c.70% of FY20/21 supply will be from light industrial flatted factories, of which 50%/68% of light industrial supply will be leased to single tenants (i.e.: build to suit with a committed occupancy of 100%). Muted supply across all other segments will help to provide support for rents.

Retail:

The Retail Sales Index (excl. Motor vehicles) fell 23.3% YoY, recovering from May lows of -46.3% as Singapore exited the Circuit Breaker with physical retail stores re-opening in Phase Two. Supermarkets (+46.3%) and hypermarkets, minimarts and convenience stores (+9.1%), and computer and telecommunications equipment (+21.6%) were the only segments to post sales expansions, likely attributed to continued work-from-home arrangements.

Capacity constraint in malls and particularly in dine-in establishments are partially alleviated by more balanced customer-flow throughout the day.

Hospitality:

International Tourist Arrivals (IVA) and RevPARs still depressed as Singapore’s borders remain closed, although fast lane arrangement for business with certain countries are under negotiation. Alternative sources of income such a block-bookings by the government for isolation purposes lifted occupancies to the 40% – 80% range. Singapore gave the green light for general travel to Brunei and New Zealand from 1 September 2020 onwards. As international travel restrictions are progressively lifted, the need for dedicated isolation facilities for arriving and returning travelers will continue to provide block-booking demand. Recovery for the hospitality sector is expected to be slow in 2020. Fear and caution after international travel bans are lifted may keep visitors away. Recovery in the sector is reliant on the vaccine timeline.

INVESTMENT ACTIONS

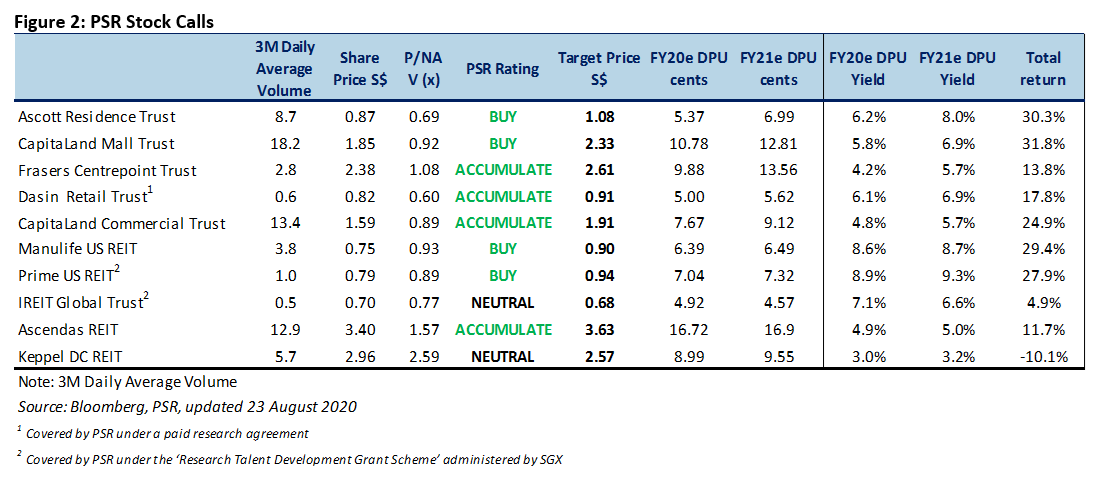

Maintain OVERWEIGHT on the S-REITs sector

We continue to view REITs as a stable yield investment. We believe that SREITs may emerge stronger will more future-ready portfolios, resulting in a re-rating of the SREITs sector due to:

Top-down view (unchanged)

We like the Commercial and Industrial sub-sectors due to tapering office supply after the surge in supply in the prior two to three years, and the AEI and redevelopment opportunities for the Industrial sector. The tenants in these two sectors are also less affected by the COVID-19 outbreak. We are cautious on the Hospitality and Retail sub-sector due softer tourism sentiment and retail outlook, exacerbated by lingering fears of another wave of COVID-19 outbreak.

Tactical bottom-up view (unchanged)

REITs that can better weather through the rising interest rate environment would be those with:

1) Well-distributed lease expiries 2) High-interest coverage; 3) Long weighted average debt to maturity; and 4) percentage of guaranteed revenue through “fixed” or “stable” leases.

MACROECONOMIC ENVIRONMENT

OFFICE

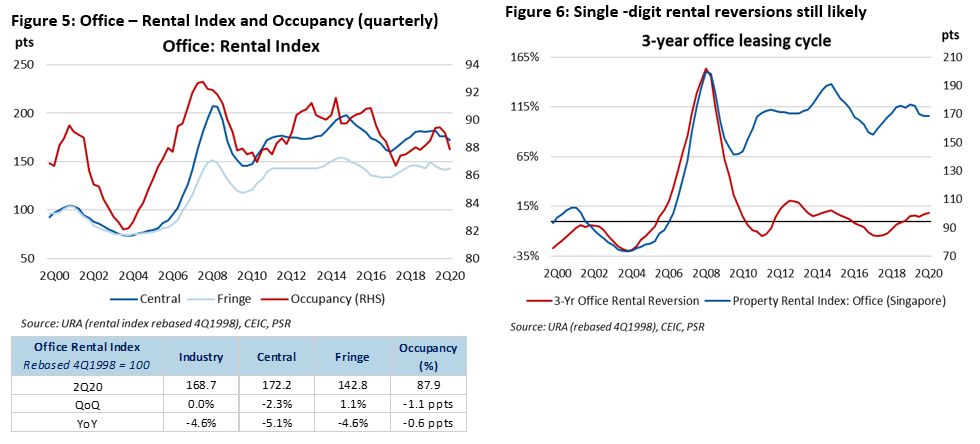

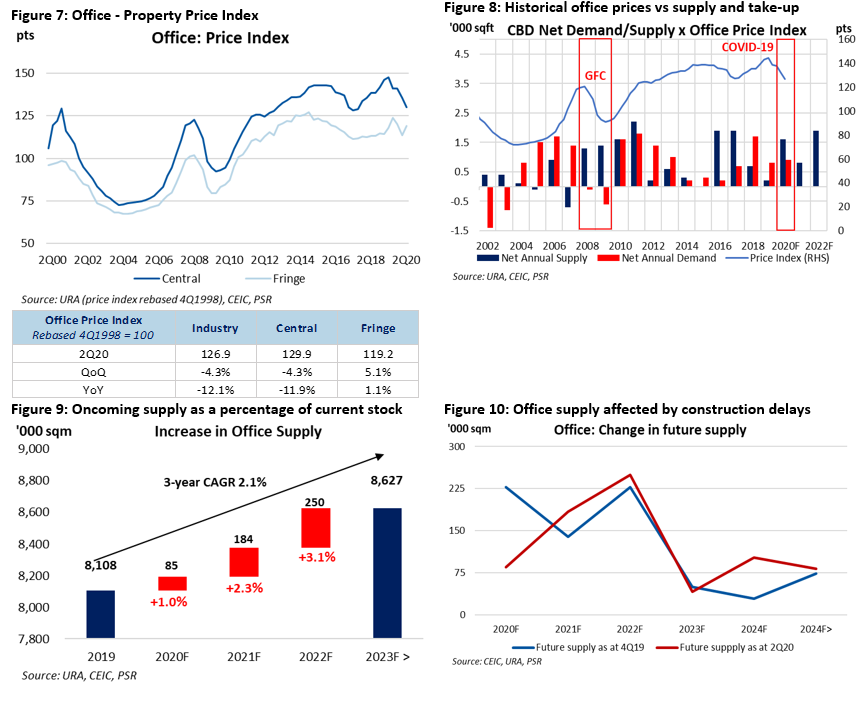

Occupancy dipped 1.1ppts in 2Q20 to 87.9%, reversing the improvement in occupancy in 2H19. The rental index was unchanged QoQ, as the 1.0% improvement in the fringe rental index offset the 2.3% dip in the central index. Movement in office prices were more pronounced, falling 4.0%/ 4.3% in 1Q/2Q respectively. Divergence between central and fringe assets, with fringe assets holding up better, registering a 1.1% YoY increase in price index versus the -11.9% observed for central office prices.

While softer leasing is expected, positive rental reversions are still likely for the office sector which typically follows a 3-year leasing cycle (figure 6), as expiring rents are still 5% to 25% below current market rents.

In line with the government’s directives for companies to employ telecommuting, the percentage of tenants operating in offices remains low at 10-25%. As the telecommuting “experiment” wears on and the novelty of remote working wears off, the value added by offices becomes clearer and is synonymous with mentoring, collaboration, corporate culture and creativity. We think flex space will play a more prominent role as an intermediate solution, as businesses revaluate their leasing strategies, and as scalable solution for space (core+flex model). That said, there is no one-size-fits-all occupier strategy, and we expect some attrition in office demand as from adoption of flexible work arrangement.

The pausing of densification trends due to social distancing, construction slippage (figure 10), as well as muted supply coming onto the market will provide near-term support for the office sector. Supply coming onto the market in the core CBD area is at the 5-year historical average of 0.9mn sqft, in comparison to supply of 1.2mn sqft during the GFC (figure 8). So far, two CBD commercial owners are revaluating redevelopments to unlock additional GFA from the CDB and Strategic Development Incentive Schemes. c.700,000sqft from AXA Tower (50:50 JV between Perennial and Alibaba) and CDL’s 353,575 sqft Fuji Xerox Tower and 131K sqft Central Mall will potentially be displaced in 2021/22, if plans for redevelopment proceed as planned. AXA Tower, Fuji Xerox Towers, reduction in supply when assets are taken offline for redevelopment, which is likely to take place in 2021.

INDUSTRIAL

Industrial rents were resilient, dipping -0.2% to -1.0% QoQ across asset classes. Industry occupancy inched up 0.2ppts due to short-term stock piling demand in the warehouse subsector (+0.9ppts). Future trends of e-commerce prevalence and increased adoption of cloud computing will likely see an uptick in demand for logistics and data centres assets.

New supply of industrial space coming on to the market in FY20/21 represents 3.3%/3.1% of existing supply. However, a closer look at the oncoming supply reveals that c.70% of FY20/21 supply will be from light industrial flatted factories, of which 50%/68% of light industrial supply will be leased to single tenants (i.e.: build to suit with a committed occupancy of 100%). Muted supply across all other segments will help to provide support for rents.

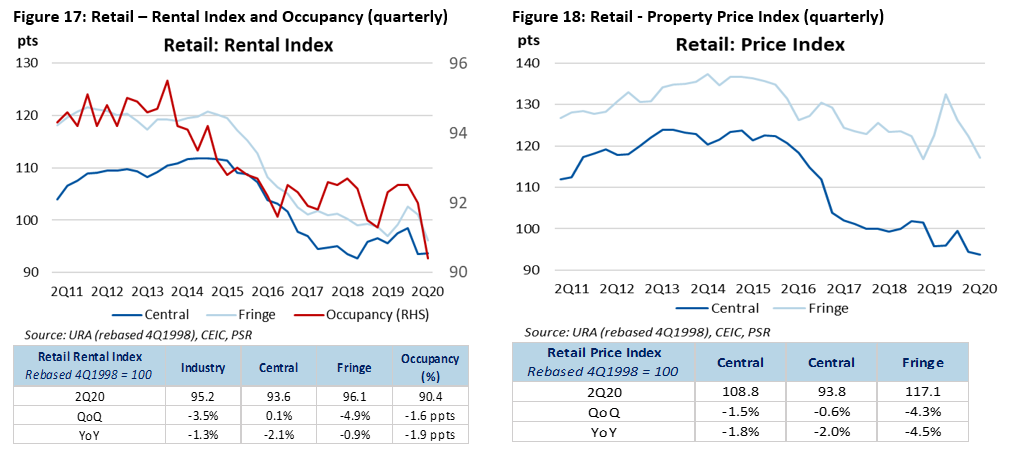

RETAIL

Occupancy fell by 1.6ppts QoQ to 90.4% while the retail rental and price index fell 3.5% and 1.5% QoQ, weighed down by fringe assets.

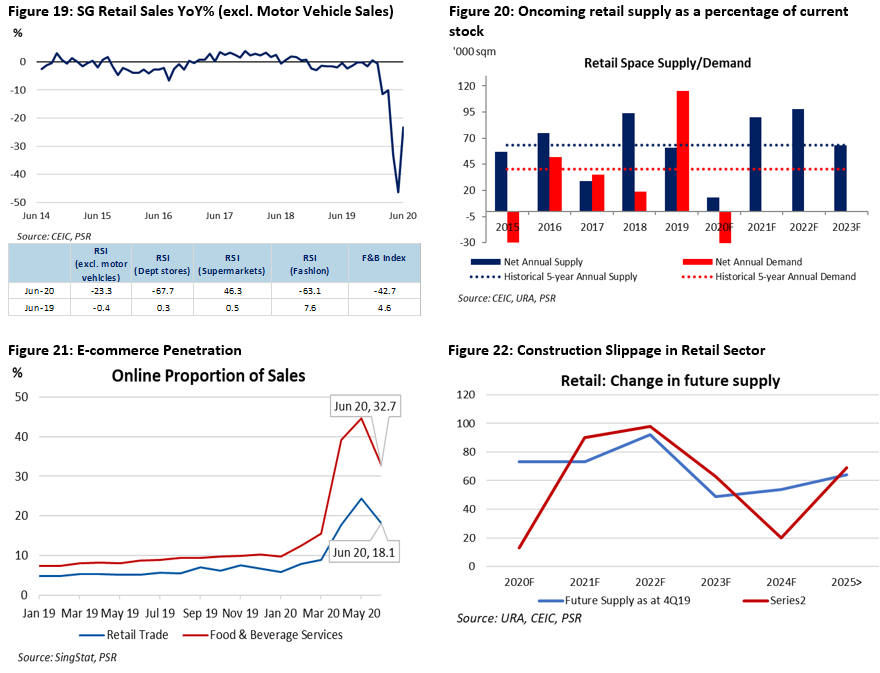

The Retail Sales Index (excl. Motor vehicles) fell 23.3% YoY, recovering from May lows of -46.3% as Singapore exited the Circuit Breaker with physical retail stores re-opening in Phase Two. Supermarkets (+46.3%) and hypermarkets, minimarts and convenience stores (+9.1%), and computer and telecommunications equipment (+21.6%) were the only segments to post sales expansions, likely attributed to continued work-from-home arrangements.

Singstats estimates the total retail sales value in June 2020 was about $2.6 billion. Of these, online retail sales made up an estimated 18.1%. Online retail sales of the Computer & Telecommunications Equipment, Furniture & Household Equipment and Supermarkets & Hypermarkets industries made up 69.9%, 45.6% and 10.7% of the total sales of their respective industry.

Sales of food & beverage services fell 43.5% YoY, compared to the 50.1% decline in May 2020, with the resumption of dine-in services in Phase Two. The total sales value of food & beverage services in June 2020 was estimated at $496 million. Of these, online food & beverage sales made up an estimated 32.7%.

Capacity constraint in malls and particularly in dine-in establishments are partially alleviated by more balanced customer-flow throughout the day.

Most of the retail supply hitting the market are part of mixed-use developments with <10,000sqft of retail space, hence indirectly competitors of suburban malls in those locations. Construction slippage (figure 22) will also help to support rents.

HOSPITALITY

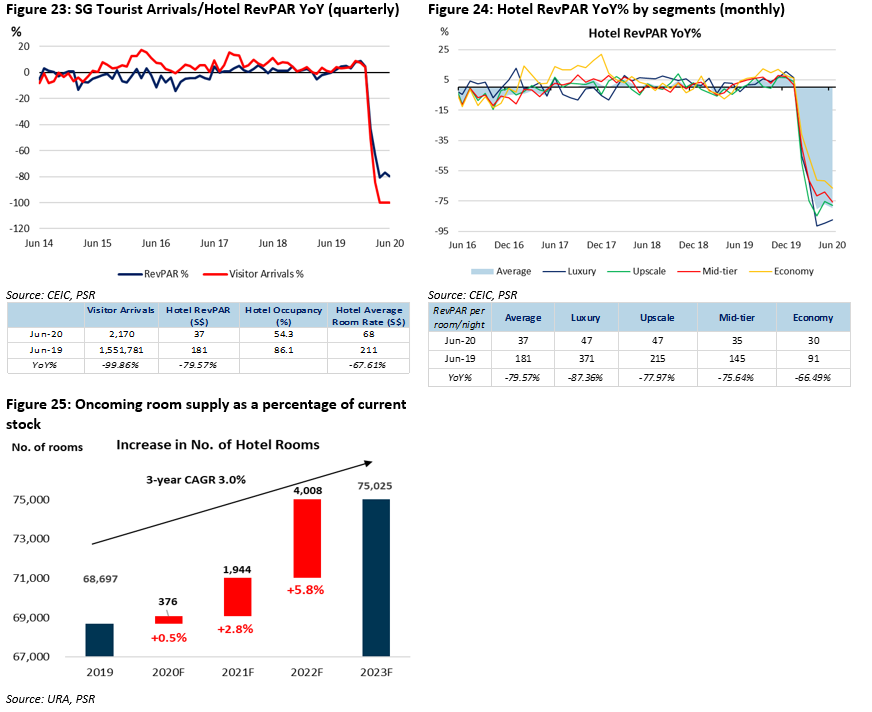

Low supply of rooms hitting the market over the next 3 years bodes positively for the SG hospitality sector. Room supply is expected to grow by 1.1%/1.0% in FY20/FY21.

International Tourist Arrivals (IVA) and RevPARs still depressed as Singapore’s borders remain closed, although fast lane arrangement for business with certain countries are under negotiation. Alternative sources of income such a block-bookings by the government for isolation purposes lifted occupancies to the 40% – 80% range. Singapore gave the green light for general travel to Brunei and New Zealand from 1 September 2020 onwards. As international travel restrictions are progressively lifted, the need for dedicated isolation facilities for arriving and returning travelers will continue to provide block-booking demand. Recovery for the hospitality sector is expected to be slow in 2020. Fear and caution after international travel bans are lifted may keep visitors away. Recovery in the sector is reliant on the vaccine timeline.

Hospitality REITs are have reported an uptick in domestic demand to after they were allowed to accept staycations bookings. Hotels likely to draw staycation demand are those luxury/upscale of resort-styled accommodations. However, significant discounts will still have to be offered to attain the sweet spot, which may be subsidized by the $320mn SingapoRediscovers initiative to boost local tourism. Pent-up demand for travel will lead to a strong recovery for the hospitality sector in 2021.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: