SDAV expected to perform as global economy and domestic property market improves.

Global equities markets have risen on the back of improving economic growth around the globe. This has benefited Singapore listed companies in the finance, technology and consumer services sectors. Property stock prices have also begun to rise as the domestic property market sentiments improved dramatically on the back of strong residential enbloc sales momentum. Average SDAV from July to September was S$1.16bn, higher than the preceding average SDAV of S$1.15bn from April to June.

Episodic regional tensions and regulatory changes help drive trading volumes for SGX’s foreign currency and equity index futures.

USD/CNH futures saw stronger traded volumes during heightened tensions in the Korean Peninsula. A replay of this tension could see hedgers drive up the USD/CNH traded volume. At the same time, regulatory changes in China and India have encouraged market participants to approach SGX as a platform to trade USD/CNH, INR/USD and China A50 futures.

However, new IPOs have not been able to keep pace with the number and size of companies slated for delisting.

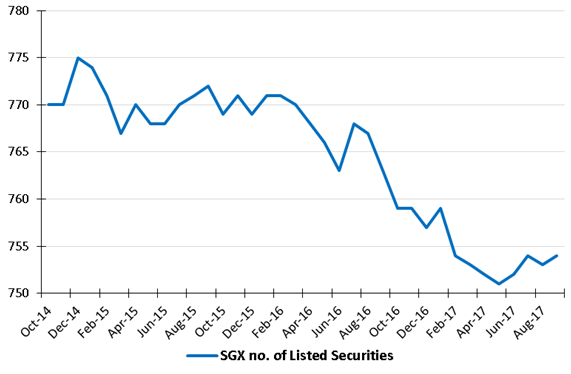

The number of listed securities on SGX have been on a decline and there is a lack of large cap stocks with high free float to replace the delistings. A review on listing rules could address the falling number of listed securities. And we expect the delisting of Global Logistics Properties to have an impact on the securities traded volumes.

INVESTMENT ACTIONS

We are revising our FY18e SDAV to c.S$1.16bn from previous estimate of S$1.08bn as stock market capitalisation and trading volumes improve. We think that FY18e operating expenses could come in above the guided range of S$425mn to S$435mn as business activity picks up hence we estimate FY18e operating expenses to be c.S$440mn. Our estimates for FY18e total derivatives volume is also revised upwards to 187mn contracts (previous estimate 180mn contracts). We expect SGX’s 1Q18 revenue to come in at S$218mn and PATMI to be at S$93.5mn, up 12.5% YoY. We expect 1Q18 operating expenses to come in at c.S$109mn, forming 24.8% of our FY18e operating expense forecast.

Given the expectation of better overall performance this year, we expect FY18e total DPS to increase by S$0.04 from FY17 total DPS of S$0.28 to S$0.32. Maintain Accumulate with higher TP of S$8.39 (previous TP of S$7.63).

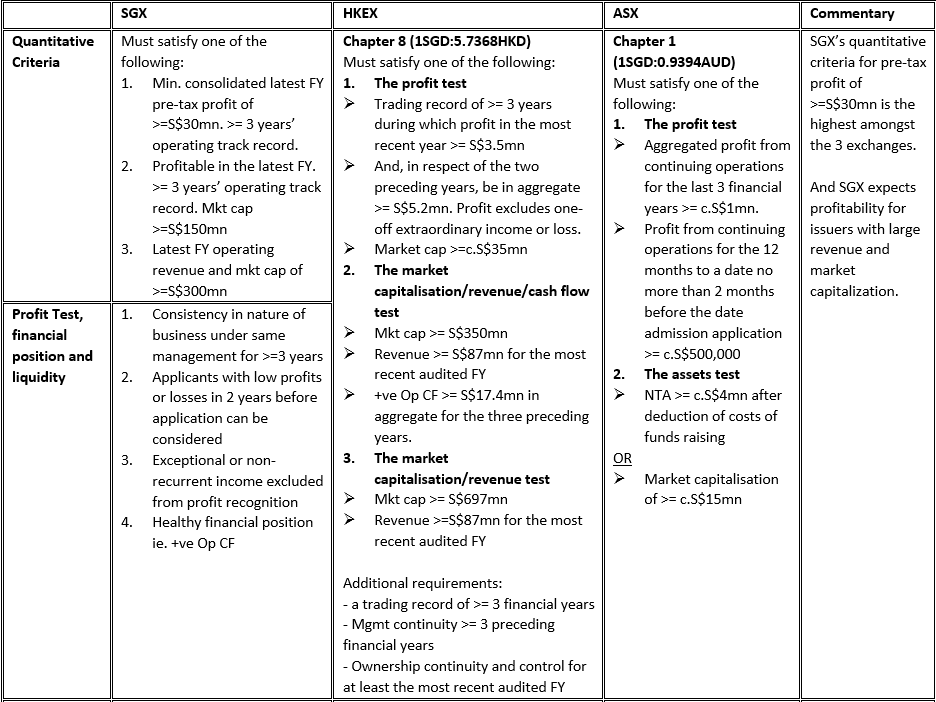

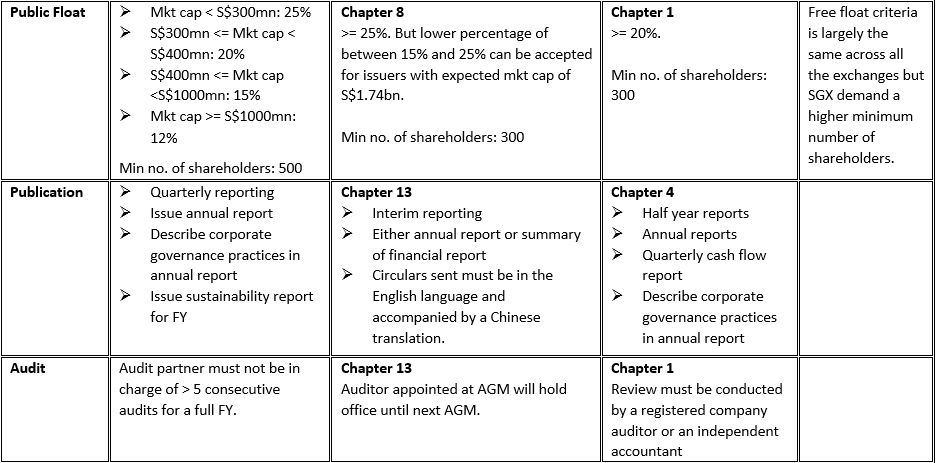

Brief summary of selected Listing Rules for comparison. Please refer to actual exchange rules for more details and conditions.

Challenges to SGX’s Securities business.

Competition from HKEX Stock Connect with Shanghai and Shenzhen. The connection allows Hong Kong listed firms will have a wider audience from mainland China via southbound trades. At the moment, mainland individual investors must have a balance of RMB500,000 in their cash and securities accounts to be eligible to trade Hong Kong listed stocks. Companies may be listing on HKEX in anticipation of any possible relaxation to the eligibility and quota for southbound trades.

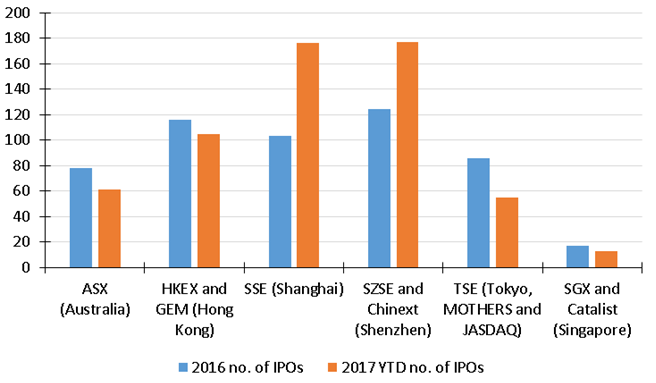

SGX’s IPO listing requirements are stricter. SGX’s higher requirements for profitability, market capitalisation, revenues and cash flow compared to HKEX and ASX reduces the pool of eligible issuers. Even though Razer Inc and Sea Limited’s (formerly known as Garena) could qualify based on valuations and revenues, the consideration for profit criteria is weak because in both cases the losses have widened in FY15 and FY16. SGX face a conundrum where the large companies avoid it for the poorer liquidity, whilst smaller candidates avoid it for the stricter listing requirements.

More costly to maintain listing on SGX. The additional costs from quarterly reporting and issuance of annual sustainability reports may discourage issuers from listing on SGX.

Better valuation from overseas listing. Growth prospects for Singapore companies are increasingly driven by overseas expansion. Singapore companies may find that better valuations in overseas markets where they have been operationally active and are gaining strong growth traction especially for consumer goods and services companies whose branding has a stronger visceral effect on the local retail market.

Singapore’s IPO market has been slow but pipeline strategy in the works. SGX has partnered with IMDA to help high growth Infocomm and Media (ICM) companies that are accredited by IMDA to leverage capital markets for expansion. The accreditation process has helped the accredited companies generate over S$80mn worth of government project pipeline (S$70mn in May 2017) and helped the companies raise over S$59mn in new investment capital (S$28.9mn in May 2017).

Figure 1: The number of IPOs on the SGX pale in comparison to its regional peers

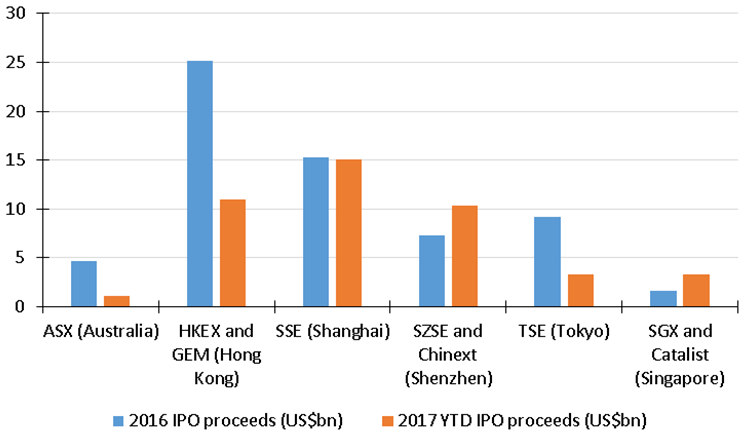

Figure 2: SGX’s 2017 YTD IPO proceeds exceeded 2016 because of the Netlink Trust IPO which raised S$2.3bn.

Figure 3: SGX’s listed securities are on a decline as IPOs had been slow and delistings are accelerating.

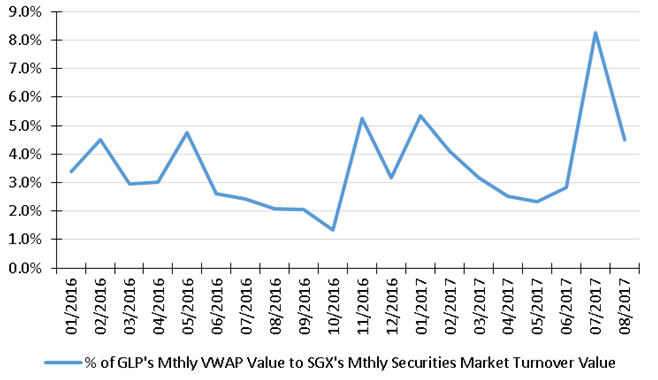

Delisting of Global Logistics Properties (GLP) could reduce SGX’s monthly securities market turnover value by c.3.6%. With a market capitalisation of S$15.5bn, GLP is ranked 11 in the STI stocks list by market capitalisation. GLP has a free float of c.38%. As of 29 Sept 2017, GLP’s total return YTD is 52.8%. Owing to its high market capitalization and sizable free float, we estimate GLP’s average monthly Volume Weighted Average Price (VWAP) turnover value (monthly average VWAP x monthly volume) over the period from January 2016 to August 2017 to be S$851mn. This is about 3.6% of SGX’s average monthly securities market turnover value of S$23.6bn. We also think that the recent big weight IPO of Net Link Trust will not fully compensate for the delisting of GLP slated to be completed by 14 April 2018. Though Net Link Trust has a free float of c.75% (Twice of GLP’s free float), the market capitalization of S$3.2bn is only slightly more than one-fifth of GLP’s market capitalisation.

Figure 4: GLP’s monthly VWAP value could go as high as 5% to 8% of SGX’s monthly Securities Market Turnover Value.

Major developments to SGX’s derivatives business at the start of FY18 (Financial Year Ending in June).

Continued market dominance in iron ore derivatives market outside China. As SGX controls 95% of the Iron Ore Futures market outside China, the other 5% is controlled by CME. CME has been aggressive in pushing their traders to ramp up volume in Iron Ore futures but we do not think CME poses a threat as CME’s Asian office is only a representative office so their infrastructure and support is not on par with SGX. Besides, CME operates in the European time zone therefore will not see most of the trading activity that happens during the Asian time zone. As such, SGX will not be expected to reduce Iron Ore futures contract fees to compete with CME.

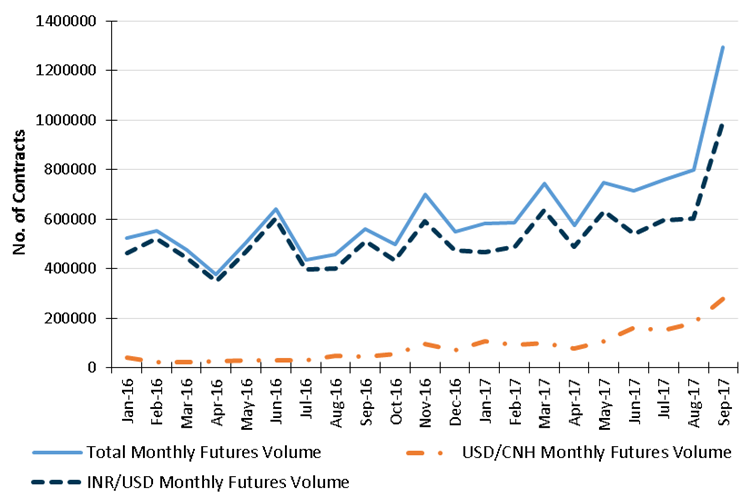

INR/USD futures performance shot through the roof as regulations in India’s domestic derivatives market tightens and volatility picked up. Foreign use of Indian domestic derivative products through Offshore Derivative Instruments (ODIs) also known as participatory notes (P-Notes) is now restricted for the purpose of hedging equity shares held. Therefore as global portfolio managers cut their exposure to Indian equities between July and August, the notional value of ODIs on Derivatives declined sharply over the same period. With reduced exposure to onshore Indian derivatives, foreign market participants will not be able to trade the volatility onshore but trade them offshore. Indeed when volatility picked up in the latter half of September, SGX experienced stronger INR/USD traded volumes.

Korean Peninsula tensions, Chinese central bank action and improving China A50 traded volume helped boost USD/CNH futures volume and market share. The USD/CNH futures benefited from higher volatility as the renminbi strengthened in early September amid rising North Korean missile threat then weakened when the Chinese central bank relaxed certain hedging and reserve related rules that were originally in place to limit the renminbi decline. We believe improving China A50 trading volumes following the relaxation of stock index futures trading rules in China early this year also helped SGX gain market share in the USD/CNH futures market because of hedging synergy between USD/CNH and China A50 futures.

We do not see the listing of Asia Pacific Exchange (Apex) as the third derivatives exchange in Singapore a major threat. Apex plans to open its exchange with refined palm oil contracts which SGX does not offer as a derivatives product. However, if Apex decides to offer iron ore and coking coal futures contracts, there will be competition for SGX Iron Ore futures market share outside China. Apex is majority owned by a China markets veteran, Mr Eugene Zhu Yuchen who held a senior position at Dalian Commodity Exchange. Dalian Commodity Exchange has the largest Iron Ore futures market with trade volume of 465 million Iron Ore futures contracts YTD. In comparison, SGX, which controls 95% Iron Ore market share outside China, had managed 10 million Iron Ore futures contracts YTD. Given Mr Eugene Zhu’s background, we think that Apex may eventually roll out iron ore futures contracts to capture and grow the market outside China. But being based in Singapore, we believe that adherence to rules pertaining to “risk-based” exposures wherein customers have to fulfil stricter margin requirements and maintain a special reserve fund would raise the bar for Apex’s growth strategies. We estimate that SGX’s margin requirement is between 11% and 14% compared with Dalian Commodity Exchange’s minimum of 5%.

Figure 5: INR/USD and USD/CNH futures are SGX’s main FX derivatives products with INR/USD futures making the bulk of it.

Figure 6: China A50 volume bottomed out in early 2017 following the relaxation of stock index futures trading rules in China.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Jeremy covers primarily the Banking and Finance sector. He has 6 years’ experience in equities related dealing and research roles.

He graduated with Bachelors of Mechanical Engineering from Nanyang Technological University.