China

Slight relaxation of air pollution control for the upcoming winter. In Sep-18, China’s Ministry of Ecology and Environment and other commissions jointly issued an air pollution-control plan for the Beijing-Tianjin-Hebei region and surrounding areas for the fall and winter spanning 2018-2019. The new plan calls for a 3% reduction of PM2.5 and a 3% drop in the number of severely polluted days during the period from Oct-18 to Mar-19. Meanwhile, production schedules for the steel, coking, and foundry industries should take turns peaking to reduce air pollution. The production of steel in hot weather was limited to 50% of capacity in key cities. Other cities were told to cut production by no less than 30%. Enterprises that failed to follow these regulations would have their electricity cut.

Restriction on coal import remains. In Oct-18, NDRC held a six coastal provinces joint conference pertaining to coal import. The authority reiterated that the restriction on coal imports would be on par with last year. There is no new quota being issued.

Indonesia

Lifting 2018 domestic production target. In Sep-18, Indonesia raised the 2018 coal production target from c.485mn tonnes to c.507mn tonnes. The additional output quotas of 21.9 million tonnes are split among 32 coal miners and will be all exported. Indonesia’s coal consumption for power by PLN and independent power producers is expected to reach 88.5mn tonnes in 2018, below a target of 92mn tonnes. PLN expects coal consumption to increase to 96mn tonnes in 2019.

Facing a hurdle to ramp up production. In Sep-18, according to the interview with Pandu Sjahrir, chairman of the Indonesian Coal Mining Association, Producers in the world’s largest shipper face an order backlog of 18 months as they are not able to get hold of additional mining equipment. The slow ramp-up in supply will probably keep coal prices buttressed at about $100 a metric ton through the end of next year.

The China authority learned lessons from last winter’s coal-to-gas conversion program

It is expected to see another peak demand for coal in winter which is coming soon. China government simply imposed one solution for coal-to-gas conversion program last year to fulfil the target of a reduction of greenhouse and polluted gas emission. The program prohibits residents from using coal. Some thermal plants and steel mills in the north of China have to shut down. In retrospect, it was considered a failure. Hence, the authorities are now slowing down the pace of reduction rather than an abrupt cut in coal consumption this year. Since the demand for thermal power could surge in the near term, see Figure 3, the authority still aims to assure the profitability of domestic coal producers. Accordingly, the domestic production growth in China turned positive in Aug-18, see Figure 1. We believe the market players have started to stock up coal for winter. We cannot rule out the possibility that a new round of restriction on coal imports during winter. As of Sep-18, the port coal inventory continued to level up (+52% YoY), see Figure 6.

External demand favours the coal miners in Indonesia

In Jul-18, the coal exports reached a new high since Mar-14, arriving at 38mn tonnes in Indonesia, see Figure 2. With the increase in export target announced by the authority, the export demand will see new highs in 4Q18. However, the room for growth of production is limited due to the bottleneck of capacity resulting from equipment supply. We believe this is a short-term issue, and it will take 3 to 6 months to ramp up capacity. Though HBA started to correct from the high of US$107.8/tonne, the temporary shortage of supply will uphold the price in the near term. We expect HBA to average at US$100/tonne in 4Q18.

Coal counters monthly updates

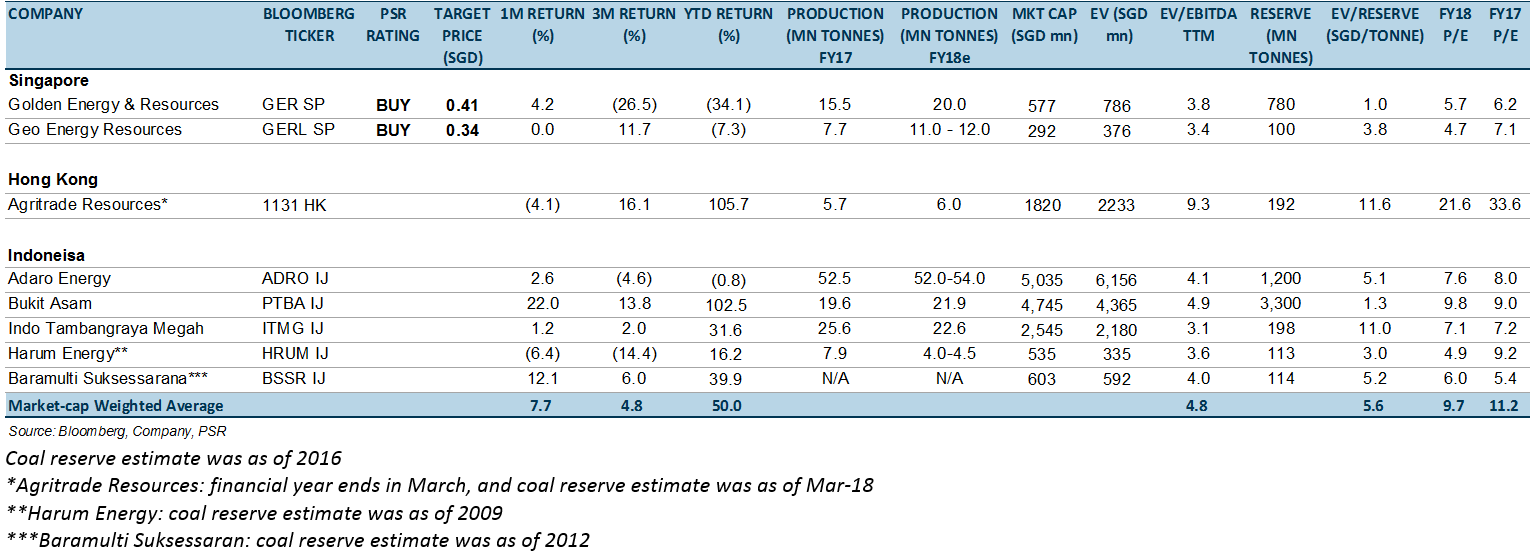

Golden Energy and Resources (Target px: S$0.42 / BUY)

Geo Energy Resources (Target px: S$0.34/ BUY)

Investment action

We remain positive on the sector as we expect coal price (FY18e ASP 4,200 GAR: US$41/tonne, 1H18 ASP 4,200 GAR: US$48.6/tonne) will be favourable for coal miners. Meanwhile, the ramp-up of production is still on track. We maintain an OVERWEIGHT rating on the coal sector.

Peer comparison

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Guangzhi graduated from Singapore Management University with a Master degree in Applied Finance and from South China University of Technology with a Bachelor degree in Electronic Commerce.

The current sector coverages include Energy, Utilities, and Mining sectors. He has 3 years experience in equity research in both Hong Kong and Singapore market. He is the mandarin spokesperson for Phillip Securities Research in relation to China-related projects and all mandarin seminars and client events.