And why did we upgrade DBS?

As competition increase, we expect NII to be led by loans volume growth. DBS has the highest Singapore CASA ratio of 91% and the largest overall deposit base of S$342.9bn. This will mean UOB and OCBC will not be able to lend more competitively than DBS. We believe this is the advantage DBS enjoys over its peers, especially against foreign banks like HSBC and BOC as they begin to compete for loans in Singapore.

Loans Growth will be the driver for better NII.

Singapore banks’ NII performed better because of stronger loans growth. The actual loans growth rate in 1H17 had exceeded bank managements’ guidance of mid-single digit loans growth. The recent improvements to economic outlook across Singapore banks’ key markets including Malaysia and Hong Kong will continue to support loans growth and positive loans volume and rate dynamics. However, we expect the pass through of higher interest rates to be crimped by competition especially in the property sector therefore NIMs expansion may be more subdued.

We expect excess capital to be returned to shareholders in the form of higher dividends.

We think that the build-up of excess CET 1 above the regulatory hurdle of 6.5% and the threat of negative economic value as WACC exceeds ROIC may spur the Singapore banks to return some excess capital to shareholders. We opine that the banks may experience lower ROIC because of our view of a more subdued NIMs. Therefore capital that cannot be deployed to improve ROIC above WACC may instead be returned to shareholders.

INVESTMENT ACTIONS

Upgrade to NEUTRAL Singapore Banking Sector – We upgrade the Singapore Banking Sector to Neutral weight from Underweight. Macro conditions have been more positive than we expected. We expect higher interest rates and loan volume to help drive NII higher.

We maintain our Reduce rating on UOB and Neutral rating on OCBC. And we upgrade our rating on DBS from Neutral to Accumulate.

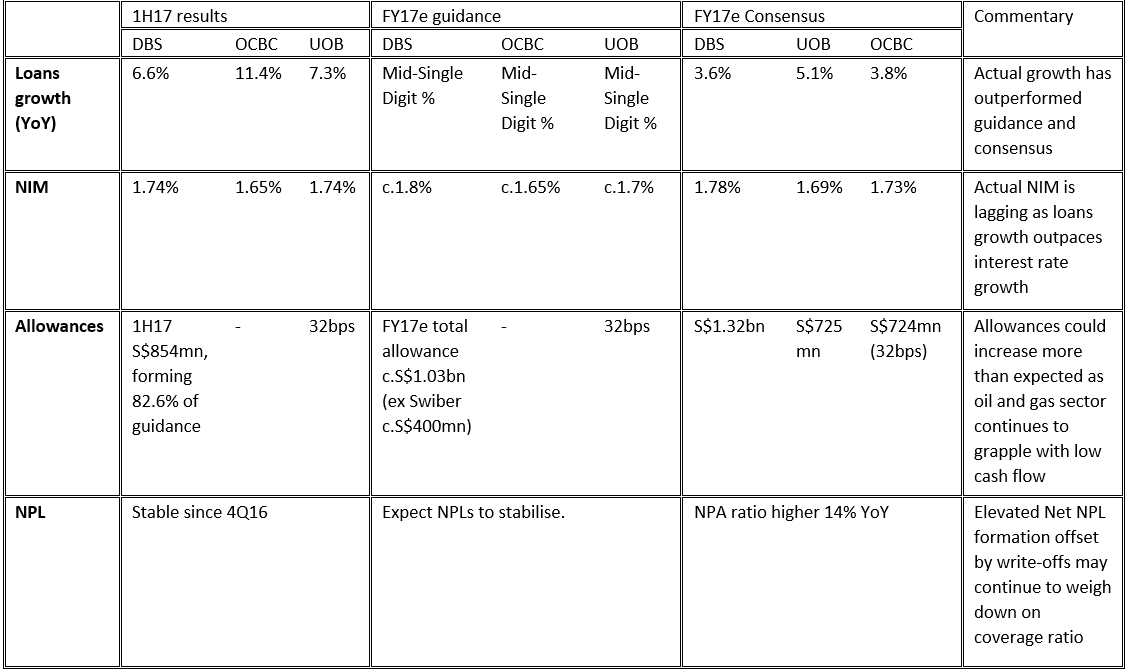

Loans growth is better than consensus but NIM and allowances are generally in line.

Source: Bloomberg, PSR estimates

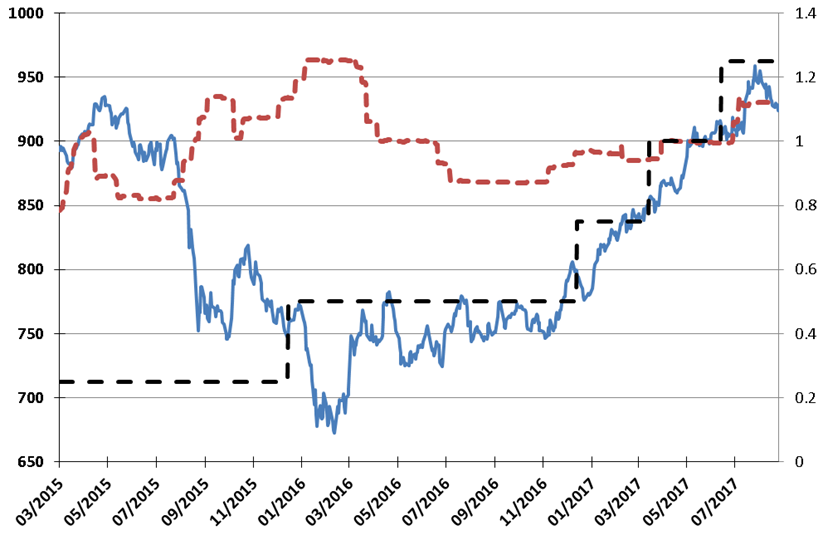

How did Singapore banks’ share price move in comparison with interest rates?

Contrary to market expectations that a rising SIBOR is always beneficial for Singapore banks, we have seen increasing SIBOR result in a steep fall in share prices. Therefore we highlight that the conditions in which SIBOR moves are more important than the direction of movement.

Source: Bloomberg, PSR estimates

How was the progress for the Singapore banks so far?

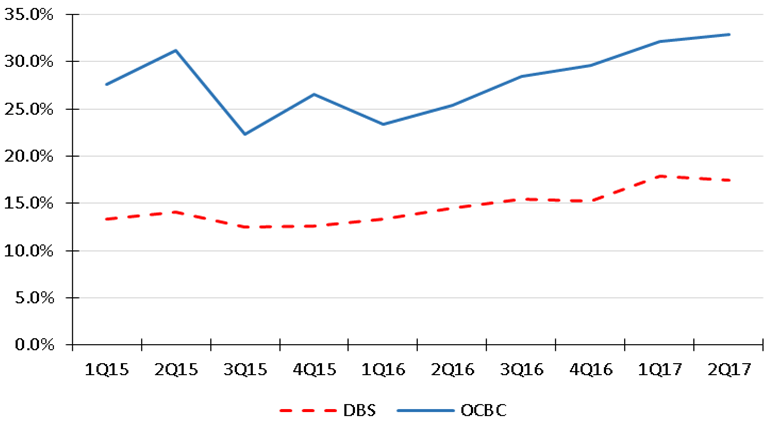

a) Strong growth in DBS and OCBC WM; UOB is lagging behind.

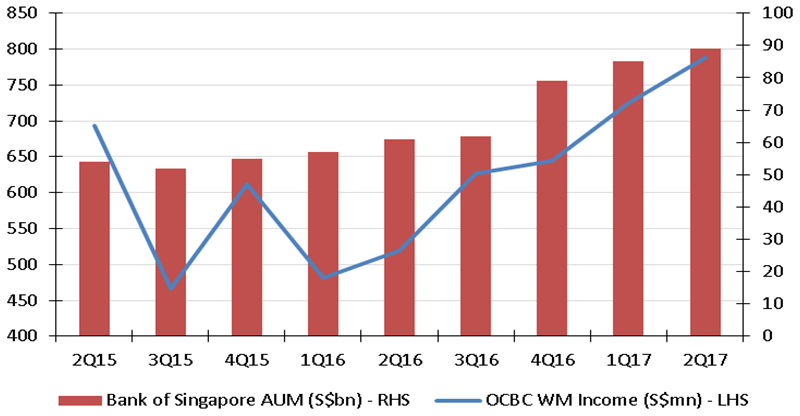

OCBC’s stronger WM contributions came from the completion of Barclays WM business acquisition in 4Q16 and the broader mix of WM products and services from its bancassurance arm and the Lion Global franchise. Owing to improving investor sentiments or risk appetite from the start of 2017, expect OCBC WM to continue performing well on the back of growing AUM and product synergies (See Fig. 2). OCBC has announced the acquisition of NAB’s private wealth business in Singapore and Hong Kong which is expected to be completed at the end of 2017 subject to regulatory approval.

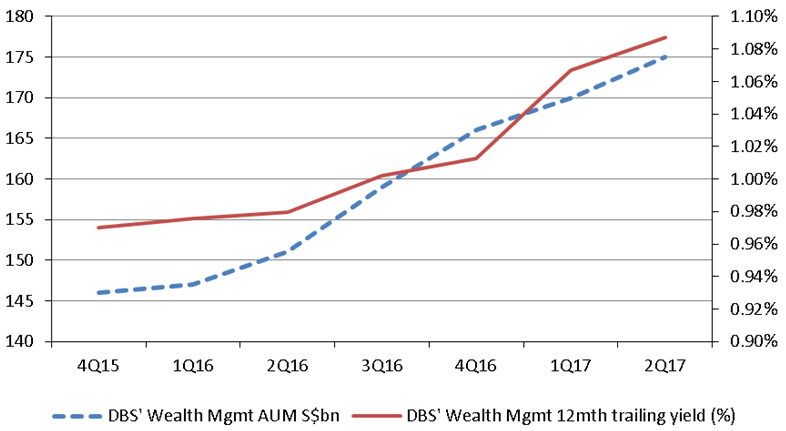

DBS’ WM growth came from the upper affluent clientele through the Treasures, Treasure Private Client and Private Bank platforms (See Fig. 3). We believe that DBS’ niche in the upper affluent market segment provides it with long term consistent growth.

UOB is lagging behind in WM compared to peers. UOB AUM from Privilege Banking, Privilege Reserve and Private Bank is only S$99bn. This is significantly lower than DBS AUM from Treasures, Treasures Private Client and Private Bank is S$175bn.

Figure 1: DBS’ and OCBC’s WM income share of total income has been increasing in the past quarters*

Source: Company, PSR estimates

*UOB does not separately disclose their WM income in full detail

Figure 2: OCBC’s AUM growth and broad WM product mix has driven quarterly WM income higher.

Source: Company, PSR estimates

Figure 3: DBS’ WM income supported by strong AUM growth in its Treasures, Treasures Private Client and Private Banking platforms and improving yields on these AUM.

Source: Company, PSR estimates

b) Quarterly provision expense may become more volatile as coverage ratios remain at historically low levels.

Offshore oil and gas vessel owners have been grappling with weak cash flow for about 2 years. Charter rates and charter tenures remain low. Therefore there are risks of elevated net NPL* from the sector. Write offs could become lumpier too as the prospects for recovery remains poor. Given the low coverage ratios, Singapore banks have less buffer to smoothen out the provision expense but will have to respond with the appropriate amount of provisioning expense in any given quarter if NPL formation becomes elevated.

* Net NPL formation is New NPL less upgrades, recoveries and translations.

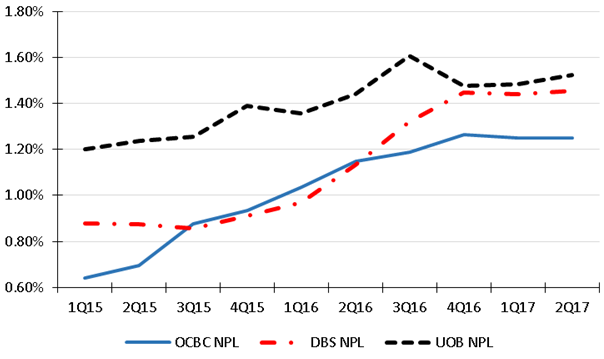

Figure 4: The Singapore Banks’ NPL ratio appears to have stabilized since 4Q16 as risks of lumpy NPL formation is behind us. But NPLs can remain elevated as the offshore Oil and Gas sector is not seeing a recovery soon.

Source: Company, PSR estimates

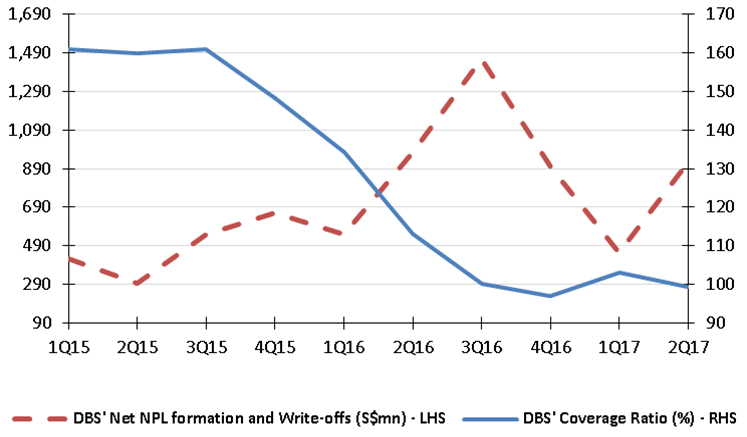

Figure 5: DBS’ coverage ratio holds steady at 100% as the profits from the sale of PwC building was used to pad up general provisions in 1Q17.

Source: Company, PSR estimates

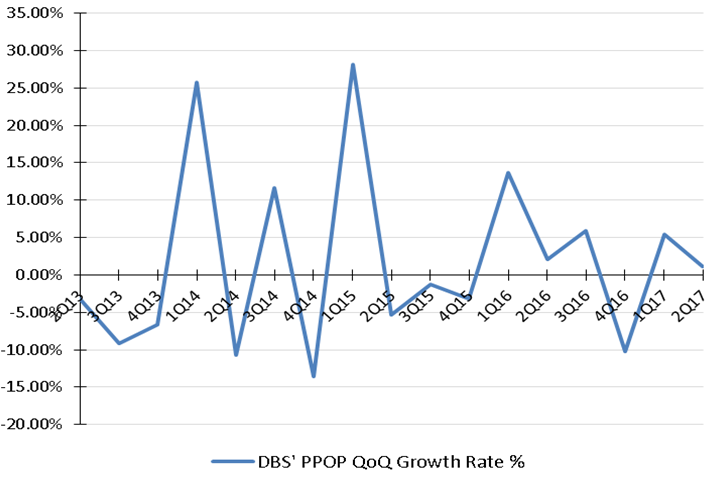

Figure 6: DBS’s recent quarterly PPOP growth rates have been insufficient to offset the elevated net NPL plus write offs. But we expect better performance in 2H17 for DBS.

Source: Company, PSR estimates

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Jeremy covers primarily the Banking and Finance sector. He has 6 years’ experience in equities related dealing and research roles.

He graduated with Bachelors of Mechanical Engineering from Nanyang Technological University.