The Positives

The Negatives

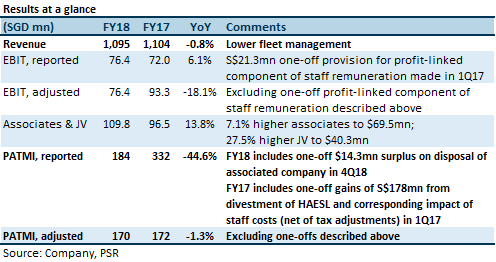

Outlook

The outlook is improving, but remains challenging. Management appears to have some visibility on the pipeline for engine shop visits. Our view is that even when engine shop visits return, the long-term normalised profit contribution will still be lower than historical level, due to lower work content. At the same time, competition from other MRO players is not expected to abate.

Maintain Accumulate; higher target price of S$3.57 (previously $3.51)

We have retained our Accumulate rating despite expecting lower PATMI in FY19e. The return of engine shop visits will be a positive catalyst for re-rating. However, we believe the profit recovery will be L-shaped. We expect FY20e earnings growth to be driven by contribution from the associates/JVs. SIAEC has a strong balance sheet in a net cash position and has positive free cash flow. Current dividend level of 13 cents is sustainable for a current yield of 3.9%.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.