Sembcorp Industries – Exceptional margin from conventional energy August 7, 2023 511

PSR Recommendation: ACCUMULATEStatus: Downgraded

Last Close Price: 5.23Target Price: 6.000

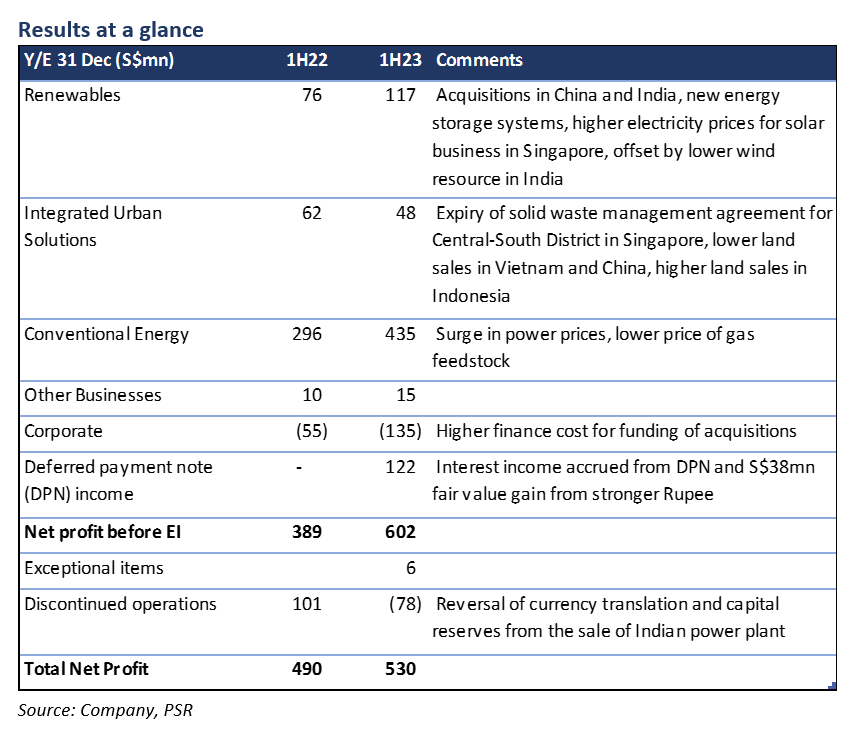

1H23 net profit beat our estimates, due to the surge in Singapore power prices (USEP), which peaked in May to S$492/MWh, and widening margins from lower gas prices. USEP has retreated to about S$200/MWh in July. Together with temporary price controls implemented by the Energy Market Authority (EMA) from 1 July, we think 2H23e conventional energy margin would normalize.

SCI began to accrue interest income of S$122mn from S$2bn deferred payment note it received from the sale of Indian power plants in Jan 2023. This includes a S$38mn fair value gain from a stronger Rupee. But it also booked a one-time non-cash accounting loss of S$78mn on reversal of currency translation and capital reserves.

We raise FY23e net profit estimates by 19.8% to factor in the stronger 1H23. We also lift TP to S$6.00 (previously S$5.06), based on an average 9x EV/EBITDA of FY24e estimates for the renewable energy players. Downgrade to ACCUMULATE due to recent price performance.

The Positives

Surge in Singapore power price in 2Q and lower gas prices boost profit from conventional energy. The Uniform Singapore Energy Price (USEP) rose to a peak of S$492/MWh in May due to scheduled maintenance at some power plants. SCI had lower contracted capacity in 2Q and hence was able to enjoy higher pool gains. The USEP has since retreated to about S$200/MWh in July, and margins are expected to normalise. Two-thirds of its capacity has been locked-in through long term contracts from 2H23. This helps to lock in volume and protect margins.

EMA implements temporary price controls from 1 July. The measures works to smoothen out any spike in USEP and still ensure a positive margin for the power producers. We believe the impact on SCI would be marginal. Profit from conventional energy would be shaved by 13.8% (S$60m) if it were implemented in 1H23. Net profit margin would be 2.1%pt lower at 13.1% (1H22: 9.5%).

Renewable energy segment books profits from new acquisitions in China and India, and the new energy storage system in Singapore. The solar infrastructure in Singapore also benefitted from higher electricity prices, offset by lower wind resources in India. Renewables make up 61% of the group’s total gross capacity. Current capacity of 11.9GW (including 3.3GW under development) well exceeds its target of 10GW by 2025.

SCI recognises accrued interest income of S$122mn from the S$2bn deferred payment note it received from the buyer of the Indian power plants. This amount includes S$38mn in fair value gain from a stronger Rupee. This is offset by a S$78mm non-cash accounting loss from the reversal of currency translation and capital reserves. In our earnings estimates, we assume these notes would be repaid over 20 years. SCI has received S$47mn in 1H23.

The Negatives

Weaker contributions from Integrated Urban Solutions was due to 1) expiry of solid waste management agreement for the Central-South district in Singapore; 2) lower land sale in Vietnam. SCI expects more land sales in 2H23 when the development permits are received from Vietnamese authorities; mitigated by 3) higher land sales in Indonesia. The sale of the solid waste management business has been called off.

Net gearing has risen to 1.38x (net debt S$6.6bn) with acquisitions of renewable energy portfolios in China and India, and the ground-breaking of a new 600MW hydrogen-ready combined cycle plant in Singapore which will be operational in 2026. The average cost of debt edged up by 0.6% pt to 4.7% from end 2022.

Subscribe

0 Comments

Inline Feedbacks

View all comments

About the author

Peggy Mak Research Manager PSR

Peggy has been a sell-side equity analyst for 22 years and a fund manager for 15 years.